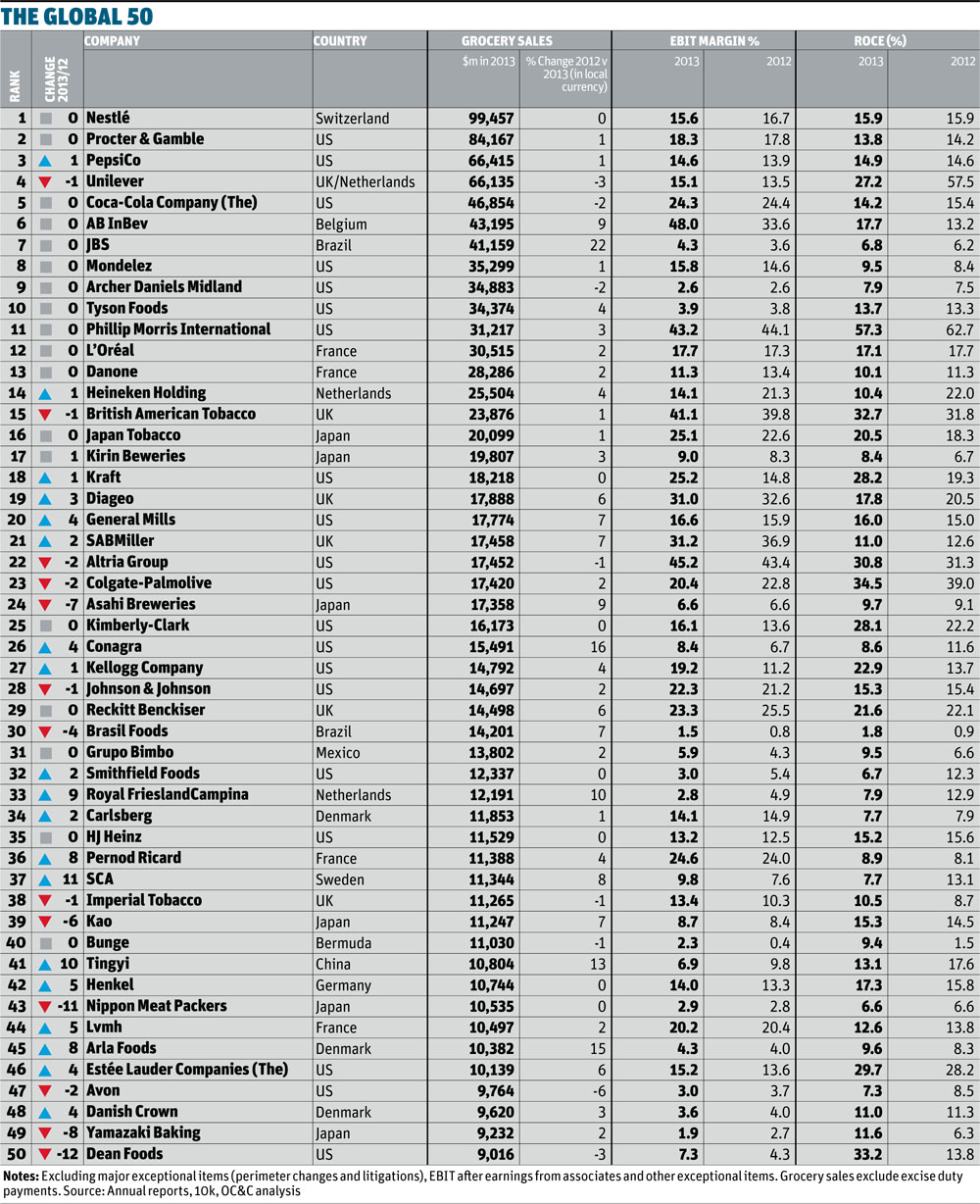

At first glance, the headline growth figures of the giants of fmcg look dire. The world’s 50 biggest suppliers have seen their sales growth halve from 5.6% last year to 2.9%, according to this year’s Global 50, a report carried out exclusively for The Grocer by OC&C Strategy Consultants.

Nestlé hit the headlines in February when it missed its long-term annual growth target of 5% to 6% for the first time since 2009. It was not alone. Unilever, Diageo, Coca-Cola and Danone have all posted weaker than expected growth figures over the past year.

“There is a bit more caution now about emerging markets. The preference tends to be joint ventures or minority stakes”

But when you start to unpick the reasons for their poor performance it provides some degree of reassurance for the industry big guns. For instance, uncontrollable factors like exchange rate volatility has had a major impact on the performance of the Global 50 - Unilever’s emerging markets business, which accounts for 57% of turnover, suffered a negative sales impact from foreign exchange of 5.9%. Falling commodity prices have also hit companies hard - two years of tumbling grain and sugar costs have constrained price growth.

Even when you take these factors into account, however, some worrying trends remain. In the fast-growing emerging markets that are still the engines of growth for the Global 50, the big international companies are losing market share to local players.

This year, Tingyi becomes the first Chinese player to enter the Global 50, and two other Chinese companies are banging loudly on the door - Yili Group and Mengniu. Yili climbed four places to 58 this year and Mengniu climbed eight places to 60.

So what’s happening on the ground? Why are these local players outfoxing the global fmcg behemoths and what are the key ingredients they need to add to ensure future growth?

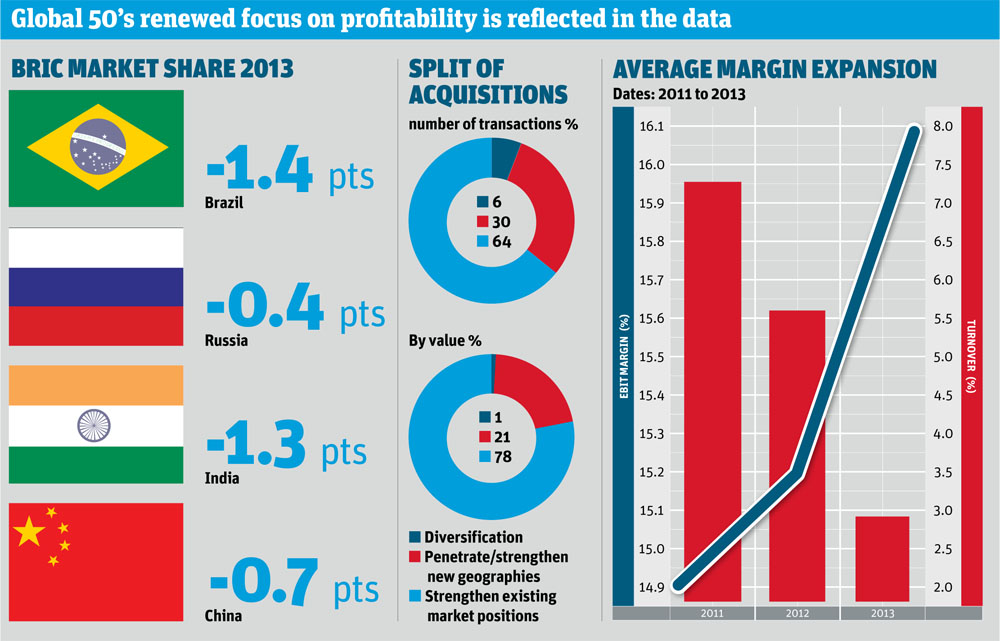

One of the most striking findings from this year’s report is the mismatch between sales growth and margins. Whereas in previous years, sales growth was strong and margin performance was poor, this year the reverse is true. Gross margins grew by 0.7 percentage points compared with 0.1% the previous year -in turn this has driven a 0.9 percentage point expansion in EBIT margin. Meanwhile, headline sales growth slowed to 2.9% in 2013, versus 5.6% in 2012.

Shift in focus

OC&C partner Will Hayllar believes this trend is not just a reflection of commodity cost changes, but the result of conscious strategic reorientation. The biggest players are now more focused on growing profits than growing the top line.

“There is a much stronger emphasis now from the leading suppliers on rebuilding profitability,” says Hayllar. “Between 2007 and 2012 the Global 50 lost almost three percentage points of EBIT margin so they are eager to claw some of that lost margin back.”

“In China, local players typically have stronger, deeper distribution networks and are better at store activation”

This shift is particularly evident in the way the Global 50 talks to investors. Analysis by OC&C of the annual reports of the Global 50 found that the amount of space dedicated to the discussion of long-term goals, such as sustainability and supply chain enhancement, had shrunk this year in favour of subjects that had a more immediate financial impact like geographic expansion and restructuring,

The new focus on profitability is also underlined by M&A. In recent years, M&A has typically added one percentage point to the sales growth of the Global 50, but this year the impact was neutral. Indeed, many have looked to sell off businesses that offer poor margins and growth prospects or are a poor fit with their core operations.

For example, Nestlé sold its stake in ingredients group Givaudan at the end of last year. This year P&G sold its US petcare business. Unilever disposed of its Ragu and Peperami businesses. Divestments made up 43.1% of deal value in 2013/2014, compared with just 16.9% the previous year.

At the same time, the majority of acquisitions that have gone through have been motivated by a desire to strengthen existing market positions rather than to diversify or enter new geographies.

“There is a bit more caution now about emerging markets. The preference tends to be for joint ventures or minority stakes. When local entrepreneurs are willing to cede control, in a high growth environment, you have to ask why,” says Magnus Scaddan, managing director and head of EMEA consumer and retail at Houlihan Lokey.

Mindset shift

In emerging markets more generally the mindset has shifted, according to OC&C partner Richard McKenzie. Instead of going after growth at any cost, international companies are now behaving more like normal businesses.

Global 50 - top performers

AB InBev

Grocery sales: $43.2bn (+9%)

Margin: 48% (14.4 percentage point increase)

The world’s largest brewer negated a 2% volume decline and negative currency movements by improving pricing strategy, focusing on premium brands and completing the $20.1bn acquisition of Mexican brewer Grupo Modelo.

Arla Foods

Grocery sales: $10.4bn (+15%)

Margin: 4.3% (0.3 percentage point increase)

The Danish dairy firm saw a 15% rise in local currency sales last year, driven by a strong performance in its fresh dairy business, which represents 43% of total turnover. Arla’s revenues in China (Arla branded products and third party manufacturing) doubled in 2013.

ConAgra Foods

Grocery sales: $15.5bn (+16%)

Margin: 8.4% (1.7 percentage point increase)

US company’s consumer and commercial foods divisions showed organic sales growth of 8% and 4% respectively. Top-line growth also boosted by its acquisition of US food supplier Ralcorp Holdings for $6.8bn.

JBS

Grocery sales: $41.2bn (+22%)

Margin: 4.3% (0.7 percent point increase)

The Brazilian meat company topped the table for annual growth, with acquisitions and organic growth driving its 22% increase in sales. The firm acquired Seara Alimentos, the second-largest poultry and pork processor in Brazil, for R$5.85 in June 2013 and saw its US beef and poultry businesses grow by 6.5% and 3.6% respectively.

Tingyi

Grocery sales: $10.8bn (+13%)

Margin: 6.9% (2.9 percentage point decrease)

The Chinese food and drink company entered the Global 50 after recording 13% local currency sales growth. This performance was primarily driven by a 27% rise in beverage sales, helped by its exclusive partnership with Pepsi in China.

“When I first arrived in China most conversations I had were with people who had been told to invest as much as possible,” says McKenzie, who is based in the company’s Shanghai office. “Now a more normal business attitude has emerged. The mentality has shifted from a land grab to a need to extract value.”

The innovation strategy of the leading players also reflects a more cautious, profit-focused approach. New product development is centred on line extensions within core categories. There is comparatively little in the way of innovation in adjacent categories and very little that breaks new ground. Analysis by OC&C suggests more than 80% of innovation fell into the category of ‘core renovation’ rather than ‘genuine innovation’.

This conservative approach reflects a lack of investment in R&D. Only eight of the Global 50 are spending more than 2% of turnover on R&D, with most spending less than 1%, estimates OC&C.

At the same time, when they do launch new products, the multinational players are looking to get the most of their investments by going into as many countries as possible.

“We continue each year to make our innovation bigger, reaching to more countries - last year we had 70 innovations that reached 10 or more countries,” says a spokeswoman for Unilever.

And even on those rare occasions when they do target innovations at specific countries, the main priority is on the emerging markets, judging by OC&C’s research. The company estimates that more than two thirds of region-specific innovations are in emerging markets and it’s easy to see why as, currency issues aside, emerging markets continue to be the engines of growth for the Global 50. Those companies generating more than 50% of their sales from Asia and Africa grew by 3.6% , whereas those with less than 30% of their turnover from these regions experienced average growth of just 1.6%, says OC&C.

Tough trading conditions for drinks giants

The headline growth of the world’s largest beer and spirits companies remained strong in 2013, but the overall positive figures masked tough trading conditions.

Booze suppliers with a high exposure to Asian markets struggled, with Japanese companies in particular impacted by the relative depreciation of the Japanese yen.

Kirin Breweries, for example, saw total turnover drop 14% in 2013 while Asahi Breweries recorded a full-year turnover fall of 11%.

The Chinese spirits market was also impacted by the imposition of new anti-extravagance and corruption measures, which helped trigger a 66% decline in net sales at ShuiJingFang (in which Diageo holds a 39.71% stake).

Diageo’s growth in China fell from 13% to 5%; and it also suffered a sales decline in India last financial year (-2%) while Brazilian growth fell from 20% year-on-year to just 1%.

In this environment Diageo will probably be pleased that global sales rose 6% to $17.9bn; while SAB Miller sales were up 7% to $17.5bn. The best performance came from AB InBev, which saw turnover rise 9% to $43.2bn; while Heineken was up 4% to $25.5bn.

Additionally, four of the top 10 profit margins in the study belonged to alcohol producers. AB InBev topped the Global 50 with a margin of 48%. However, beer & spirits firms are battling declining volumes and negative currency trends.

AB InBev’s 9% growth was boosted by acquisition (it bought the outstanding 50% of Mexican brewer Grupo Modelo, while volumes declined 2% globally and FX movements caused a net loss.

Similarly, Heineken’s turnover was boosted by acquiring Asia’s APB and Serbian brewer Central European Breweries, which offset a 4% global volume decline and a net loss from currency fluctuations. Crucially, both brewers increased their price/volume ratio, with AB InBev benefiting from a shift to more premium brands and Heineken investing in innovation and stronger pricing.

Growth of local companies

The spoils from emerging markets are not spread evenly, however, with local companies enjoying the most spectacular growth. The four companies in the Global 50 that are based in emerging markets (JBS, Brazil Foods, Grupo Bimbo and Tingyi) grew at 14.6% last year. Excluding them, the Global 50 are losing market share across the BRIC countries (Brazil -1.4 points, Russia -0.4, India -1.3, China -0.7).

The renewed focus on profitability by the multinationals is part of the story, but it is also impossible to ignore the growing strength of local competitors.

“In China, local players typically have stronger, deeper distribution networks and are better at store activation,” says McKenzie. “In an average supermarket, half the staff will be paid by suppliers and employed to push their products. Local players are better at using that. It’s not in the DNA of the international players.”

“We will tailor global campaigns for local use. A great example is our activity for the World Cup in Latin America”

Tingyi is a case in point. And, as the first Chinese company in the Global 50 it demonstrates both the strength of local players and the new profit focus of international players. Delivering direct to 110,000 stores and with more than 500 sales offices across China, Tingyi has built up a distribution network that is hard for international companies to compete against.

PepsiCo saw the potential of the company back in 2011. The US soft drinks giant had already built a strong presence in China, but growing distribution was proving costly and signing a deal with Tingyi allowed it to piggyback on its vast network. In 2013, Pepsi’s drinks business under Tingyi grew by 20% and became profitable.

Tingyi’s approach to innovation is another important factor in its success. “It is very good at trying new flavours, new packs, new twists, and in common with other Chinese businesses, it’s not afraid to let things fail,” says McKenzie.

Whereas most multinational groups are constrained by the logic of international rollouts and tend to have a preference for carefully prepared ‘big bang’ launches, with tastes constantly changing in the fast-evolving emerging markets, the more market-focused approach of Tingyi and other local players gives them an edge over their rivals.

So how can international players fight back against this wave of rapidly expanding local operators? PepsiCo is not the only Western business to embrace the idea that ‘if you can’t beat them, join them’. Weetabix has taken a slightly different tack.

Local partnerships

Since its acquisition by China-based Bright Food, the cereal giant has been able to expand into China in a way that would have been unthinkable before. Using Bright’s distribution network, its products are now on sale in 4,000 Shanghai stores, but its new owners have been able to help in other ways, too.

“They know how the market works and are able to help us adapt our communication to local consumers,” says Weetabix commercial director Kevin Fawell. “The Chinese also have very different tastes in terms of breakfast - it tends to be hot and savoury. So what we have to do is make sure we have the right offer. The model is global brands adapted locally.”

“Between 2007 and 2012 the Global 50 lost almost three percentage points of EBIT margin, so they are eager to claw some of that back”

Weetabix has yet to develop a product for the Chinese market, but it is looking at new flavours such as green tea for its breakfast cereals and snacks. Other Global 50 players are looking to follow Weetabix’s lead by opening up innovation labs in these emerging markets to accelerate the R&D process. For example, at the end of 2012 PepsiCo opened its first R&D centre outside North America, in Shanghai.

But Hayllar believes that more can be done to develop better products and get them to market quicker. “It is still relatively slow. A lot are investing in innovation centres, but I’m not sure the mindset has changed. They’re still relatively risk-averse,” he argues.

The global giants do appear to be working harder to make their marketing better suited to individual markets. Speaking at the Deutsche Bank Global Consumer Conference in Paris in June, Diageo CEO Ivan Menezes said: “We will tailor global campaigns for local use. A great example of these more locally based activations is the activity we’ve put in place for the World Cup in Latin America. This is an integrated campaign across six countries, using the simple message that the ‘best’ have come to Brazil for the World Cup and asking the question, on a soccer ball: ‘Do you have the best in your cup?’

MINTS

As BRICs become more competitive, the Global 50 are increasingly exploring new markets as well. The MINTs (Mexico, Indonesia, Nigeria, Turkey) are steadily making their way on to the agendas of the global giants. Of the 11 companies in the Global 50 who reported underperformance in a BRIC country in their annual report, eight named a MINT country as a key growth market.

“There are commonalities between BRICs and MINTs,” says Hayllar. “They all have strong macro fundamentals and have significant classes of people who can afford to buy consumer goods. But in the MINTs, the competitive intensity is typically lower. You don’t have as many global players seriously investing, and local players are often weaker.”

Those that went into the MINT markets early have reaped rewards. For example, by 2010 in Nigeria, Coca-Cola had built a 41% share of the soft drinks market (versus 26% globally) and Nestlé had a 69% share of the coffee market (versus 22% globally).

Growth accelerates

As in the BRIC markets, forming partnerships with established players can be a good way of accelerating growth. For example, Kellogg’s has established a strong presence in Turkey where its products are co-branded with local food manufacturer Ulker. However, in places like Nigeria, there is less scope to do this. “Operating in Nigeria there are fewer well developed incumbents. That requires them do heavy lifting themselves to build up distribution,” says Hayllar.And as with the BRICs, there are risks attached to expanding into the MINTs. Inconsistent growth is common.

For example, Diageo enjoyed 18% growth in Scotch sales in Mexico, but in Turkey increased excise duty caused a sharp slowdown in sales. The challenge for the Global 50 will be to build sustainable businesses that offer long-term profitable growth. The lesson from the trailblazers is that there is no quick fix.

“Those who succeeded came in early and were willing to take their time. They took each market seriously, really getting to know it and understanding where and how to sell,” says Hayllar.

The record of M&A as a short cut to building bigger emerging market businesses is mixed. City sources see more potential from combining some of the biggest names in the Global 50 and are talking up the prospects of mega deals. Would Mondelez and Danone make a good fit? How about Kellogg’s and Campbell’s? Could Unilever make a move on Colgate? And could Coca-Cola bid for Danone or even Nestlé?

The conservative approach to deal-making since the recessions means many companies have the means to pull off what sound like far-fetched deals. Coca-Cola is sitting on an estimated cash pile of more than $20bn. With that sort of money to throw around, anything is possible.

China set to be biggest dairy market in world

Dairy is not a traditional part of the Chinese diet, but by 2018 China is expected to become the biggest dairy market in the world, worth over $60bn (Canadean), as the government has lent its support (and investment) to the country’s dairy farming industry and the growing middle class develops a taste for yoghurts and flavoured milks.

The market is dominated by two local players, Yili and Mengniu.

Like other Chinese companies, fast-paced innovation has been key to their success. In 2013, Mengiu launched 12 products and Yili 11, including papaya milk and flavoured milk for cereal. “The market is very different to the UK - a common gift when visiting friends would be a pack of milk,” says OC&C’s McKenzie.

Domestic players have also adapted products to local challenges. Bright launched a UHT yoghurt brand in 2009 called Momchilovtsi - named after a Bulgarian village where the locals allegedly live longer thanks to the local yoghurt - that has a four-month shelf life. It quickly established itself as China’s fourth-biggest yoghurt brand.

Meanwhile, international companies have struggled to establish significant market share, unable to compete with local suppliers on price. Where they have a strong presence is infant nutrition because Chinese consumers trust foreign brands ahead of local ones following the melamine milk scandal in 2008. That could change. New government requirements to register foreign brands and fines imposed last year on several foreign companies for anti-competitive behaviour have been reported as the government attempts to bolster domestic infant nutrition brands.

High Chinese demand has put pressure on global dairy prices and the margins of global players such as Danone and Royal FrieslandCampina. Only Arla has been able to grow EBIT margin - albeit by just 0.3% - thanks largely to an effective global cost-cutting programme.

No comments yet