Cheese is a tough place for brands right now. As the discounters expand into the sector, price is taking centre stage. Own label is growing; brands are paying for it. Category sales are up 0.3%, well below the rate of inflation and reflective of a 3.6% volume decline.

Brands are seeing their propositions challenged by retailers in all segments of the market. At the top end, Waitrose continues to bolster its diverse range of premium cheeses, which includes French artisan cheese Berthaut’s Epoisses and award-winning German blue Montagnolo Affiné.

Tesco has made a play to transform the mid-market by completely overhauling the way it merchandises cheese; blocks are now sold at key single price points of £1.50 and £2.50 instead of being grouped by flavour profile.

As if this weren’t enough, the discounters are reshaping the value end of the market by offering a tight range of quality cheeses at prices that make brands look expensive by comparison.

“As people become more aware of discounters’ prices, it becomes evident how high the prices are for branded products in the supermarkets,” says dairy consultant Hamish Renton of Hamish Renton Associates.

Lidl PR manager Georgina O’ Donnell notes the retailer’s cheese category “has seen a very high increase in sales over the past 12 months and our Cheddar performance, in particular, is ahead of the market with the emphasis being put on new formats and flavours to drive yet further growth.”

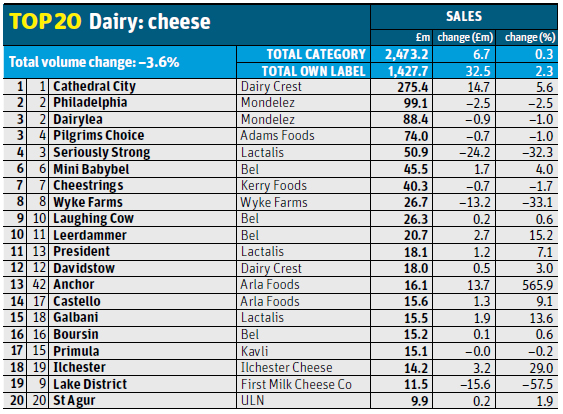

But while the majority of Cheddar brands have suffered at the hands of buoyant own labels, one brand continues to assert its superiority over the entire category. Cathedral City sales increased 5.6% to £275m as a fluid NPD pipeline, coupled with investment in marketing and advertising, continued to bear fruit.

“Cheese will be more affordable as a protein source and there’ll be big opportunities to get people to trade up…”

Cathedral City Spreadable launched in early 2014, and was followed in October by Cathedral City Selections British Cheese Variety Pack (see Top Launch), the brand’s first extension beyond Cheddar. Cathedral City also added value to the category by launching an Easy Tear Resealable Pack, and returned to TV screens in June for a new advertising push. Explaining the brand’s growth, Cathedral City’s marketing manager Elaine McCague says: “Dairy Crest invests significantly in a continued programme of value-adding marketing initiatives and innovation, alongside an intelligent promotional plan in order to differentiate from own-label and other brands.”

A further eye-catching performance came from Anchor Cheddar, which has racked up sales of £16.1m since its relaunch in April 2013 following a four-year absence from shelves. “Looking ahead to next year, we’ll be launching a through-the-line campaign, which will emphasise the brand’s taste and quality and be sure to continue the growth of Anchor Cheddar in the years to come,” says Matt Walker, senior category cheese director at brand owner Arla Foods.

Elsewhere, the news for Cheddar brands has been less positive. Wyke Farms, which - along with Lactalis McLelland’s Seriously Strong and First milk’s Lake District brand- suffered some of the sharpest losses in Cheddar this year, admits consumer demand for everyday low-price cheeses has taken a toll. However, MD Rich Clothier believes, with milk prices on a downward trajectory, the price of cheese should weaken in 2015 to the benefit of branded suppliers.

“As the economy improves next year, we’ll be doing some TV and magazine ads in April and the autumn. The economy is going to be better, cheese prices will be softening so it will be more affordable as a protein source, and I think there’ll be big opportunities to get people to trade up within the category without it being prohibitively expensive.”

Investing in advertising

Advertising is also on the agenda for Pilgrims Choice, which has just about held its own this year, having been boosted by the launch in April of Pilgrims Choice Crumbles, a three-strong premium range of grated Cheddar. “Because the market has been so competitive, the competitor set has spent less on TV than they have done previously,” says Mike Harper, director of brands at Pilgrims Choice owner Adams Foods. “That’s something we need to work hard on next year to make sure we continue to do above-the-line and drive consumers to make those choices and pay that premium for branded Cheddar.”

Sales of leading Continental brands such as Président, Castello and Galbani have all grown, suggesting Brits’ love of Continental cheese shows no sign of abating. Arla Foods recently launched a pop-up shop in London to showcase the diversity of its Castello range, which encompasses blue cheese, hard cheese, soft cheese and extra-mature Cheddar. “Traditional provenance is becoming less important to consumers nowadays, as seen by the recent rapid growth of British Brie and Camembert in the UK market,” says Walker. “Ultimately, consumers are looking for great-tasting cheeses that offer something a bit different from the norm.”

Although mini portions and segments have not been able to match the growth of Continental cheeses, they have proved resilient, with sales of Dairylea, Cheestrings and Laughing Cow staying relatively flat but Mini Babybel delivering a 4% sales increase. Things have just got a whole lot tougher for suppliers of kids’ snacking products with the introduction of free school meals for all primary schoolchildren under seven. Harper believes brands, including Adams’ Mu Cheddar, could find a key snacking occasion restricted by the new policy. “The main occasion for kids’ snacking cheese at the moment is predominantly in lunchboxes, so I do think it will have a big effect.”

Brands may increasingly have to target an older audience if they wish to grow sales of snacking products. Bel UK’s repositioning of its The Laughing Cow Cheez Dippers as Dip & Crunch earlier this year to appeal more to adults is an example of one such move.

Health credentials

Suppliers are also highlighting the health credentials of snacking products in a bid to appeal to an increasingly health-conscious consumer. “Our Laughing Cow Light with Blue Cheese and Light with Emmental variants are both performing well, with the success reflecting the strong ‘25 calories per triangle’ claim,” says Steve Gregory, marketing director at Bel UK.

Bel UK has also relaunched Leerdammer Light with a new front-of-pack nutritional claim to better demonstrate to consumers how natural slices measure up to other cheeses. Instead of the previous claim that stated Leerdammer Light contains ‘38% less fat than Leerdammer Original’, the messaging now reads ‘50% less fat than Cheddar.’

Also pushing a health message is Kerry Foods, which in March launched a new TV campaign for Cheestrings highlighting its calcium content and ‘real cheese’ credentials.

The campaign tied in with Cheestrings’ Brave Bones website, which allows families to sign up and complete a challenges to earn virtual badges to celebrate their achievements.

Cheese brands will need to keep investing in such marketing initiatives throughout 2015 if they’re to reclaim the initiative from their private-label counterparts.

Top launch: Cathedral City Spreadable by Dairy Crest

Dairy Crest moved to shake up the cheese spreads category early in 2014 with the launch of this spreadable version of its market-leading Cathedral City.

Tapping consumer demand for convenience while offering a familiar brand and “authentic” flavour profile, the launch came after Dairy Crest spent many years in R&D working on a spreadable product good enough to sit under the Cathedral City brand. The launch was backed with a £1.3m media campaign.

No comments yet