If the UK’s food and drink producers did not realise they had been experiencing a momentary calm before the storm, they are now in little doubt a category five hurricane is upon them.

Pressure is intensifying not so much due to fundamentals (the economy is, after all improving) but as a result of seismic structural change within the grocery retail industry. As prices are slashed, shares crash, and senior execs are hastened to the exit, supermarket margins have reached their lowest level for almost 30 years. Indeed, the grocers have been rendered “uninvestable” according to one analyst, due to the sheer murkiness of the outlook.

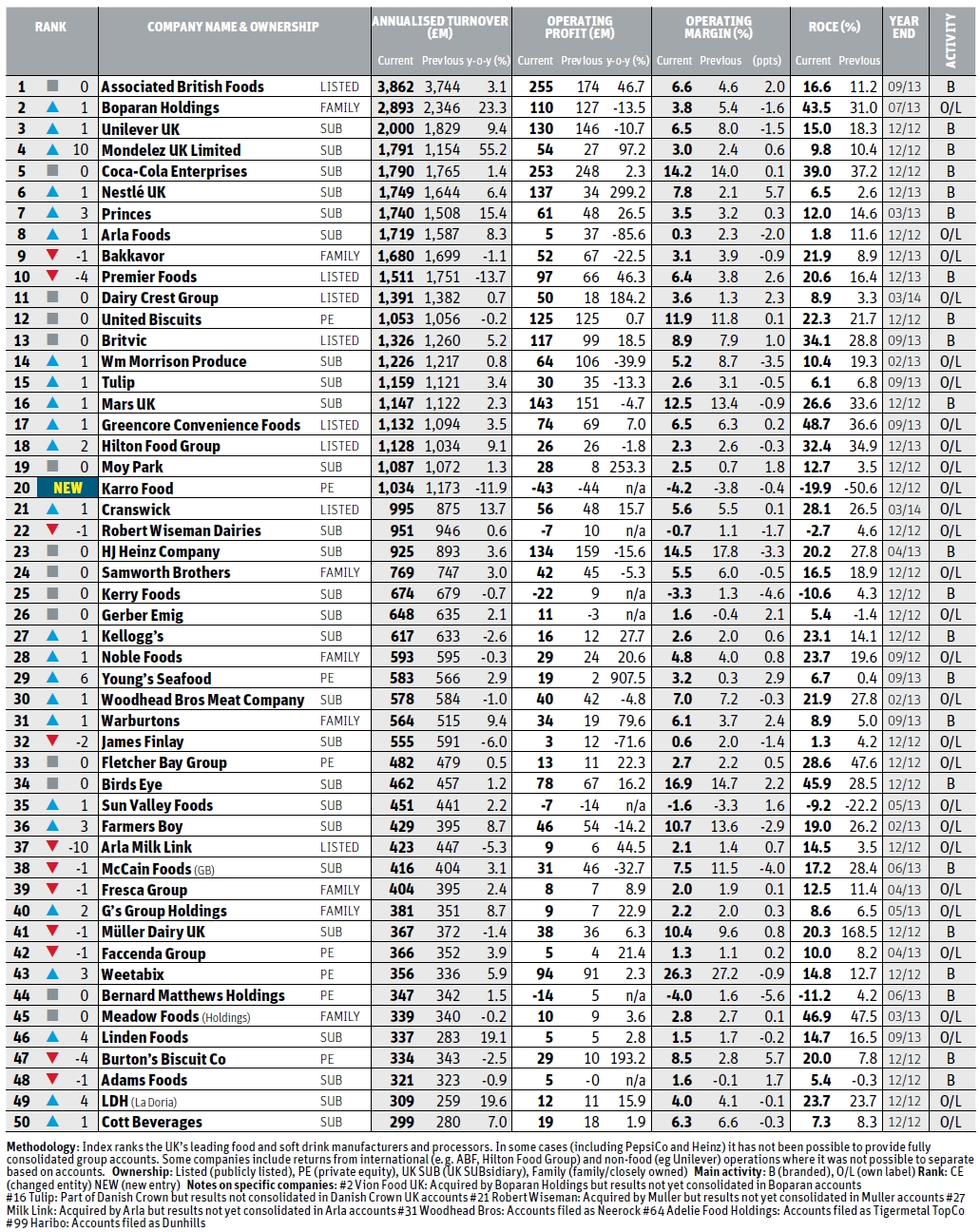

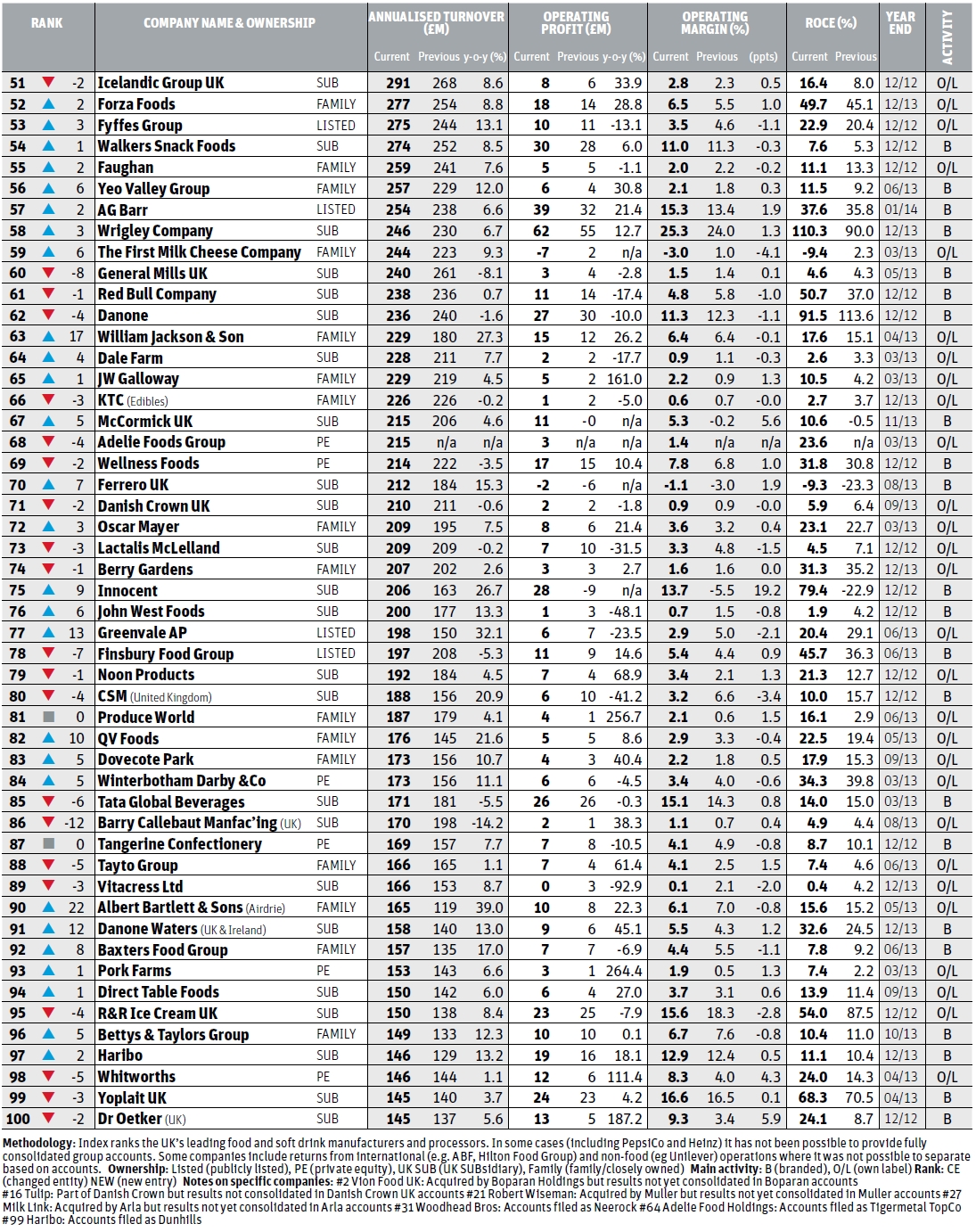

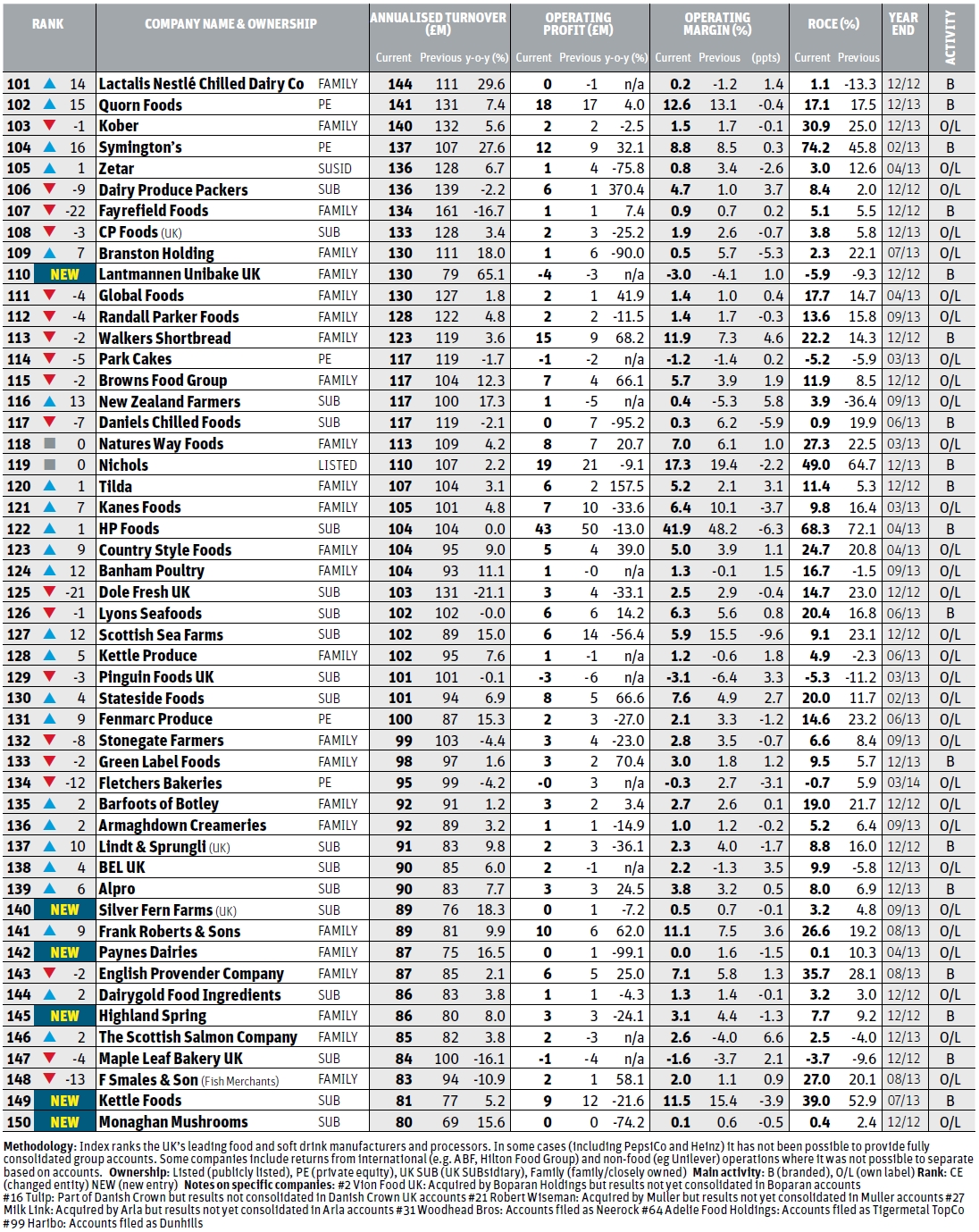

The OC&C Grocer Index 2014 therefore comes with something of a Health warning: compiled for The Grocer by OC&C Strategy Consultants, the Food & Drink 150 mostly features results from 2012 or 2013. It showed UK suppliers increasing sales (5.8% in 2013 against 5.6% in 2012). Over 75% of companies experienced growth last year. What’s more, margins have finally stabilised after two years of rapid decline, staying at 5.2%, having topped 6.5% just three years ago.

Taking into account the growth in consumer expenditure since the double-dip in 2012, UK GDP returning to pre-recession levels and commodity inflation largely slowing down, the data seems to show the worst ravages of the recession are behind us. But clearly these historic figures tell only part of the story. As the title of OC&C’s report states, this is looking like a ‘False Dawn.’

The structural changes now affecting grocery retail have been well rehearsed – essentially the old superstore model has broken as the rise of online, discounters and convenience eats away at sales and profits.

So it comes as no surprise that amid 2014’s flood of supermarket profit warnings, declarations of price wars and the plunge in overall UK food sales, the market for food and drink suppliers is more hostile than the pure numbers suggest. Far from experiencing the green shoots of recovery, OC&C’s report points to an industry embarking on its toughest test for a generation. When the supermarkets last embarked on a price war with the launch of value ranges in the recessionary early 1990s, supplier margins were touching 6%. Producers are now facing a new price war with margins touching historic lows of 5%.

This has created an environment where food and drink suppliers are having to rapidly adapt, but with all-time low margins there is little spare cash and even less scope to be squeezed by under-pressure retailers.

“Conditions aren’t getting any easier,” says Innocent CEO Douglas Lamont. “2014 feels like the toughest year yet.”

Will Hayllar, co-leader of OC&C’s global consumer goods team, argues that although the shift to discounters has accelerated, the underlying trends causing industry pain right now have been around for years. “Some of the factors that were masking the impact of these trends, like food price inflation, have fallen away, which has really magnified the growth challenge,” he notes.

Clear disparities between winners and losers are already emerging. Notably, the disruptive market conditions have provided further impetus for the shift in power from larger to smaller producers. The 2013 financial figures show smaller players (under £500m turnover) have grown more (5.9% vs 5.6%) and improved margins more (0.2%) compared with a 0.1% margin decline for larger branded producers and a 0.5% decline for large unbranded suppliers.

It’s a trend Hayllar expects to solidify in 2014. “The fragmentation of consumer demand in certain categories favours smaller brands that have generally been faster to adapt to the new conditions,” he says.

Pack/price adaptability is key

With the rise of online, convenience and the discounters, suppliers have never had so many channels to sell through. That means a one size fits all approach to pack size and pricing is now redundant. And the need to adapt is more important than ever.

“You have to adapt, it’s become a standard thing we’ve all had to do,” says Innocent CEO Douglas Lamont. “It adds complexity, but it’s important to keep moving in the right direction. It’s about taking advantage of convenience or online and considering what that means in terms of price point and pack sizes.”

Right now, the hottest channel of all is the discounters. One senior industry figure from a global brand that supplies Lidl with personal care products simply rolls his eyes and grins when asked about the volumes being shifted through the discounter. And Will Hayllar suggests, even if there are potentially tricky factors to consider, there are solutions.

“You might have a proposition that the discounters want to sell, but in doing so, how do you make sure you’re not undermining your price position in other channels?” he asks. “Part of the answer is product and pack architecture.”

Famously, that pack architecture is how the fixed price discounters like Poundland have thrived, keeping their round pound prices intact while simultaneously delivering big brands. So six packs of Walkers crisps become five, or a Toblerone loses a triangle. However, it still represents value to shoppers, and the fact that big brands are happy to tinker with production lines and packaging strongly suggests the volumes they are moving through the channel justify the additional complexity.

“It could be about the size of the pack and the price, or it could be about an absolute price point – and if you cross those points it can have a non-rational impact on the scale of how many people will buy that product,” adds Lamont. “So we have always tried to understand where those breaks in the road are. And make sure we don’t cross them.”

Of course, its a precarious business getting it spot on but if you’re not set up to offer flexible pack and price architecture, you’re limiting your options.

Many of those more fleet-of-foot producers have been able to outmanoeuvre the multinational behemoths as retail format fragmentation has meant the benefits of sheer scale have proved of limited use in meeting retailer needs. Quorn CEO Kevin Brennan explains: “It does help in this environment that if a retailer comes to us with an opportunity we can respond very quickly and move from deciding there’s an opportunity to implementation.”

Some of the more successful mid-sized businesses have used this flexibility – enhanced in some instances by private ownership and a lack of quarterly reporting – to strategically invest in new product lines, product development or packaging architecture (see box right), while larger players have found executing radical product and production changes more challenging.

Of the five companies picked out as ‘winning’ against the tough trading backdrop (see p35) this targeted investment in NPD is a recurring theme. Brennan notes that in the past three years Quorn has seen a fivefold increase in its NPD investment, while Cranswick CEO Adam Couch calls NPD the “lifeblood” of the meat producer’s business.

Referencing Cranswick’s move into premium pasty production after launching a joint venture in Malton late last year, Couch says: “Having that product innovation and coming up with ideas that will resonate with the consumer and customer has allowed us to get some real purchase in the marketplace… There are a lot of meat operators out there and we want to innovate in areas that can’t be easily copied.”

Brand differentiation

That sense of brand differentiation is becoming vital, given the growth of the primarily own-label discounters, competition for convenience shelf space and tightening margins. A number of those thriving in the current market have brands with strong consumer followings – often number one in their chosen markets or those that particularly resonate with a distinct consumer segment (ie premium, value or convenience).

Even with tightening margins, players such as Haribo and Quorn have supported NPD by generating brand distinctiveness through vastly increased ad spend (Haribo accounts for 21% of market ad spend and Quorn has increased ad spend eightfold in recent years). But other smaller brands are increasingly able to build those connections with consumers without huge ad budgets via more targeted online campaigns focused on engaging specific consumer groups.

Hayllar notes: “The more you’re offering a brand to people who are engaged, the more potent digital is as a marketing tool. Some of those successful smaller brands have done that in a way that’s left big incumbent brands looking a bit outdated.”

In that sense, brands with weak distinctiveness or producers with wide product portfolios but little depth behind those lines are among those most exposed to the current market pressures. These brands could find themselves in the uncomfortable position of being traded as pawns in a price war or usurped by own-label products. “There will always be a market for strong brands at a fair price,” says Haribo UK MD Herwig Vennekens. “What’s difficult is if you find yourselves in the middle, with products where the quality is not the best or which are more generic without much brand strength. In this day and age that is a very dangerous area to be.”

Cranswick

Turnover (£m): 995

Turnover growth: 13.7%

Operating margin: 5.6%

Margin change (% pts): +0.1

UK-listed meat producer Cranswick recorded strong organic growth in the UK and its export business. UK revenues grew 14.6%, driven by premium product development in core categories and moving into new sectors. It invested £28m in infrastructure during the year, including commissioning a pastry facility in Malton. CEO Adam Couch put its growth down to “efficient operations and really good product innovation.” Exports increased 12.8% despite the relative expense of producing UK pork, driven by quality.

LDH (La Doria)

Turnover (£m): 309

Turnover growth: 19.6%

Operating margin: 4.0%

Margin change (% pts): –0.1

The private label supplier’s near 20% annual growth was driven by volume increases in core categories and NPD. It leveraged its dominant position in private label canned tomato (40% share) and baked beans (52% share) to increase penetration – adding to its key Tesco and Asda accounts, by growing business with Sainsbury’s, Morrisons and Co-op. LDH benefited from the consumer shift towards scratch cooking but it also invested in new cardboard packaging to improve margins and help transportation.

Innocent

Turnover (£m): 206

Turnover growth: 26.7%

Operating margin: 13.7%

Margin change (% pts): +19.2

After a false start, Innocent’s successful expansion into the juice market helped it to its highest ever sales in 2012 and, more importantly, to its first profit since 2007. Having 9.6% share in juices offset its decline in smoothies (though it still has 73% share). Juices look set to overtake smoothies as its biggest revenue segment in 2013. Innocent has innovated in a more focused way in recent years, tweaking flavours and packaging in 2012 and launching new product ranges (such as Super Smoothies) and new pack sizes.

Haribo

Turnover (£m): 146

Turnover growth: 13.2%

Operating margin: 12.9%

Margin change (% pts): +0.5

Haribo continued its strong annual UK growth in 2013, with sales up £16.7m and margins rising by 90 basis points to take its share to 14.8% and strengthen its position as market leader in UK sugar confectionery. New ranges, particularly seasonal (Easter and Halloween) lines were complemented by extra marketing activity – now accounting for 21% of confectionery ad spend. Rising raw material costs mean a slight increase in price per kg, but that was also the result of smaller packs and seasonal lines.

Quorn Foods

Turnover (£m): 141

Turnover growth: 7.4%

Operating margin: 12.6%

Margin change (% pts): –0.4%

Quorn saw double-digit growth in the UK (15.8%) and Europe (16.7%) to continue its strong recent annual revenue growth since its 2011 private equity sale. Quorn was helped by the fallout from the horsemeat scandal, but the brand also benefited from wider trends related to health and sustainability. Quorn increased its share of a growing market to 24.3%, helped by significant ad investment – using Olympians Mo Farah and Rebecca Adlington – and a revamp of the core range.

Which is not to say own-label producers can’t thrive – OC&C points to LDH (La Doria) growing key accounts and maintaining margin – but here size has certainly been an advantage in leveraging scale. Those own-label producers serving big accounts without such cost advantages will find the tightening margins of the retailers a tough place to operate.

Power shift?

The unprecedented disruption of the grocery retail market is likely to bring profit pressure on many suppliers, but the balance of power might actually be shifting in their favour. The loss of power of the big four coupled with the declining number of smaller independents potentially means there are more retailers of scale that producers can address directly. The changing market also exposes them to a number of growth channels that have the potential to create value, enabling them to tailor products more acutely to different shopper needs.

Hayllar adds: “Fundamentally what the changes in the retail environment are doing is reducing the concentration of power [in terms of] the big retailers. In some ways this changing environment is probably less difficult for those companies with business models that are already better placed to access a more diverse array of channels and activating those through different pack and case formats.” He believes the disparity between the market’s winners and losers is likely to become wider, but there are several core strategies companies can adopt to mitigate downside risk.

Instead of chasing absolute scale efficiencies, producers should think more strategically about customer (and consumer) demand. It may well be more efficient to produce standardised products at the lowest cost per unit possible, but given the widening variety of channels and consumers, making identical products is unlikely to be the way to generate the most profit. The trick is to find efficiencies while creating more tailored and relevant products that can be sold for a higher price.

Commodity pressures ease

The virtual elimination of inflation from the market has done no favours to supermarkets as they’ve been unable to hide the lack of growth (indeed negative growth) in their big stores. But from a supplier perspective, not having to contend with the rampant commodity inflation of 2011-13, which drove retail prices up, will come as a relief.

Analysis by The Grocer in July showed grain prices are down by double digits year on year. Milling wheat is down 13.4% and wheat feed is down 21.17% year on year – due to an expected global glut.

EU sugar prices also fell (from €700 a tonne in 2012 to less than €600) as, worldwide, sugar is set to deliver a fifth consecutive global production surplus, according to the International Sugar Organization. With a surplus sugar mountain of 1.31 million tonnes for 2014/15, prices will be weak.

Dairy is also looking like a relative bargain. The wholesale price of milk powder is down 25% on last year, while butter prices fell 20%. Cheddar is down 10.4%.

And it’s not just food prices that are falling. Gas may have moved up following EU sanctions on Russia, and over concerns Ukraine may block Russian supplies from entering Europe, but year-on-year gas prices are much cheaper, down 35.6%.

However, it seems manufacturers take a similar line on the price of commodities to the one conservative analysts take on the global economy. At best they are cautiously optimistic. “The pressures have subsided since the impact we suffered over 2011, 12, 13 and in early 2014, but we’re always mindful they can return,” says Cranswick CEO Adam Couch. “It just takes a poor harvest for wheat, or speculators coming back into the marketplace.”

A Quorn spokesman adds that the volatility of the last few years means “net, our total costs have gone up. Even as we look forward, certain [goods] are falling like meat, but [ingredients] like eggs are going up. Unless you are tied to one big commodity, most manufacturers have seen a little bit of cost pressure.

“Some goods are clearly falling, and that might be helpful, but if you are buying across a whole raft of [ingredients], by and large everything goes up a little bit.”

“Efficiency of operations really is an obsession for us,” says Cranswick’s Couch. “But that means investing in facilities and having quality management on the ground. We’ve seen the mistakes others have made trying to cut back and centralise certain functions that don’t suit being centralised.”

Rethink products

Being able to adapt to changing consumer demands means rethinking product and pack architecture, ensuring good presence in growth formats and retailers, and investing in long-term distinctiveness.

OC&C’s Hayllar draws an analogy between the food industry and car manufacturers – these days auto firms will generally have a great amount of commonality across engines and chassis formats as they are prohibitively expensive to re-engineer. But while car firms insist on efficiencies on these costly components, they are innovating and look for differentiation around other, cheaper and more flexible aspects of production, such as body shapes.

“Like car manufacturers, food and drink producers need to be efficient at the things where there are big scale advantages, while managing to get the tailoring right in the places where it’s most valued,” he says.

Fundamentally, both grocery retailers and producers are facing urgent threats to their business models. While the temptation may be to aggressively look to deflect profit pressure on to each other, it may well be that the retailers and producers that can find common, mutually beneficial ground are the ones most able to forge genuinely successful relationships.

“You’ve got to be able to create win-wins with your customer,” says Innocent’s Lamont. “In this market you need to avoid getting into difficult confrontations with retailers, instead you need to think about how these situations can be turned into opportunities for both of you. If you can’t do that, in a difficult market you’re going to struggle.”

Retailers and suppliers increasingly need to put their heads together and work out ways to take out inefficiencies between the different steps of the supply chain to be able to keep prices in check without slashing profitability.

There is little doubt suppliers are facing the toughest grocery market in many people’s working memories. But that does not mean revenues must necessarily be squeezed and margins cut. Instead, these market disruptions create very real opportunities for those producers that can adapt fast and get it right. For those that can’t, the 2015 OC&C Grocer Index will make for even more uncomfortable reading.

No comments yet