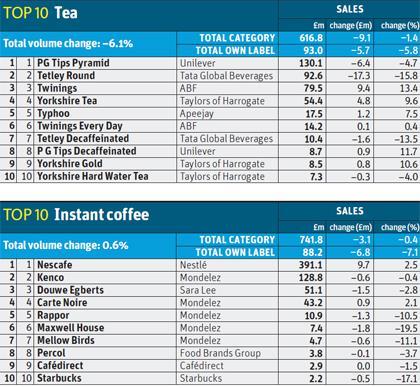

How long can Britain claim to be a nation of tea drinkers? There’s been a long-term decline in tea sales but it has significantly accelerated in 2013: value sales have fallen 1.4% and volumes are down 6.1% [Nielsen 52 w/e 12 October].

It hasn’t helped that the average price of tea in the supermarkets has risen 5%. But with tea sales falling, volume sold on deal has increased to 56% in the past year, a level of activity described as unsustainable by Tetley director of shopper & customer marketing Andrew Pearl. “Whereas before it was one brand on promotion, now it’s two or three,” he says. “People used to be loyal, but now they shop around for the best deal.”

Read The Grocer’s full Top Products Survey.

Pearl has every reason to be concerned because they’re leaving Tetley’s biggest seller, Rounds, in their droves: value is down 15.8% volume declines fell still more, as Tata implemented an 8.1% hike in average price over the past year, moving away from cut-price deals to focus on on-pack cash giveaways and link deals with McVitie’s biscuits.

“People used to be loyal, but now there are more promotions, they shop around for the best deal”

Andrew Pearl, Tetley

The contrast between Tetley and market leader PG Tips shows just how price sensitive tea has become. PG’s average price has fallen 4.5%, helping volumes to stay more or less flat (following a big decline in 2012) but inevitably dragging down the brand’s value. It’s lost £6.4m in sales over the past year, despite pumping £8m into marketing initiatives such as the PG Tips Cuppa Club.

Some players have another answer to the value drain: premiumisation. But tea brands aren’t necessarily using the same provenance and quality cues espoused by their colleagues in coffee to justify higher prices. Instead, they’re taking the health and functionality route - like our top launch, Twinings Sensations (see below). “The macro health trend has been driving growth in green tea and infusions,” says Twinings MD for the UK and Eire Jon Jenkins. “Consumers are increasingly seeking out premium teas, with 919,000 additional UK households purchasing premium tea in the past year.”

Kate Mitchell, brand manager for PG Tips, agrees that diversification and premiumisation remain a key category driver. “The biggest opportunity remains in getting people who drink normal tea to either substitute one drink for decaffeinated, more premium or speciality teas, or to add fruit and herbal teas to their repertoire,” she says.

Tetley’s Best of Both - the brand’s strongest grower of the past year, albeit from a small base - makes much of the health benefits of green tea in its marketing. However, despite the launch of the super-premium Tetley Estate Selection this year, Pearl says posher green and loose-leaf teas and herbal infusions can never replace an honest mug of builder’s tea.

“The number one thing is to address the decline in everyday tea which makes up 75% of the category,” he says. “But buying everyday tea is a very dull shopping experience - it is grab and go, whereas in other teas, people take longer and interact.”

Instant coffee

At first glance the instant coffee sector isn’t exactly in great shape either. Following the decision by major players in 2012 to pass cost rises on to consumers - driving up value by 9.1% but resulting in a 2.1% dip in volumes - in the past year value has flatlined as a result of increased deals. This contributed to a 0.6% rise in volumes. Hardly inspiring, but it could have been a lot worse.

The slight overall drop in instant coffee value was mitigated by 60.3% growth in wholebean instant, which helped brands outperform the market overall, with value growth of 0.6% on volumes up 4% (largely because of deals).

“Without wholebean, instant coffee would have seen declines at 3%,” says Nielsen coffee analyst Chris Fagan. “Wholebean’s performance has been driven by substantial gains from Nescafé Azera, and Mondelez’s Kenco Millicano and Carte Noire Instinct brands, as well as the introduction of private label.”

Top products: the stats

Nevertheless, the level of deals in the market remains a concern for Mondelez. “There’s a strong trend of consumers trading up to a better quality coffee. However it is currently a heavily promoted category,” says trade communications manager Susan Nash. To reduce reliance on price cuts, Mondelez has launched a rewards programme for Kenco and added price marks to refill packs.

Market leader Nescafé, which added an extra £9m in sales and growth of 2.5% on volumes up 6.3%, also notes demand for better quality instant coffee. “Consumers are seeking new coffee experiences within the premium segment and looking for a richer, full-bodied coffee from a brand they are familiar with,” says a spokesman for Nestlé, which added the Gold Blend Barista Style variant to the Nescafé line-up in August, and three new variants (Latte, Cappuccino and Intenso) to the Azera range in July to appeal to younger coffee drinkers.

Number three instant brand Douwe Egberts is also looking to appeal to younger consumers following the 2012 launch of the Flavoured Collective (in hazelnut, caramel and chocolate), although the brand’s value and volume decline suggests it has found the going tough. In contrast, flavoured coffee brand Beanies has achieved quintuple digit value and volume growth, albeit from a small base, thanks to distribution gains.

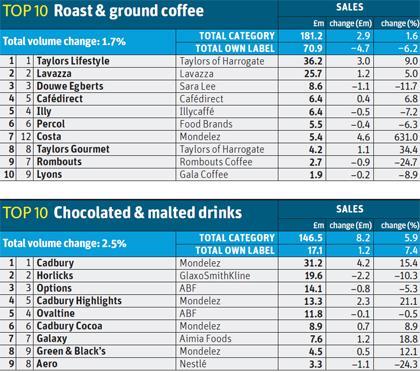

Roast and ground coffee

With premiumisation to the fore, roast and ground coffee volume growth has continued at broadly the same rate (up 1.7% versus 1.8% last year). On value growth it is a different story, however. Value sales rose just 1.6% versus last year’s 13.1% value growth, when manufacturers were successful both at passing on rising commodity price increases, and adding value through the continued growth of alternatives to the Nespresso that, unlike the Nestlé phenomenon, are predominantly marketed via the takehome channel. The average price of roast & ground brands has actually fallen 1.9% in the past year (against a 0.7% hike for own label), suggesting that more players are resorting to cut price deals to maintain share.

“Value growth has slowed but this is against a backdrop of over five years of double-digit growth,” says Paula Goude, category manager at Taylors of Harrogate.

The performance of Taylor’s Lifestyle and Gourmet brands certainly give reason for cheer, with market leader Taylor’s Lifestyle gaining £3m in extra sales and up 9%, and Gourmet adding another £1.1m (a 34% gain). While Lifestyle’s price dipped by a below-average 0.6%, it’s worth noting, however, that Gourmet - which sold at a 41p/kilo premium to Lifestyle in 2012 - has been selling at a penny less per kilo than Lifestyle in the past year, after a 3.5% average price drop.

Deals have been key to volume growth. “Around 38% of roast & ground is sold on deal, an increase from 34% last year,” says Goude. Yet she’s confident roast & ground can grow further. “UK penetration is up nearly a quarter and continues to improve year on year, so there is headroom for future growth albeit at a lower rate.”

Deals on brands have been a major contributor to own label’s 6.2% decline (on volumes down 6.8%), according to David Rogers, MD of Lavazza UK. But brands need to tread carefully, he warns: “Some have pursued an almost permanent programme this year. This is likely to damage the roasted category and participating brands in the long term.”

Others suggest the continued growth of high-street names Costa (up a staggering 631% to £5.4m and number seven in our ranking) and Starbucks (up 33% to £1.9m and the number 11 spot) as retail brands bodes well for future value growth. Indeed, with Costa selling for an average of £13.69 a kilo and Starbucks fetching £14.21, against a category average of £12.83, it shows punters are willing to pay more for that coffee shop experience.

The higher prices haven’t gone unnoticed at Tesco , which in October relaunched its Finest range, adding a host of new premium coffees (including a Hawaiian Kau Coffee with an rsp of £9.99/114g). Goude calls the new Finest prices “daring”: “This shows a better understanding of the true potential for premiumisation within the category.”

If big coffee brands like Starbucks are helping the roast and ground coffee market, the new Wispa hot chocolate appears to be doing the same for the hot chocolates and malted drinks category. Although more traditional malted drinks declined sharply - GSK’s Horlicks at number two fell 10.3%, on volumes down 15% - the overall category has steamed ahead, with growth of 5.9% on volumes up 2.5%.

This has been largely driven by Mondelez’s brands, which dominate the top 10. Cadbury grew 15.4% and Cadbury Highlights also rose, up 21% on volume growth of 10%. Mondelez credits its new Wispa hot chocolate as pivotal to driving sales this year, however. “It delivered £2m sales in its first four months with 76% of volume incremental to the hot chocolate category,” says Nash. Growth is coming from instant hot chocolate and diet hot chocolate in particular, she adds.

However, there is a shift in buying patterns, she notes. Although shoppers don’t want to give up affordable treats, they are buying smaller jars, because cost inflation has driven prices up 3.3%. Upmarket brands such as Green & Black’s are seeing the effects, up 12.1% by value on volumes up just 2.1%.

Read The Grocer’s full Top Products Survey.

Top launch: Herbal Sensations Twinings

As black tea continues to slump, flavours are increasingly important for brands. The demand for infusions is growing, and this year Twinings took it a step further with the launch of Herbal Sensations. This range of full-on fruity flavours came in response to insight suggesting consumers don’t just want to drink lightly perfumed ‘healthier’ drinks, they want intense flavours. This has helped add incremental sales and Twinings says it has driven 62% of the growth in the infusions sub category.

No comments yet