The big guns of booze are going to war over dwindling shelf space as a wave of agile and on-trend craft brands advances

Welcome to the revolution: a coming of age for craft booze. Sales of Britain’s top 20 craft brands have surged 71.9% to £124.7m; their combined growth stands at £58.2m. That’s almost twice the growth of Britain’s 20 biggest booze brands, which have seen combined sales inch up just 0.6%, putting an extra £30.3m through the tills.

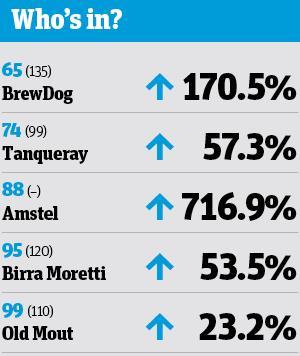

BrewDog, the brewer that swaggered out of Aberdeenshire a decade ago to wage war with the mainstream brands that it says “treat beer drinkers like brain dead zombies and vilify creativity and competition”, has stormed into the top 100 on 170.5% growth worth an extra £24.4m. It’s now Britain’s 65th biggest drinks brand. Legions of smaller brands - among them Hendrick’s gin, The Kraken rum and Innis & Gunn beer - are lining up to break into the top 100 in coming years.

Some of Britain’s biggest brands have been ousted from the shelves to make way for these newcomers. In March, Tesco more than halved the number of Heineken UK lines it stocks to clear space for higher value products. The other mults, convenience players and discounters have also cut back on traditional brands. Last month, Sainsbury’s culled more than 70 mainstream beer & cider lines.

But here’s the rub: Britain’s top 100 alcohol brands are actually in better shape than they were this time a year ago. Combined sales have grown 2.3%, pushing their value past the £9bn mark. The fastest growing individual brands are not craft; they are big global brands. So is this really a revolution, or is all this talk just a way of enticing drinkers to pay more for their booze? And who’s outgunning whom in Britain’s booze aisles?

Be in no doubt: the booze market has been turned on its head in the past decade. And not just in terms of the brands people are buying, but how they are viewing alcohol and where, when and how they are deciding to drink it. Our research shows that 41% of Brits are now actively trying to curb their drinking, up from 33% a year ago [Harris Interactive]. More are drinking at home, rather than in the pub.

This means they’re making more considered choices. “People are indeed drinking less, but they’re drinking more premium products,” says Helen Stares, client business partner at Nielsen, which produced the top 100 in partnership with The Grocer. “As competition hots up between the retailers, they’re competing on price on the high volume items but also looking to something other than price that makes them stand out.”

Hence all the range resets. Asda says it has now dedicated 10% of its existing floorspace to craft beer in a review that saw more than 100 new craft beer lines listed and an extra 40 craft spirits, including gins, rye whiskies, vermouths and tequilas.

Waitrose, meanwhile, has added another 25 speciality beers to its roster, taking its total SKU count to 95. Sales are up a third in the past year.

Meanwhile, gin at Waitrose is up more than 20%, driven largely by craft products. For the first time, gin is Waitrose’s bestselling spirit, says spirits buyer John Vine. “The fact that sales have now overtaken other spirits shows just how popular it’s become,” he says. “We’re starting to see a change in the way people enjoy gin, with many sipping it as an aperitif. That’s why local craft suppliers, who tend to enhance their gin with unique flavours and aromas, really appeal to our customers.”

Many of these brands are Davids next to the Goliaths of the top 100. Gin brands such as Sipsmith and Caorunn, brewers William Bros and Camden Town and US whiskies Bulleit and Woodford Reserve (all are in double-digit growth) are stealing share thanks to two key assets: the speed at which they are bringing exciting new products to market and the stories they tell about the quality, craftsmanship and provenance behind their products.

The master is BrewDog. “The growth we’re seeing is driven by distribution and more people coming back to buy more often,” says head of sales Steve Ricketts. “We’ve developed our range through both new beers and new pack formats to cater for many more consumer occasions. This has not only had a positive effect on our BrewDog business but on the whole craft industry.”

Similarly, the explosion in craft gin has driven growth for mainstream players. All four of the top 100 gin brands - Gordon’s (9), Bombay (36), Greenall’s (73) and Tanqueray (74) - are up in double digits. Diageo’s Gordon’s brand has enjoyed the greatest growth, with sales surging 12.6% to £213m.

“The proliferation of gin listings in the retailers has driven higher visibility and space in-store for gin, and this is benefiting Gordon’s,” says Diageo off-trade sales director Guy Dodwell. “Some areas, like standard lagers, flavoured ciders and blended whisky, have become squeezed in-store and other areas have expanded considerably.”

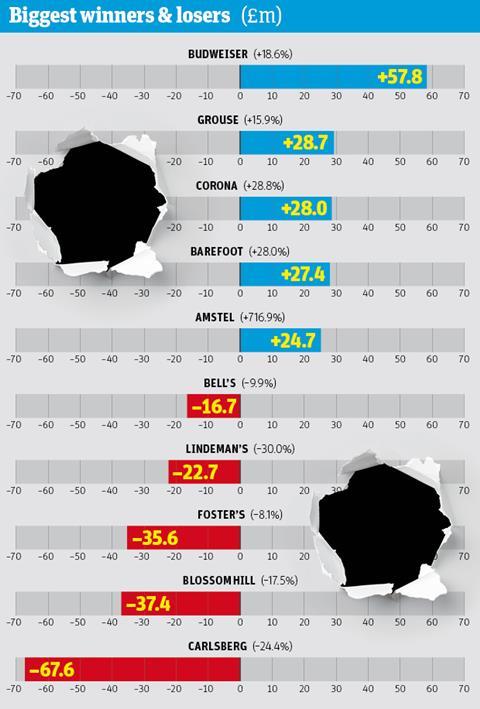

The list of this year’s biggest losers bears this out. For the second year in a row, Carlsberg (11) has suffered most, losing £67.6m as it endured more delistings after Tesco’s decision to bin it in 2015. Blossom Hill (13), Foster’s (3), Lindeman’s (51) and Bell’s (15) are the next biggest losers. They may seem disparate, but these brands have two things in common: they’re all at the lower end of the price spectrum and, arguably, little differentiates them from their rivals.

Wine has been the scene of one of the biggest culls, with some retailers’ branded SKU count having fallen by as much as a fifth. “For a number of years we saw an increase in wine brands on shelf, with similar price points and similar propositions all fighting for the same shoppers,” says Caroline Thompson-Hill, marketing director at Treasury Wine Estates, distributor of Blossom Hill and Lindeman’s, among others. “As a result, retailers have undergone range rationalisation. But it’s led to opportunities for more premium wines and wines with different propositions.”

This is a crucial point. While space is being squeezed for mainstream booze sectors, some of the biggest brands are still managing to drive staggering growth. Some are doing it by selling at a lower price than the brands that are losing shelf space. That Carling (5) is now the cheapest lager in the top 100 has helped the brand defy the downturn in mainstream lager with 1.1% growth. Grouse (10) has enjoyed the second greatest growth of the year, partly by undercutting rival Bell’s (15).

So many of the big guns of booze are defying the difficult times by mustering their considerable financial and marketing firepower. But the smartest players are doing more than just lowering prices and splurging on ads; they are working with retailers to cut the dead wood from their ranges. And there’s been plenty of that in certain categories of late.

“While fixture space for classic segments in both lager and ale is being reduced to prioritise space to the growth segments, delivering an optimised core range is important,” says Toby Lancaster, category & shopper marketing director at Heineken, which has seen huge cuts to its Foster’s and Bulmer’s (48) lineups over the past year. But he adds that standard canned brands such as Foster’s still play a crucial role in the category. “The beer category is worth £2.8bn in the grocery sector - classic lager represents 22% of this; 46% of beer shoppers buy into classic lager.”

But even those drinkers are trading up to pricier brews; see the growth of AB InBev’s Budweiser (4) and Corona (11), which have enjoyed the year’s biggest and third biggest gains, and Heineken’s Amstel (88) for proof.

Even Britain’s biggest booze brand, Stella Artois, is managing to convince drinkers that not all mainstream lagers are created equal.Overall sales have fallen 2.1% to £527m on volumes down 4%, but this is down to huge losses of space for the Cidre range and Stella 4; the 4.8% abv lager is up 2.3% to £487.8m.

“We’re seeing strong growth as premium and world lagers continue to win market share,” says head of trade marketing Jessica Markowski, who adds that Stella’s tie-ups with Wimbledon and Ascot and a greater emphasis on the bottle format have helped attract new drinkers to the 4.8% abv lager. As the image on p54 makes clear, it’s also been pushing itself as an accompaniment to food.

It’s not the only one. Newcomer Buckfast Tonic Wine (91), a brand that was linked to 6,500 reports of antisocial behavior in a recent Telegraph article, is trying to present itself as foodie brand “We’ve done a lot of food shows down south,” says sales manager Stewart Wilson. “We want to educate people on how versatile Buckfast can be.”

Pitching Bucky as a dinner party drink to the chattering classes may be too tough a sell (Wilson concedes that most of the brand’s growth is from growing distribution in England), but plenty of other big players have proved that, with a little bit of creative thinking and flexibility, drinkers can be encouraged to rethink how much a brand is worth.

Guinness (28) is perhaps the best example of this. After years of decline the brand has been given a shot in the arm by the new craft beers brought out under the Brewers Project. “Smaller craft brands have been amazing at adapting their ranges,” says Diageo’s Dodwell. “It does put pressure on your supply chain and innovation function, but this is something big brands have to get better at.”

So the big brands need to emulate the craft. But there also comes a time when craft has to adopt mainstream tactics. For the first time this year BrewDog, which had hitherto used guerilla marketing and publicity stunts (like driving a tank through London or serving beer in roadkill), paid for advertising.

That shows just how far craft has come.

Download the PDF version of this report

![]() Britain’s Biggest Alcohol Brands 2017

Britain’s Biggest Alcohol Brands 2017

Downloads

BBAB 2017 Full PDF Download

PDF, Size 10.71 mb

Britain's Biggest Alcohol Brands 2017: the battle for the booze aisles

The big guns of booze are going to war over dwindling shelf space as a wave of agile and on-trend craft brands advances

Currently

reading

Currently

reading

Britain's Biggest Alcohol Brands 2017: the battle for the booze aisles

- 2

- 3

- 4

- 5

- 6

No comments yet