The bagged snacks sector is a conveyor belt. As soon as a new product rolls on to retailers’ shelves, another starts to fall off.

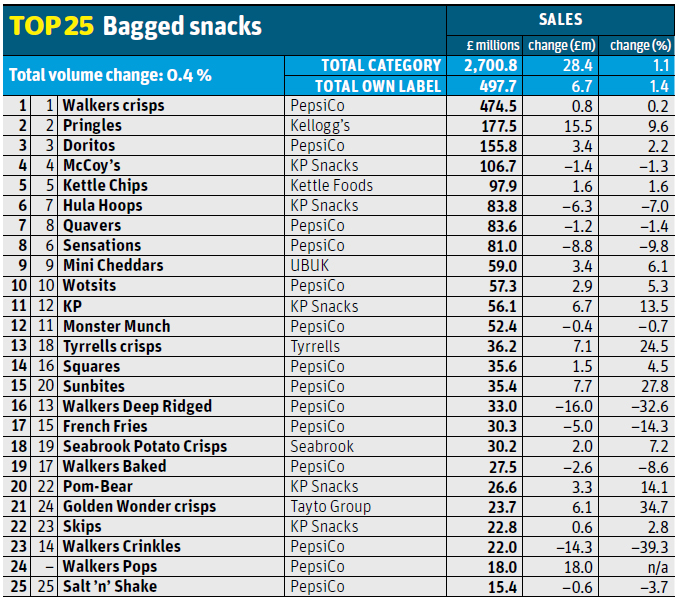

Take Walkers. Since launch in February, Walkers Pops, a low-calorie, air-popped offering, has racked up an impressive £18m. Yet that growth is undermined by the £16m losses of Deep Ridged, which hit the market in 2012 and was the brand’s star performer last year. Overall sales for Walkers have tumbled 4.1% on volumes down 4.5%. Ouch.

The decline is in contrast to the sector’s albeit rather lacklustre growth (value is up 1.1%; volume 0.4%). So who is stealing Walker’s sales? How? And what are brands such as Walkers trying to ensure their NPD has longevity in this fickle market?

Promotions are key in bagged snacks. Of the 318 million kilos of snacks Brits have munched through in the past year, 55.3% were bought on deal. That’s an annual increase of 1.4 base points. Yet average price per kilo is up, not down, by 0.6%, driven by a 0.4% rise in base price and a 1.4% higher deal price.

The rising price of singles is partly to blame. “Price rises have altered the balance of value between singles, sharing and multipacks,” says Nisa trading controller Trevor Standing. “As a result, singles appear poorer value and people are trading up to larger packs.”

As sales of singles have been hit by rising prices (for example, Hula Hoops’ volumes are down 15.6% as average prices have soared 10.1% and McCoy’s volumes are down 8.8%, with price per kilo up 8.2%), the sharing segment has cleaned up, with growth of 4.9%.

In reflection of this growth, sharing stalwart Pringles is the best-performing brand in our top 10, recording value growth of 9.6% on volumes up 13.8%, the brand’s decline in average price driven by an increase in volume-driving deals.

“Working hard with our retail partners has allowed up to deliver some fantastic in-store execution this year around key snacking occasions such as the World Cup, summer music festivals and Christmas,” explains Gavin Bowyer, UK marketing manager for savoury snacks at Kellogg’s. “What’s been happening in store has also been supported with a new multimillion-pound advertising campaign, which has run across the whole year. It’s been a huge success and allowed us to unleash the fun from the can.”

Such support is crucial, particularly when it comes to NPD, which accounted for 6.1% of the category’s sales in the past year, according to Nielsen. “Walkers Pops benefited from a substantial marketing campaign,” says Walkers marketing director Jeremy Gibson.”There have been bursts of TV advertising throughout the year, which started in March, and it has also been supported with substantial in-store activity, including eye-catching branded point of sale material and sampling that has helped drive strong sales.”

With brand owner PepsiCo putting Pops under the spotlight and reducing support for other recent launches, it seems shoppers have been quick to forget other products in the portfolio. For example, Walkers Baked Hoops & Crosses - launched in March 2013 and supported by the brand’s biggest print campaign in five years - has slumped 27.4% in value.

Deep Ridged’s growth was similarly short-lived. Walkers claimed the variant’s launch in the summer of 2012, backed by TV ads starring brand ambassador Gary Lineker, was the biggest in fmcg in three years and the biggest category launch of the decade. Now it can lay claim to a much less enviable title: its £16m decline to sales of £33m make it the category’s fastest faller of 2014.

Not that Walkers has abandoned established brands entirely. Sunbites has jumped 27.8% in value and 28.4% volume, thanks in no small part to a two-month TV campaign and activity on Facebook and Twitter, which Gibson says has attracted existing and new consumers.

While important, the waxing and waning of the fortunes of the bagged snacks market’s biggest player is down to more than marketing. Sunbites and Pops have benefited from the growing health-consciousness of consumers, while Deep Ridged has suffered from a more general move away from ridged crisps, with Walkers Crinkles down 39.3% in value, and even McCoy’s losing sales (albeit only a minor fall).

At the same time, there’s a new kind of crisp on the market. In April, Seabrook launched Lattice Cut Crisps exclusively into Asda before rolling it out to the rest of the big four. Lattice Cut now accounts for more than 10% of the brand’s sales, up 7.2% on volumes up 6.6% overall. What’s more, growth has been achieved with just a fraction of the marketing budget Walkers would typically spend.

“Walkers does big textbook launches with huge marketing campaigns and support but that is not always sustainable over a long period of time,” says Seabrook marketing director Kevin Butterworth. “We’re not a business that wants to throw things at the market and see what will stick. Instead we are incredibly customer-focused and consumer-focused and do a lot of activity in-store.”

In October, Seabrook launched Lattice Cut in 40g and 90g bags with peel-open front panels in a bid to tap growth in sharing and widen distribution into convenience and food service, where the format will be exclusively available (about 95% of the variant’s sales are currently from a supermarket, says Butterworth). Such efforts may prove crucial if mainstream brands are to avoid losing more share to premium brands in sharing formats.

That Seabrook’s peel-open packs are price-marked (40g at 75p; 90g at £1) is also significant. Others to introduce PMPs since the summer have included McCoy’s (in July) at 55p across its best-selling 35g format flavours - salt & malt vinegar, flame-grilled steak and Cheddar & onion; Bobby’s (in October), which reduced the price of its seven top-selling impulse snacks and price-marked them at 39p; and (also in October), KP nuts launched a selection of £1 PMPs in convenience.

“Sharing is set to continue growing, which will place more pressure on the rest of the fixture,” says Chris Harrison, head of commercial operations at P&H Direct. “The £1 PMP has been a key driver in impulse, growing from £35m two years ago to £67m as c-store customers seek quality and price.”

The other key dynamic continues to be quality crisps, as seen in the ongoing growth of posh brand Tyrrells, up 24.5% on volumes up 16.7%. Walkers is having another stab at the premium sector with Market Deli, which has racked up £6.6m since its July launch, helping to offset the £8.8m losses of PepsiCo’s other posh bagged snack brand Sensations.

Whether Market Deli has enough support to still be in growth in a year’s time remains to be seen. But if not, there’s another format Walkers could adopt: lattice. “That’s always the danger,” says Butterworth. “If Walkers did so we’d take it as a compliment. Of course, they’d be able to outspend us but there’s always credibility in being first to market.”

Indeed, air pop pioneer Pop Chips is up 43.5% on volumes up 50.6%, despite Walkers Pops bursting on to the scene. It seems there can still be a first-mover advantage.

Top launch: fish ‘n’ Chips Burton’s Biscuit Co

1980s favourite Burton’s Fish ‘n’ Chips returned in January following The Grocer’s Bring Back A Brand campaign (ably supported by The Sun).

More than a decade after disappearing, the savoury biscuits were reintroduced in various pack sizes - a 40g grab bag, a 5x25g multipack and a 125g share bag - and have already generated £8.6m sales (see p82). In April Burton’s invested £14.8m in its supply chain to help expand its savoury snacking portfolio (though to us they’re bagged snacks).

No comments yet