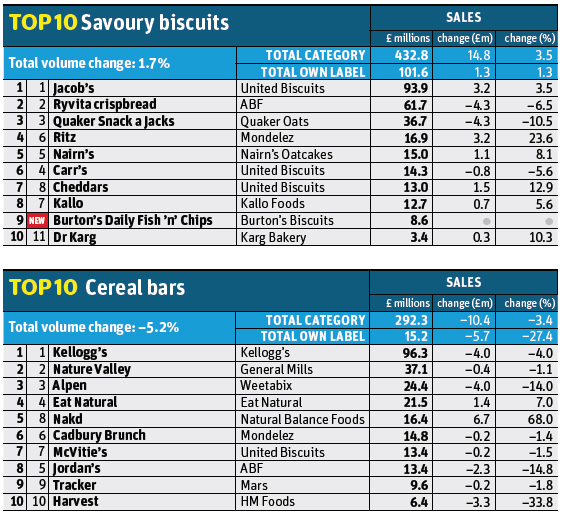

What a difference a year makes. Twelve months ago, breakfast was the most important meal of the day for biscuits in terms of growth. Belvita was up 29.1% and new launches from Weetabix and McVitie’s were booming after they jumped on the breakfast bandwagon.

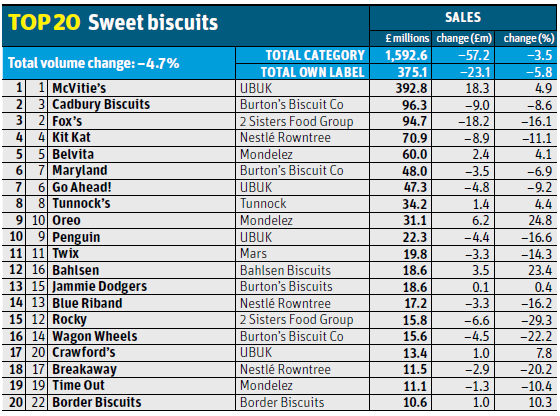

Now growth has stalled. Although Belvita has managed to grow (though at a much slower rate: value is up 4.1% on volumes up 2.9%) its breakfast-time rivals are struggling: Weetabix On-the-go has plummeted 23.7% in value; and McVitie’s Breakfast Biscuits are down 20.7% - the only dent in the brand’s otherwise impressive growth of the past year.

Breakfast isn’t the only biscuit sector struggling, either. Sales of sweet biscuits as a whole are down 3.5%, with volumes plunging 4.7%. Worst affected was Fox’s, down 16.1%, but several chocolate biscuit bars - Kit Kat, Penguin, Twix and Rocky - have all seen double-digit declines.

With brands on both side of the health divide struggling - Go Ahead! was another near double-digit casualty - it’s clear the decline isn’t all down to concerns about sugar and fat content.

So what is driving shoppers away? And how are some brands managing to defy the overall decline?

Part of the problem for the supermarkets is that we’re choosing to buy more biscuits from the discounters, which significantly overtrade in the category, with share of about 20% and counting, according to United Biscuits.

Value is falling out of the category as supermarkets lower prices to compete, says Jon Eggleton, UK MD of United Biscuits. “Deflation has played a crucial part; so has changing shopper behaviour,” he says. “Consumers are increasingly savvy, planning trips further in advance and reducing waste by throwing less away.”

So what can biscuit brands do? New United Biscuits CEO Martin Glenn made three key moves: last December he announced that McVitie’s would revert to its previous formulation to address concerns over taste and to tackle production issues. Second, he stopped supplying its Digestives in an own-label guise and at a knock-down price to Aldi. And finally he brought all its sweet brands (bar Go Ahead!) under the McVitie’s umbrella (at the same time, savoury brands Cheddars and Mini Cheddars successfully rebranded as Jacob’s, again backed by advertising).

As the numbers show, this strategy, backed by a £22m brand awareness campaign and the creation of a national field sales team, has worked a treat. To achieve 4.9% growth in a market declining 3.5% boils down to basics, Eggleton adds: “It is about offering prices and margins that ensure the most positive return on investment possible.”

It’s not the only strategy in play, of course. Promotions are still vital, though a Nestlé spokesman observes that consumers have become so used to buying biscuits on promotion that many have “become trained that £1 is the price for any biscuit pack.”

Some brands advocate greater use of deals and PMPs to create visible VFM in the price-sensitive everyday biscuits area. But Burton’s category management head David Costello believes: “Sustainable growth will only come from premiumisation.”

Portion control has been another key focus as brands try offer greater convenience and control over calorie intake. Mondelez attributes the respective 24.8% and 23.6% growth of Oreo and Ritz partly to the success of such formats. And after the nostalgic return of Burton’s Daily fish ‘n’ Chips in January (in 5x25g packs), in September it followed up with on-the-go packs of Cadbury Fingers and Maryland Gooeys and Choc Chip Cookies.

“Only 5% of traditional biscuits are in out-of-home format,” adds Costello. “With 5.8bn snacking opportunities in the workplace alone, the potential is enormous.”

Fox’s, looking to turn around its 16.1% decline, is hoping to open up new consumption occasions. For Julie Stevens, category controller at Fox’s, brands need to find ways to tap into special occasions like the ‘big night in’, and to look for more creative ways of merchandising their product.

Bahlsen trade marketing manager Julien Lacrampe believes the market is crying out for more innovation. “We haven’t seen true innovation in the last couple of years. New variants of existing products, new pack formats, packaging changes… but no real game changer.”

New products have paid off for Bahlsen. 23.4% growth was helped by the launch of Pick Up biscuit bars. The launch of McVitie’s BN (not strictly a new launch; it had previously been under the Jacob’s brand) contributed £3.9m of McVitie’s £18.3m growth. Even in breakfast biscuits Belvita bucked the decline with a Crunchy variant in April.

And what should we make of Nakd’s staggering 68% growth? In a cereal bar market down 5.2%, Jamison Combs, MD of Nakd brand owner Natural Balance Foods, believes its success is part of a “wholefood revolution”. “There’s a cross-category, cross-cultural, cross-generational desire for more natural alternatives,” he says.

It also taps into the free-from trend. Now there’s a thought.

Top launch: Cadbury Wispa Biscuits Burton’s Biscuit Co

After being extended into hot chocolate and chilled desserts, it was only natural that Wispa would join the Cadbury Special Occasions range, which Burton’s says is the fastest-growing range of NPD in the sector’s history.

The range already included Dairy Milk, Crunchie, Caramel, Bournville and Creme Egg varieties, but Wispa brought a distinct texture to the line-up to cater for fans of the bubbly bar. The launch was supported by a £250,000 campaign, PoS and in-store marketing.

No comments yet