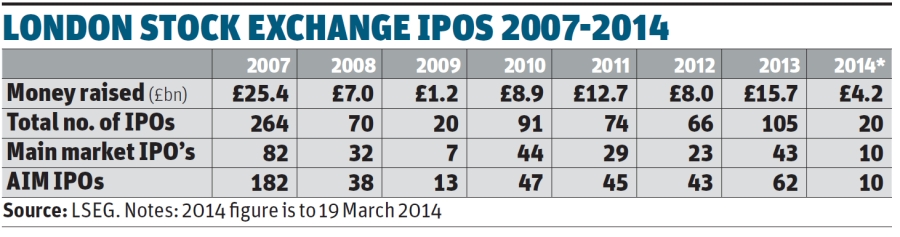

It started out as a trickle. Then it became a steady flow. Now it’s well on the way to becoming a torrent. But although the number of IPOs in 2013 were the highest since 2007 - and have continued apace in 2014 - many financial experts fear the tap could be turned off at any moment.

With many of the recent IPOs being in the retail space and another 60 companies looking to float before Easter, according to a source, the market appears to be adopting a “herd instinct”. And that means there’s a real danger that the heat will be taken out of this market before it has really caught fire, with some IPOs undertaken so far in 2014 already falling short in terms of pricing expectations.

So will 2014 turn out to be the year of the retail IPO as some finance experts predict - or will it be remembered for being an irrational bubble?

The conditions for an IPO haven’t been this good since 2007. Consumer confidence is slowly but surely returning and the UK economy is on track to exceed its pre-recession peak this summer, according to the British Chambers of Commerce.

“Obviously these are dream conditions for retailing IPOs, with the re-rating of the general retail sector coinciding with the much-vaunted pre-election economic recovery, low interest rates and tons of institutional cash,” explains retail analyst Nick Bubb.

“It is hard to construct a strong story around suppliers to the UK supermarkets”

City source

This is underlined by some of the recent IPOs undertaken by businesses that had been put up for sale previously and failed to get the valuations hoped for. Now these same businesses are going for eye-watering numbers via the public markets and this in turn is encouraging private equity groups with retail assets on their books to look at the possibility of an IPO, in an attempt to capitalise on the pent-up demand for their stock, says Bubb.

“The fund managers grumble about private equity-backed retailers being foisted on them, given the history of Debenhams, but the sector is in urgent need of fresh new blood to replace tired old stalwarts like M&S, so the retailing IPO has plenty of legs in it,” he explains.

But for retailers that got IPOs underway, it’s been a bit of a mixed bag. After the successful flotation of Bargain Booze franchise Conviviality last summer, c-store chain McColl’s, the first retail IPO of 2014, finally set the price for its IPO at 191p per share, valuing it at c.£200m - some way short of the £225m market value it was aiming for.

“McColl’s was odd in that it was not very successful, despite the apparent attractions of c-stores,” explains Bubb. “I guess investors were worried about the supermarket competition and saw more exciting IPOs coming down the line.”

Russian hypermarket chain Lenta also failed to excite investors. It floated in late February with an IPO price of $10 per share - at the lower end of its projected price range - with shares taking a further hit on their first day of trading thanks to the turmoil in the Ukraine.

Bucking the trend

However, with the three listed supermarkets effectively “uninvestable” according to Shore Capital analyst Clive Black, investment fund managers and hedge funds are on the lookout for new retail plays. “Fund managers that have seen capital inflows and the value of their stocks appreciate are open-minded to diversifying their portfolios rather than fuelling further share price growth by buying more of the same,” says Black. “Therefore, there is a strong appetite from investors for new issues, too.”

And one that’s definitely caught the imagination is Poundland, whose IPO price of 300p was at the upper end of its price range, valuing the discounter at £750m.

As Bubb points out, in the US, investors can leverage the discounter phenomenon through Dollar Tree, Family Dollar and Dollar General - “all huge chains, nibbling away at the market share of Wal-Mart and the drugstores.” And the Poundland IPO has also been sold into the US investor base. Another City source also values its transparecy. “It has a strong and clear strategy, good growth opportunities in the UK and internationally, and good, experienced management,” he says.

The most eagerly sought after IPOs in 2014 to date have been for online retailers like AO.com and Boohoo.com. Both achieved valuations at the upper end of the IPO price range, causing some City analysts to express fears we could be on the verge of another tech bubble.

But though the start of 2014 has been particularly active on the retail IPO front, we’re still a long way short of pre-recession levels. “If you go back to 2006, there were more than 100 main market IPOs that year and over 450 on AIM,” says Stephen Nash, partner in Eversheds corporate group and head of its public company takeover group. “The market is nothing like as frothy as that - it’s just looking a lot more positive than it has done for the last three to five years.”

That’s why a number of businesses are hedging their bets and looking for private buyers at the same time as pursuing a float. “Private equity groups are running dual-track processes at the moment,” says Nash. “They’re looking to either IPO or to sell, and they’re running both processes in parallel to see which generates the better valuation. A lot of these are ending up with an IPO as an exit rather than a sale, whereas over the last five or six years a lot of people didn’t even bother to run that process because they knew it would end in a sale.”

2014 retail flotations

McColl’s

Who: convenience retail

Floated: February 2014

IPO price: 191p

Float valuation: £200m

Multiple*: 16

Current price: 182p

AO.com

Who: online electricals

Floated: February 2014

IPO price: 285p

Float valuation: £1.2bn

Multiple*: 61

Current price: 349p

Pets at Home

Who: pets retailer

Floated: March 2014

IPO price: 245p

Float valuation: £1.23bn

Multiple*: 17

Current price: 245p

Boohoo.com

Who: online fashion

Floated: March 2014

IPO price: 50p

Float valuation: £300m

Multiple*: 26

Current price: 67p

Poundland

Who: fixed price discounter

Floated: March 2014

IPO price: 300p

Float valuation: £750m

Multiple*: 17

Current price: 374p

* Based on P/E to 2015. Source: Nick Bubb

One company rumoured to be exploring this dual-track approach is United Biscuits (UB), which has recently been linked to a float rather than a purchase by a private equity group or a rival food group. However, a City source thinks it unlikely. “Brokers are talking it up, but I think it unlikely. There are unhelpful precedents in terms of Premier/RHM and it is hard to construct a strong story around suppliers to the UK supermarkets.”

Investors can pick and choose

And while there is a certain exuberance in the market following the re-rating of the general retail market, it’s not the case that investors are acting irrationally, argues Nash: “Institutions can afford to be a little more choosy about where they invest today. In 2006, banks and brokers were bringing in companies that should not have been on the market and were still raising funds. Although valuations have picked up, they are still realistic and institutional shareholders are not investing in poor-quality operations.”

There isn’t a shortfall of potential IPO contenders for these hedge funds to take a slice of either, according to David McCorquodale, UK head of retail at KPMG.

“Value retailers, category killers and online players may catch the headlines, but the convenience space, with McColl’s and Conviviality Retail, has already got in on the act. Some offer good equity growth, others offer dividend yield, which is also important on the public markets. And for some, an IPO could be transformational and provide the investment the business needs to take it to the next level.”

Part of the urgency to list at the moment is out of relief. It’s also fuelled by the fact that the IPO window won’t be open forever. But that’s not to say retailers should rush to get their own flotation underway, McCorquodale cautions.

“Those first out of the gates may gain a competitive advantage over latecomers, but only if they are adequately prepared and have their house in order. Rushing to list and skipping parts of the preparation process means grocers could risk a failed listing, and the associated reputational damage.”

No comments yet