Austerity isn’t over yet. Inflation has continued to outstrip growth in average incomes George Osborne has been sharpening his knife for yet more cuts consumer confidence has remained weak. As the first green shoots of a recovering economy emerged in 2013, Britain’s grocers and their suppliers are facing up to their third consecutive year of volume declines.

But, as we reveal in the next 80 pages of analysis, for some, products sales have boomed as if the age of austerity never happened. These are 2013’s Top Products. We’ve forked out £62.5m (or 14.1%) more on Cadbury Dairy Milk, glugged down 13.1 million (273.3%) more litres of Coors Light (despite a flat lager market) and spent £44.4m more on Warburtons bread in the past year, to name just three of the leading lights of 2013.

Some retailers are resisting the squeeze, too. Not the big four their share of grocery has been eroded from 76% to 74% in the past two years by everyone from Aldi and Lidl - up 21% combined in 2013 as they continue to beat mainstream retailers on price and, increasingly, quality - to Waitrose (up 10.5%), whose widening appeal continues to win new shoppers.

See the full Top Products Survey.

So just how challenging have market conditions really been over the past year? How have the suppliers and retailers behind Britain’s top products managed to defy them? How have the events of 2013 - such as the horsemeat scandal and the long Arctic winter, followed by the hottest summer in nine years - affected grocery? And what’s the outlook for 2014?

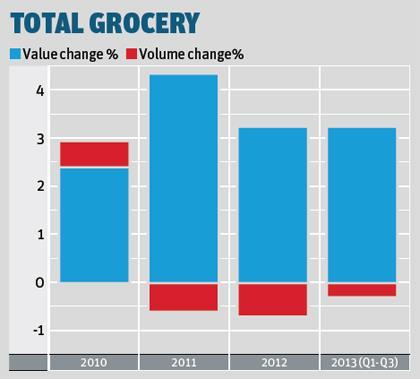

Analysis from Nielsen reveals that in the first three quarters of 2013, grocery’s value grew by 3.2%. That’s in line with the market’s growth in 2012. But while volumes are still down, the rate of decline is slowing. In 2012, volumes fell by 0.7% across the full year in the first three quarters of 2013 they slipped just 0.2%. A good Christmas could make all the difference between volume growth and decline.

The recovery is not consistent across the country, however. “It’s good to see a little positive growth, but so much of it is coming from London and the South,” says Asda CEO Andy Clarke. “If you’re in the North East, say, and on a budget, you’re not seeing this growth in your wallet or purse. You’ll read that the economy is growing, so that might have a marginal effect on your outlook but it’s no more than that.”

Low confidence

So, shoppers are still tightening their belts. “Consumer confidence is still negative, but it has increased from the third quarter,” says Mike Watkins, head of business & shopper insight at Nielsen. “Throughout the year we have seen many shoppers remaining reluctant, unwilling or unable to spend. As a result, and to stimulate demand, in-store promotions remain high at 35% of sales, the same as the previous year.”

Witness the rise of the discounters, the increasing use of money-off vouchers as a means of retaining loyalty and the growing trade Amazon is doing on certain bulk items, such as nappies and toilet roll, for proof of just how heavily price has weighed on shoppers’ minds in 2013. In this climate, those who have resisted the temptation to raise prices - or at least not as much as the competition - to offset cost inflation, have done well.

“When we talk about point-of-purchase levers, price is the key lever we pull,” says Craig Clarkson, trade & marketing director for off-trade at Heineken UK, which has enjoyed combined growth worth a staggering £73m across its biggest lager and cider brands in the past year. “Of course, we want to have other attributes in terms of brand strength to execute at point of purchase to draw attention away from price, but, particularly on the core brands, price and promotions are very important.”

The fact the average price of a litre of lager has climbed 3.2% to £2.10 in the past year, while the average price of Heineken UK’s two biggest lagers, Fosters and Kronenbourg 1664, have risen by just 1.7% and 1.2% respectively to £1.78 and £2.40 a litre, goes some way to explaining how they have defied the ongoing drain in the lager market to achieve impressive value and volume growth.

Horsemeat

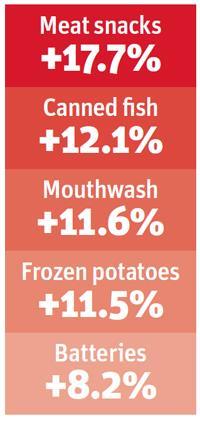

There are numerous examples of brands defying the general volume slide by keeping a tight lid on price. Famous Grouse usurped Bell’s Original as Britain’s best-selling whisky this year, thanks in part to fierce deals that saw the brand’s average price dip 0.9% to £18.24 a litre (Bell’s rose 4.7% to £18.63) Energizer has defied an 8.8% volume decline in the batteries market with healthy value and volume growth by lowering prices own-label nappies are up 37.3% on volumes up 44.5%, partly as a result of a 5.5% drop in price.

Of course, price isn’t everything. NPD has contributed £38.1m (52.2%) to Heineken UK’s growth in the past year and growing sales of pricier sub-brands Snow, Black and Naked Grouse have surely helped pay for Maxxium’s price cuts on Famous Grouse. The brand’s first TV ads outside Christmas this year can’t have hurt either. New distribution gains helped Energizer. So it’s not just about price. And now more than ever.

Our appetite for a bargain - and the upward march of commodity prices over several years - created the ideal climate for fraud. Since the first evidence of that fraud emerged - the discovery that some of the meat in a Tesco frozen ‘beef’ burger was in fact horse - in January, the repercussions have been wide.

“The horsemeat scandal has made people think about where their food comes from and the true price of cheap food”

Rachel Kelley, Charlie Bigham’s

It will come as no surprise that sales of frozen burgers tanked following the revelations. Value sales for the 12 weeks to 2 February showed a 40% year-on-year decline on volumes down 43%, with own label bearing the brunt of the decline (branded burger sales actually showed a slight increase). Further research by Nielsen found that 67% of adults were less likely to buy processed meat products as a result of the scandal.

This was remarkably prescient. Of course, brands and categories later implicated in the scandal have suffered - Findus frozen ready meals value sales are down 43.1%, and Birds Eye frozen ready meals fell 25.7%, contributing to an 8.4% category decline on volumes down 7.3% - but the rot has spread further. Volumes of savoury pastries have dropped 6.6%, for example, and everyone from chilled ready meal brands to microwaveable snack players have cited ‘Horsegate’ as an issue that’s affected them.

But the effects haven’t always been negative. Quorn Foods sales across frozen and chilled are up 7% to £129m [IRI 52 w/e 13 November] with sales in some retailers rocketing by more than 30% at the heat of the crisis - prompting it to increase production capacity. “The horsemeat scandal provided further impetus, adding about three percentage points of growth for about three months,” says chairman Clive Sharpe, “but with consistent advertising, extensions to our range, additional promotion, and new distribution wins in store becoming live, growth rates are currently tracking 10% to 20% from month to month.”

It’s not just vegetarian players that have enjoyed growth off the back of the consumer backlash. Premium meat products have prospered too. “We’ve seen growth in sales as consumers are wanting to pay more for a product they feel they can trust,” says Rachel Kelley, commercial director at Charlie Bigham’s, which has seen value and volume sales of its chilled pies more than double in the past year [IRI]. “The horsemeat scandal has made people think about where their food comes from and the true price of cheap food.”

But the trend for posher food at home had of course been growing long before the horsemeat scandal ever reared its head. Showing that our taste for the finer things in life prevails, sales of Champagne and Sparkling wine rose 7.3% by volume - although prices were depressed 0.6% in the past year, primarily by own label’s 4.9% point share gain. This swing towards own label fizz, particularly Champagne, has hit brands such as Cordoniu cava and Jacob’s Creek sparkling hard (both are down in value and volume by double digits) as prosecco has become a more fashionable alternative to Champers.

The premiumisation trend is even more pronounced in cider and perry, where volumes rose just 0.5% - a sign that the category’s astonishing growth over the past five years is finally running out of steam - while the average price climbed 5.7% , making it the fastest-growing alcohol category by value.

This isn’t just a case of inflation. It’s the posher stuff that’s driving the lion’s share of the growth. All but one (Strongbow pear) of the five fastest-growing ciders sells at a premium way above £2.07, the average price of a litre of cider in 2013. And while it’s pertinent that four of these ciders are non-standard fruit ciders (ie not made with apples or pears), meaning they do not enjoy the same tax breaks as traditional ciders, hence pushing up the price, the premium can’t entirely be explained away by tax, says Heineken’s Clarkson.

“It’s important that NPD adds value so the shopper feels they’re getting something extra, the retailer feels they’re getting something extra and we, the supplier, do too,” he says, pointing to NPD such as Bulmers Bold Black Cherry, which has sold for an average of £2.91 and racked up a whopping £10.7m since its March launch. “Again, in lager, NPD sells for an average of £2.50 against £2.13 for existing lager. It’s important we add value with NPD and that everyone feels that.”

Tastes are getting more expensive elsewhere, too. Standard gins are faltering while premium alternatives are flying (Gordon’s is down in value and volume while Diageo stablemate Tanqueray, which fetches £6.08 more a litre, is flying, albeit from a much smaller base). In ice cream, Ben & Jerry’s and Magnum continue to outperform the market thanks in part to premium NPD such as Magnum Infinity and Ben & Jerry’s Core. And in bottled water, San Pellegrino is leading the growth.

Long, hot summer

The fact we’ve glugged three million litres (23.1%) more of San Pellegrino, which sells at more than double the market average of 51p a litre, in the past year isn’t all down to our oh-so-sophisticated tastes, however. The growth, of the brand and the wider bottled water sector (up 10.6% in value 8.7% in volume), is primarily down to a more basic human need: we were hot and thirsty.

“When the temperature reaches 28 degrees, water grows faster than any other soft drinks category,” says Silika Shellie, retail channel & category controller at Nestlé Waters, which owns three of the 10 best-selling bottled water brands (Buxton, Pure Life and San Pellegrino, which have grown by £14.7m in the past year). It will come as no surprise that ice cream also benefited from the hot summer, with handheld sales up 9.6% on volumes up 5.6%. “It would be disingenuous to say it hadn’t been important - clearly, when the sun shines people eat a lot more ice cream - but it depends on the brand,” says Noel Clarke, brand director for ice cream at Unilever. “With brands like Solero (up 9.1% in value 2.2% in volume), you see a big summer spike. For Magnum (up 11.4% in value 4.1% in volume), it’s still important but slightly less so it’s more of a year-round product. We’ve had growth in Magnum since March and we had snow on the ground then.”

Clarke credits the development of new products such as Magnum Kisses and Magnum in tubs - launched in autumn 2012 and already worth £3.8m, despite the brand’s advertising focusing chiefly on handheld variants over the past year - helping to reduce its reliance on the peak summer season.

“When you look at ice cream it’s a billion-pound category but there’s no reason why it couldn’t be £2bn,” adds Clarke. “Tubs as a luxury business is the most consistently fast-growing part of ice cream for the past three years, Ben & Jerry’s is almost half of that. We have to continue growing consumer demand for it because it’s a fairly new part of the market. Magnum will bring a lot of investment and marketing support to bring people in. We’re hoping we can eclipse this year’s £4m with a bigger year next year.”

Innovation and big marketing support is crucial (Clarke claims Magnum accounts for 40% of ice cream marketing spend in the UK), especially when own label continues to challenge, as it does, in many categories. Own label is up 13.4%, compared with 8.4% for brands in handheld ice cream. And in tubs, premiumisation is every bit as strong on the own label side, in some retailers, as it is with brands.

Own label challenges

There were some marked swings in own-label share: in flu & cold remedies, which enjoyed a £48m surge in sales thanks in part to the severe winter of 2013, own label achieved value growth of 5.7% compared with 1.7% for brands.

And while soup appears to have enjoyed some benefit from the prolonged winter conditions (value is up 2.9% on volumes up 1.1%), it is own label that’s really dominated the category in the past year, surging 16.1% on volumes up 11.7%. Retailers have been promoting their own lines hard to achieve this growth, contends Afruj Miah, national account manager at Glorious!, whose parent company TSC Foods has launched a budget range of fresh soups in a bid to undercut cheaper own-label lines. “There has been a huge push in own label from all the retailers,” says Miah. “Promotional space is at more of a premium this year where the retailers are trying to drive even more profit from effectively the same space.”

“Of course, we want other point-of-purchase levers, but particularly on the core brands, price and promotions are important”

Craig Clarkson, Heineken UK

The influence of own label on brands is writ largest in the nappies subcategory, a market that many claim has become commoditised by an over-reliance on cut-price deals and a lack of genuine innovation. In the past year, own-label nappy sales have surged 37.3% on volumes up 44.5%, thanks to the development of new own-label lines by everyone from Tesco to Lidl. Brands, meanwhile, have fallen 13.6% on volumes down 18.9%, dragging the subcategory into value and volume decline.

Considering we’re supposed to be in the midst of a baby boom, that’s frustrating for P&G, whose Pampers brand has continued to decline despite its main rival Huggies exiting the market earlier in the year. “As we said this time last year, we knew own label would present strong competition and this has been the case,” says a spokesman for P&G. “We’re continuing to focus on Pampers’ role in the market to bring the latest technology and innovation to provide the best-performing products for parents.”

Brands like Pampers aren’t just being undercut by own label, however. They are every bit as innovative. Take Tesco’s launch of newborn baby nappies under its new Tesco Loves Baby banner as an example. The retailer claimed a market first in adding a wetness indicator to the nappies, adding an incentive other than price for parents to buy.

This, of course, is key. If brands are to be able to afford the marketing, advertising and promotions that growth in this challenging environment requires, and offset the increasing cost of raw materials, they need to be able to raise their top line by bringing to market new, innovative products shoppers are prepared to pay more for. And the top products of 2013 are those that have done this in spades.

Marvellous innovations

None more so than Cadbury Dairy Milk, which has launched a raft of new products including slabs loaded with Oreo and Daim chunks (and even salted pretzels and popping candy under the Marvellous Creations banner). This impressive innovation accounts for £58m of the market-leading £62.5m growth the Cadbury’s brand has achieved in the past year, and has allowed brand owner Mondelez to push up average prices by 3.8%, without adversely affecting volumes (in fact, they’re up 10%).

With the raw material costs of a bar of chocolate (particularly milk powder and cocoa) having surged 25% in the past year [Mintec], such innovation has never been more important, says Matthew Williams, marketing director for chocolate at Mondelez. “In a recessionary market, everybody would love to pay less but in reality, with higher raw material and energy costs, that’s not how you grow a business sustainably. So our focus is not just on innovation but also our core business to find ways to offer consumers genuine value that can be sustainable in terms of the bottom line as well as the top line.”

With volume increases dependent on a final flourish over the Christmas period in 2013 - which seems increasingly unlikely given widespread reports over the late start to Christmas shopping in December - the market will be looking to 2014 for a grocery-based recovery to finally take shape. With competition fierce, and structural changes altering the retail landscape in front of our eyes, that won’t be easy. But inflation is calming down. Amid so much uncertainty, it’s the least the market deserves.

See the full Top Products Survey.

Methodology

The Grocer’s Top Products Survey is sourced using data from Nielsen’s Scantrack service, which monitors weekly sales data from a nationwide network of EPoS checkout scanners and represents sales in grocery multiples, co-ops, multiple off-licences, independents, multiple forecourts, convenience multiples and symbols, online grocery retailers, online fulfilment stores (‘dark stores’) and impulse channel feeds from forecourt retailers.

Data for nappies and baby products, personal care and OTC is sourced from Nielsen’s Personal Care and Over The Counter services, which include grocery multiples, impulse and chemist trade channels.

Nielsen no longer includes estimates for Aldi or Lidl within Scantrack.

The data period for the Top Products Survey is MAT 12 October 2013.

Nielsen’s Scantrack service provides comprehensive information on actual sales, market shares, distribution, pricing and promotional activities, and is the fastest and most accurate monitor of consumer sales in Europe.

Nielsen services are constantly improved to reflect the retail marketplace, with back data being regularly reprocessed. It offers the UK’s most comprehensive read.

Table notes

Butter & margarine: includes solid oils.

Milk: includes all milk, with branded milk and dairy brands listed in the table.

Frozen pizza: category is split by sectors, including dietary, deep, light meal, restaurant-style, takeaway-style and thin.

Laundry: category split by formats (tablet, gel, powder, liquid and capsule).

Other spreads: includes chocolate, curd, honey, peanut butter and yeast/veg extract. Soup: snack pots are excluded from soup but included in instant pot snacks.

Table sauces: includes thick and thin table sauces, including salad dressing. Tea & coffee: decaffeinated variants are split out.

Copyright

The Top Products Survey data was compiled by Nielsen exclusively for The Grocer magazine and William Reed Business Media. No reproduction of this list or data within, in full or in part, is permitted for commercial use without the prior consent of Nielsen.

No comments yet