The latest top 50 report shows organic growth is returning. How have the global giants managed it?

After years of tinkering with the model, the world’s biggest consumer goods companies have finally hit upon a formula to drive previously elusive organic growth.

Having been besieged by activist investors, cost-cutting mantras, economic stagnation and customer disloyalty, the OC&C/Grocer Global 50 study of the world’s largest fmcg companies has found real internal growth is beginning to return.

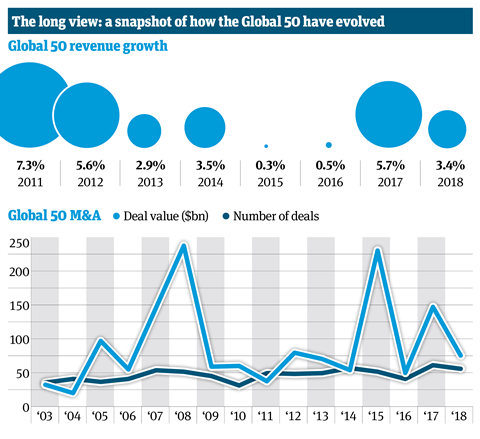

The rate of headline revenue growth across the Global 50 in this year’s study fell to 3.4% from 5.7% after the previous year’s figures were bloated by $145bn of dealmaking.

Crucially though, organic growth was at its highest level for three years at 3.2%, with the majority driven by volume as the measures taken by consumer giants to fight back against insurgent competitors and fragmenting consumer demand have started to bear fruit.

Organic year-on-year volume growth across those Global 50 companies that split out such figures was 1.8% - well above global population growth of 1.1% - after a number of years of falling behind this metric.

“It’s an encouraging sign that organic volume growth is rebounding quite strongly as it’s been pretty elusive for these big players over the last few years,” says OC&C UK managing partner Will Hayllar.

Of the 20 consumer groups to split out organic growth, only General Mills failed to achieve any, with 16 of the 20 posting some measure of volume growth.

“That’s not necessarily driven by an improvement in overall market conditions,” adds Hayllar. “It is more a reflection of the actions these big companies are taking that are starting to have benefits in terms of their ability to capture the growth that is out there in the markets.”

In the most recent times of feast for the industry, emerging market growth in particular has been a tide that raised all boats. Now individual players are having to work much harder to drive growth and some key players are finding a winning formula.

Most notably, the consumer giants have started winning back some of the share they lost to smaller, more on-trend rivals by investing behind their brands and adapting more successfully to rapidly shifting tastes.

“We are seeing more effort to step up product innovation to address different trends in the market, most notably the growth of health and wellness,” comments Liberum analyst Robert Waldschmidt. “It has taken a few years, but now we are seeing more big players getting into things like clean label and reduced sugar content, while big food is starting to realise they need to have more of a story in order to get younger consumers.”

Michael Collinson, MD in Houlihan Lokey’s consumer, food & retail group, agrees: “In general the effectiveness of product innovation, including relevance of innovation and speed to market, looks to have improved in the last year compared to, say, four and five years ago. Overall, innovation has stepped up its role in the portfolio mix.”

Growth outside grocery

This innovation also encompasses efforts to address the increasing proportion of growth happening outside grocery channels, whether that is the growing power of e-commerce in the beauty market, direct to consumer possibilities in packaged goods or the growth of foodservice, convenience and takeaways in food and drink.

Coca-Cola is one of the poster children of this organic turnaround as it has overcome stagnant sales of its core Coke brand to drive strong organic growth of 5% through investment behind more on-trend lower-sugar alternatives. In so doing it has targeted young consumers through digital campaigning and launching niche premium products like Swiss water brand Valser in growth categories.

“After a number of years of tweaking recipes and not really doing much else, Coca-Cola has really stepped up innovation and realised they are not just a carbonated beverage company,” Liberum’s Waldschmidt says.

“I wouldn’t overstate the extent that the industry is truly seeing sustainable higher underlying growth”

However, for every Coca-Cola there is a Kraft Heinz, General Mills or Mondelez struggling with sinking share prices and stagnant sales. “If you haven’t made those adaptations, it’s still going to be a pretty tough market,” concludes Hayllar.

“I wouldn’t overstate the extent that the industry is truly seeing sustainable higher underlying growth,” cautions Rothschild & Co’s global head of consumer Akeel Sachak. “There are certainly more divergent experiences between companies and the challenges they face, particularly in delivering sustainable top line growth continue to be material and quite complex.”

For all the progress some key players have made in developed markets, there is little doubt western markets, particularly in Europe, continue to lag behind other geographies.

While the boom times in emerging markets may be over, a significant proportion of global growth is still dependent on emerging territories. “Clearly emerging markets have become a more benign environment again, with conditions stabilising in Russia, Brazil and something of a rebound in Asia,” notes Moody’s analyst specialising in beverages Ernesto Bisagno.

In particular much of the growth in the Global 50 is driven by Asia-based companies, which have grown from just seven constituents in 2008 to 13 a decade later, accounting for 15% of total sales. While the majority of these Asian giants are based in Japan, China now boasts five companies on the list - with four out of five of them growing at double-digit rates.

Moody’s consumer packaged goods analyst Lorenzo Re suggests this more benign global macro-economic environment could turn once more, with the ratings agency modelling weaker global economic growth in 2019/20 - including a potential slowdown in emerging markets like China, which has also been a major driver of sales growth for western giants like Nestlé, L’Oréal and Danone.

Some sectors have also got to grips with winning back market share in rapidly changing markets better than others. While tobacco remains the fastest growth sector at 8.8% due to M&A, food and drink grew at a solid 4.3%, largely driven by organic growth and in line with the 4.6% global growth of the wider market. Beer and spirits too recorded improved performance of 1.8%, slightly higher than the overall sector growth.

However, household and personal care growth of 3%-3.5% remains behind wider market growth as the Global 50 continues to lose share to smaller companies.

The beauty area of personal care remains very strong, but household and the more commoditised end of personal care continues to struggle to find growth drivers. Hayllar suggests such producers are finding it “harder to engage consumers emotionally and encourage them to premiumise”, while the strong defensibility of big brands has also made it harder for insurgents to enter the market and drive some of the innovation-led growth that has seeped into other Global 50 categories.

M&A activity has barely moved the needle on headline growth last year, but the impact dealmaking has had on organic growth should not be underestimated - potentially puffing up some of those numbers over and above the real picture out in the market.

While the 2018 Global 50 was a picture of large-scale M&A boosting the top line, the 2019 report shows strategic portfolio management - in particular sales of low-growth assets - has helped beef up organic growth. There were nine Global 50 divestments above $500m last year, led by two billion-plus deals as Nestlé sold off its US confectionery arm and Gerber Life Insurance.

The logic behind these asset sell-offs - with Unilever similarly selling its spreads business and Coca-Cola shedding bottling operations - is to sharpen focus on core business areas and optimise the portfolio. But it also has the added benefit of increasing organic growth just by virtue of shedding low-growth brands.

Read more: Organic growth makes return to the world’s largest fmcg players

“Many large-cap corporates have a few very fast-growing businesses counterbalanced by a bunch of others that are not growing at all,” Rothschild & Co’s Sachak notes. “Take these out of the equation and the top line looks better, but it doesn’t mean anything has fundamentally changed.”

This refocus towards growth assets has also driven what M&A there has been across the Global 50. Deals conducted by these global giants fell by 48% in value terms back to $75bn as blockbusters such as AB InBev’s 2015 acquisition of SAB Miller have fallen out of fashion.

“The biggest driver of M&A has turned towards companies looking to adapt their portfolios and get into or scale up operations in category areas experiencing higher growth,” Hayllar says.

The biggest four deals last year all share this motivation, with Altria buying a big stake in Juul to ramp up in fast-growing tobacco alternatives, General Mills moving into premium petfood and Nestlé and Coca-Cola buying a share of the global coffee market.

These mid-sized acquisitions are complemented by the raft of Global 50 venture capital and incubator programmes buying up fast-growth brands for Unilever, Danone, Reckitt Benckiser and Coca-Cola, as well as deals for direct-to-consumer businesses such as Nestlé’s acquisition of Tails.com or Unilever’s of Graze.

Their motivation for M&A has also shifted from geographical expansion towards strengthening existing market positions. Some 48% of deals by volume conducted last year were done on that basis - compared with just 27% in 2017.

There is no lack of deals being done - indeed, the 55 deals completed was only marginally down on the 60 of the previous year. But the nature of these high-growth companies in on-trend sectors, while nudging the dial, is having a less transformative impact on the top line.

“Global players want to buy in innovative products and thereby growth, as well as skills, so almost by definition these are smaller targets rather than larger deals where the prime motivation is taking out costs,” says Houlihan Lokey’s Collinson. Such deals are not without risk, he notes, given the challenges of large global businesses becoming custodians of small, fast-growing brands with very different cultures. But if all goes well, the returns can be very sizeable.

At a glance: the biggest deals of 2018

A key driver of M&A for the Global 50 has been the desire to claim a slice of fast-growing global categories outside core packaged goods.

The structural growth of the $146bn global premium coffee market has seen a wave of consolidation, led by Nestlé and JAB, but Coca-Cola’s bold move to acquire Costa Coffee heralds the arrival of a new force in this area. Another key trend has been the desire for pharma companies to shed their consumer assets to focus on drug development, meaning consumer healthcare brands are finding new homes in the portfolios of fmcg giants, which can then benefit from their marketing, retail and distribution expertise.

Target company: Juul Labs

Country: US

Bidder: Altria Group

Value: $12.80bn

The US-based manufacturer of e-cigarettes received a $12.8bn cash injection for a 35% stake from Marlboro maker Altria in December 2018. San Francisco-based Juul is the market leader in US vaping, with the Altria investment expected to boost its distribution in more traditional retail channels as tobacco sales decline.

Target company: Blue Buffalo

Country: US

Bidder: General Mills

Value: $7.94bn

General Mills made an $8bn bet on the fast-growing premium petfood market in February 2018 in a bid to inject growth into its portfolio. The US food group plans to roll out new natural products in pet treats and wet food for dogs and cats. Its most recent trading updates show strong growth in its new asset, while food sales continue to falter.

Target company: Starbucks

Country: US

Bidder: Nestlé

Value: $7.15bn

Nestle paid over $7bn to acquire the rights to Starbucks’ global fmcg business to reinvigorate its own retail coffee portfolio. The May 2018 agreement significantly boosted Nestlé’s presence in the growing North American coffee market. It launched a new range of 24 Starbucks-branded products in February 2019, including Nespresso capsules.

Target company: Costa Coffee

Country: UK

Bidder: Coca-Cola

Value: $5.07bn

Coca-Cola raised eyebrows with its move into the retail sector after agreeing to buy the UK-based Costa Coffee chain from Whitbread in August 2018. The other prize is the Costa Coffee brand, which Coca-Cola is poised to use in retail and foodservice channels to win a portion of the fast-growing global category in developed markets.

Target company: GlaxoSmithKline Consumer Healthcare

Country: India

Bidder: Unilever Hindustan

Value: $4.78bn

An all-equity merger between Hindustan Unilever and GSK’s Indian-based consumer health business was agreed in December 2018. The real prize was GSK’s Horlicks brand, dominant in the region, significantly boosting Unilever’s presence in consumer health and emerging markets.

M&A caution

However, the trend for smaller deals points to a growing industry cynicism around the benefits of large-scale synergy driven M&A such as the mergers between Kraft and Heinz or AB InBev and SAB Miller, both of which are showing mixed growth prospects since integration.

Sachak points to “more caution around value-destructive M&A” and how “M&A isn’t necessarily the answer to a company’s problems”. He suggests the prevalence of activist shareholders in the consumer goods sector has made boards more “thoughtful and discerning” over M&A options.

And that is just one way the appearance of these activist investors on the shareholder registry of fmcg giants - including Procter & Gamble, Nestlé and Campbell Soup - has affected thinking across the industry.

Shareholder pressure was a key motivation behind the more active approach of portfolio management at Unilever and Nestlé, and their decision to sell off underperforming, if profitable, businesses. Perhaps most notably, these activists have prompted boardrooms to take a more aggressive approach to shareholder returns - in particular stepping up efforts to improve margins.

So far the industry is delivering on the bottom line, with the Global 50 posting its highest collective EBIT margin result in history - improving by a further 0.4 percentage points last year to 18.2%, a significant jump from 16.4% just two years ago.

Part of this improvement is undoubtedly attributable to the industry’s well-publicised cost-cutting drive in recent years - inspired by the early successes of 3G Capital’s margin-inflating zero-based budgeting (ZBB) formula at Kraft Heinz and AB InBev. Twelve Global 50 companies have publicly signed up to the ZBB mantra - where every cost has to be justified on its own merits each year - and a number of them have shown strong margin improvements. Two of the four biggest margin improvements were seen by ZBB converts Coca-Cola and Mondelez last year, with fellow disciples AB InBev and Unilever also in the top dozen.

“Zero-based budgeting is not a panacea. I would say the understanding of it is maturing”

But performance has been mixed, with margins at Grupo Bimbo, Diageo and General Mills contracting despite their ZBB approach. ZBB poster child Kraft Heinz had a disastrous year too, with huge writedowns, stagnating earnings and a 45% share price crash.

“The trailblazing of those 3G-owned business in terms of the magnitude of the cost cutting they achieved has reset some of the ambitions of other players,” Hayllar says. “But zero-based budgeting is not a panacea that solves every problem and if you do it too aggressively you can exacerbate them.”

He notes that the mentions of ZBB in the annual reports of Global 50 companies has fallen by around 60% year on year - suggesting that the balance between cost-cutting and investment in growth has moved back towards the latter.

Sachak notes: “The easiest thing in the world for a consumer business is to grow profits and cashflow in the short term by cutting what is perceived as discretionary investment in marketing and NPD. But the benefits of doing that are something of a mirage.”

At the moment it does not appear that the Global 50 are merely inflating profits by cutting marketing, with weighted average marketing spend as a proportion of revenue up 0.1 percentage points to 10.3% year on year and R&D spending remaining at 1.1%. But adopters of ZBB have consistently grown organic revenues at a slower rate compared with non-adopters - the latter up by 3.3% last year compared with 2% for the ZBB stable.

The evolution in thinking on cost-cutting suggests topline growth is no longer seen as a secondary consideration to profit. “Those companies that will succeed in the longer term are those that have consistently invested in marketing and innovation,” says Sachak.

Importantly, cost-cutting has only been one part of margin improvement, with the bottom line also boosted by a benign environment in terms of global commodities and input cost inflation and the efforts to tailor product portfolios towards premium products.

This premiumisation trend - driven by buying up premium high-growth brands as well as internal portfolio shifts to drive customers towards more expensive products and ranges - is largely generating higher gross margins. It is little coincidence that as annual report mentions of ZBB and costs fall, mentions of premiumisation have risen by more than 20%.

In short, despite myriad challenges, the Global 50 has managed to find a way to achieve headline growth, organic growth and profit growth. The big question now is whether this situation is sustainable. The demise of fundamentalist ZBB augurs well, as does increased focus on portfolio management towards growth assets and the maintenance of marketing spend.

However, with global economic growth forecasts remaining mixed and consumer tastes continuing to fragment, life will not get any easier for these global consumer players. At least now a more balanced approach to innovation, investment and growth sets them up better for the fights ahead.

In focus: how Chinese commerce is driving global growth

While overall emerging markets growth has flattened somewhat in recent years, the continued strengthening of the Chinese consumer market remains a key driver of global growth for the whole industry.

As China’s 1.4 billion-strong population gradually become more affluent, the centre of gravity of the whole Global 50 is shifting towards Asia.

There are now 13 Asia-based companies in the Global 50, accounting for 15% of total sales, with five of those now China-based (there were zero as recently as a decade ago).

These companies are also growing at a faster rate than the rest of the industry - with four of the five Chinese companies growing at over 10%, compared with average sales growth of 2.5% across the Global 50 from 2008 to 2018.

The growing buying power of Chinese consumers has been tapped by international firms, most notably spirits players such as Diageo and cosmetics companies like L’Oréal. But recently demographic shifts are suiting more local players.

“While the market for luxury goods has slowed dramatically in recent years, there is still strong growth for decent quality but affordable packaged food and drink products,” says OC&C’s Will Hayllar. “The fastest growth is now outside the big cities and that’s where large local business are much better set up to extract growth than international players.”

Some of these local players, such as Moutai and Yili, are taking advantage of the long-term trend of increased consumption to grow into players of genuinely global scale. OC&C partner and China specialist Adam Xu says: “The total volume growth of consumer goods in China is slowing down, but within these markets the winners are taking more share.”

International companies have made little headway in food and drink, where local tastes have meant local players dominate.

However, Chinese growth is being largely driven by some of the same trends as in the west - price rises, premiumisation and health and wellness.

Xu says the growing health trend in China is “very important”, though it differs from the west in that it is focused on nutrition and supplements rather than sugar or free-from eating - meaning local players are again best placed to capitalise.

No comments yet