Online grocery has never been busier. In May, Amazon launched its long-awaited Fresh grocery service in the UK, underpinned by a landmark supply deal with Morrisons. A few weeks later, Sainsbury’s signalled its growing online intentions by bidding £1.4bn for tech-savvy Argos. Start-ups like Hello Fresh and Gousto are increasingly gaining mainstream traction. At the same time, shoppers are being offered ever faster, ever more convenient shopping options: one-hour slots are becoming commonplace; investment in click & collect continues apace; and tech pioneers like Amazon are even automating the ordering process now, through devices like the Dash wand.

But beneath the flurry of activity, there remains one big, nagging question: that of profitability.

It’s a question that has plagued online grocery since it first emerged in the mid-1990s, and it continues to divide expert opinion. While there are glimpses of profitability in some parts of the sector (Bernstein estimates both Tesco and Ocado reap profits of up to 3.5% and 2.5% from online orders, respectively), the overall figures - taking into account the huge sums being invested in online infrastructure - continue to be disappointing. “A hardly profitable operating model” is how Capgemini bluntly called it in a report earlier this year. And Aldi CEO Matthew Barnes famously declared last year the discounter wouldn’t move into online food selling because “no-one is making any money online”.

It’s not a sustainable situation, and retailers are under growing pressure to prove they really can make online pay. So what are the most promising strategies they should explore?

Picking and delivery are the most costly elements of the service - Bernstein calculate they swallow up £15 per order - so anything that can be done to cut this spend would clearly help profitability. Getting consumers to pick up the tab (or at least more of the tab) seems an obvious solution. Indeed, supermarket shareholders have long complained the costs involved in picking food and getting the items to customers’ homes far outweigh standard delivery charges, which largely range from £1 to £7. This is particularly the case for small online orders. “Generally, smaller online grocery baskets will not make any money overall - unless you charge for delivery - because the profit on the purchases is wiped out by fulfilment costs,” says Nick Harrison, Oliver Wyman’s European retail co-lead.

Consumer backlash

Only it’s not that simple. Tesco tried last July, when it changed the minimum spend on online orders from £25 to £40, with customers under the threshold paying a £4 surcharge on top of the existing delivery fee. But the move prompted a backlash among some customers who took to Twitter to voice their dissatisfaction - a #hardlife hashtag even made an appearance. Despite the furore, Tesco stuck with the model, but it’s risky.

Ocado’s head of retail, Lawrence Hene, is all too familiar with the difficulty of asking shoppers to pay more for delivery. The reason “all the retailers offer cheap slots today is that customers have a resistance to delivery charges”, he says. It’s one of the reasons he isn’t convinced of the new crop of start-ups offering super-speedy grocery delivery for a premium price: London-based services Togle and Convibo, for example, deliver food from M&S, Waitrose and Whole Foods Market within an hour for fees of £4.50 and £6.99 respectively, and also charge a mark-up of up to 15% on products. These kinds of charges mean such services will be relegated to the domain of distress purchases, Hene believes.

Neil Saunders, MD at Conlumino, agrees blanket charging isn’t the way forward. The level of competition in the UK simply makes that impossible, especially as new entrants will continually fight to undercut established retailers on charges. “Amazon will be keen to make a point that its delivery will be cheap,” he says. “And there’s a clear elasticity of demand. If you put delivery charges or prices up too much, volumes will drop back and that can damage profitability.”

Given how important volume is to profitability, it’s no surprise that several retailers have looked to subscription models to amass customers and better manage delivery costs. The concept is simple: loyal online shoppers are rewarded with cheaper delivery charges; one-off purchasers and those who like to shop around have to pay more, especially for small baskets.

Tesco, Asda, Amazon and Ocado all offer unlimited deliveries on orders over a certain amount for a fixed fee - with Tesco offering a mid-week subscription for as little as £2.50 a month. Bernstein says the model has driven “rapid growth” for Tesco and Ocado. On the flipside, it also drove further erosion of delivery fees; Bernstein estimates Tesco delivery charges went from contributing 4% of gross margin to just 2%.

Despite the initial hit to margin, these subscription models continue to represent one of the most promising options for online grocery operators. Indeed, the arrival of Amazon in the UK online grocery space is set to add further weight to the model. Services such as Fresh and Pantry, and the fast-turnaround delivery options associated with them, require an Amazon Prime subscription with an annual fee, cementing the idea that more convenient delivery options are something that has to be paid for - though the jury is out on whether the fees being asked for right now are high enough for the figures to stack up long term.

Further vital economies of scale can be created by getting shoppers to buy bigger baskets. “Given the costs of picking and delivering are fairly fixed for home delivery, any increase in order size adds a lot to the profitability,” says Harrison. “So if you don’t want to charge for delivery, the most straightforward way to improve the economics is to increase the average order size.”

Linking delivery charges to basket size is one way of encouraging shoppers to go for bigger shops, but so is the creation of more compelling non-food offerings, like Ocado’s recent tie-up with Marie Claire and Sainsbury’s acquisition of Argos.

Squeeze harder

But retailers also have to keep looking for operational improvements wherever they can. “Without operational excellence - lots of narrow delivery slots, high product availability, timely delivery etc - customer retention is very low and the business never reaches scale,” warns Bernstein.

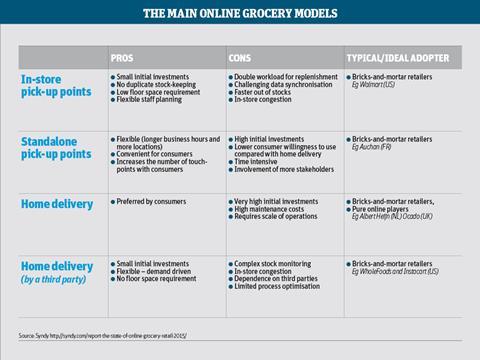

Crucially, there isn’t one ‘right’ way to be efficient: dark store, in-store picking and pure-play online models (see table, right) can all be made to work profitably, provided the right efficiencies are created. For example, Sainsbury’s (which Bernstein estimates to be breaking even) opened its first dark store last month to speed orders up after spending years using in-store pickers. Tesco, on the other hand, managed to increase its in-store picking rate from 40 to over 120 items an hour in just a couple of years through a mix of technology and sequencing shoppers efficiently, while Ocado focused on streamlining its pure-play process through patented machinery to achieve rates of up to 600 items per hour. Meanwhile, Morrisons’ renegotiated deal with Ocado, announced this week, goes big on store-picking to enable nationwide delivery (though it also means the break-even point for Morrisons.com will be delayed as a result).

The supermarkets are clearly trying to improve their online efficiencies, but Barry Clogan, a former Tesco.com chief who was tasked with rolling out Tesco.com internationally and now works for consultancy MyWebGrocer, believes they can go even further.

He points to recent technological developments, such as the green light Amazon received last month to test drones, and industry chatter about using robots to make food deliveries. “Delivery is a massive barrier to entry and profitability, so if you can get a robot to deliver £10 to £15 baskets, why not?” Clogan argues. But it is unlikely to represent the full (or particularly near-term) solution. As Clogan intimates, the technology will only apply to small baskets - and even for tiny baskets of shopping, drones are years away from buzzing up to the front door and ringing the bell.

More radical still is an idea put forward by Harrison at Oliver Wyman. He believes the current heated competition around last-mile delivery could well be a temporary phenomenon. “In the future, it is not inconceivable that government may look to regulate delivery traffic. One way to do this would be to compel retailers to use one single last mile service. Home delivery would become a utility like gas and electricity, and the ‘last mile’ would be dead as a competitive weapon for retailers.”

Click & collect

A more immediate answer to reducing the costs of the infamously expensive ‘last mile’ could be click & collect. This year Sainsbury’s plans to double its number of click & collect sites to 200. Tesco and Asda have also put in planning applications to extend their number of collection points (although Asda has scaled back on its original ambition to have 1,000 locations by 2018).

Analysts are split over consumer demand for the service, though. Bernstein believes click & collect makes online food retailing as profitable as in-store. Not only does it save retailers the £9 delivery cost, but it also appeals to customers. “From the consumer’s point of view, being at home for a one- or two-hour delivery slot is not necessarily the most convenient solution,” it says.

And the model could give supermarkets an edge over pure-play online retailers such as Amazon, says Kalle Koutajoki, CEO of consultancy Digital Foodie. “If you pick up an order at the drive-through, the process takes less than five minutes - at its most efficient, two to three,” he says.

However, critics such as Shore Capital’s head of research Clive Black believe the service only appeals to a “relatively modest” number of people compared with full home delivery, which he sees as more convenient and only slightly more expensive.

The debate shows there is clearly some way to go before the grocers find a silver bullet to make online profitable. But Digital Foodie’s Koutajoki believes everyone is looking at the problem in the wrong way. He says supermarkets should avoid looking at online as a separate channel to their in-store offering and look at the impact on their business as a whole.

“Based on our data, customers who shop online spend 2.5 times the amount of the regular in-store customers,” he says. So even if online isn’t profitable in isolation, it could be boosting the bottom line overall.

Tom Golden, marketing director of Clavis Insight, agrees being online has a wider ‘halo effect’ on all sales, because the digital channel is a “significant influencer of in-store purchases - up to 35% of in-store UK food and beverage purchases are digitally influenced, with shoppers using online for product research, price comparison and consumer review analysis”.

He also says online is “where most of the growth is coming from” in the grocery business. And the level of competition means if you choose not to offer online shopping, your digital-savvy customer can simply choose to go elsewhere.

And in 2016, customers are not something that supermarkets can afford to lose.

No comments yet