As inflation continues to dominate headlines, grocery is starting to feel the real impact. With ONS CPIH figures reaching another record high of 8.2%, latest IRI data shows that June saw the highest leap in UK grocery prices since the start of 2022. A record 1% leap in four weeks took total fmcg inflation to 7.5% to-date this year.

Within this, the categories that experienced the highest price increases were canned soup, beans, pasta and cooking oils.

Digging deeper into these increases and shopper behaviour, these are the trends we are seeing:

Branded promotions

Over the latest four weeks, unsurprisingly we are seeing shoppers navigate the increase in actual cost on branded products by seeking out cheaper alternatives – notably via those on promotion. Through choosing cheaper, promoted products, the rise in price per unit at the tills has been muted – at 3.2% for branded products.

Higher private label inflation

Across private labels, there is some softening of the inflationary impact through changing the mix of products, but that depth of promotion is not available. As a result, when you compare the actual prices paid on branded products versus private label products in the past four weeks, you can see the actual inflationary increases on private label are twice that of brands.

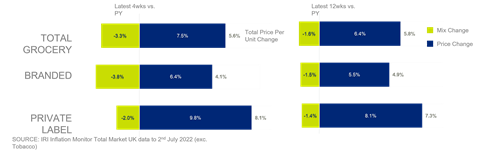

Private label is up 8.1% and 9.8% over 12 weeks and four weeks respectively, while branded goods are up 5.5% and 6.4% respectively (excluding tobacco)

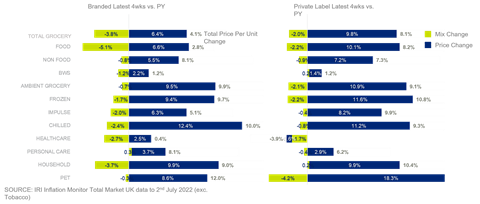

When you go deeper and look at this at category level, there is an even more pronounced increase in prices at private label versus brands across food categories.

Taking the latest 12 weeks compared with the previous period within food, excluding discounters, the percentage of volume sold on promotion has increased 2.3% for branded products, while in private label this has reduced by 5.6%.

Less deep promotions

The actual depth of promotion has decreased across both brand and private label, with percentage price reduction down by 5.1% for all food, though within brands this reduction is slightly lower at 4.5%. We see private label cutting the amount of discount by 7.3%.

The HFSS factor

Looking ahead, we can all expect to see further changes in October with HFSS legislation coming into effect, whether that be via shopper demand or retailer responses to the regulations. It is fairly safe to expect increased promotional activity for non-HFSS products, as manufacturers and retailers look to make the most of space previously given to competitor categories or products. There will also be changes to the types of promotional activity we see, moving away from volume deals and focusing more on discounting – a potential benefit to shoppers due to the current pressures.

How that translates into demand will be key. We’ll be sure to keep a close eye on expected changes.

No comments yet