Food and drink is under siege from activist investors, their influence running through small brands all the way up to global corporations – so who are the biggest players worming their way into boardrooms across the globe?

The barbarians are not just at the gates of fmcg. They have breached the city walls and are causing havoc in boardrooms across the kingdom. Global businesses once thought too big to pop up on the radar of activist investors are under siege.

Nestlé, Unilever, Hain Celestial, Campbell Soup and Procter & Gamble are just a handful of the mega-corporations to be targeted in the past two years.

Every PLC is fair game: Premier Foods CEO Gavin Darby has finally thrown in the towel at the beleaguered supplier following months of sustained pressure from Hong Kong hedge fund Oasis Management. Whitbread agreed to sell Costa to Coca-Cola for £3.9bn in August after pressure from Elliott Management and Sachem Head to separate the coffee chain from the Premier Inn business. And Unilever, while fighting off a £115bn hostile takeover from 3G/Warren Buffett last year, rapidly announced more ambitious growth targets, tried - and failed - to move its headquarters to Rotterdam this autumn following further investor unrest.

“When the growth stops these companies are not as good at shaving overheads and keeping it as lean as possible,” says former United Biscuits CEO Jeff van der Eems. “Activists are adept at sniffing out these opportunities and start knocking at the door.”

53

Instances, by 45 shareholders, of activism in global food & drink in 2017, says Grant Thornton

$40bn

The record amount deployed by activists in new campaigns in the first half of 2018, says Lazard

130

Board seats won by activist shareholders globally in all sectors in the year to date 2018, says Lazard

805

Companies targeted globally (all sectors) by activists in 2017, 10% consumer, says Activist Insight

Retailers haven’t been immune to activism either, albeit with less success: a handful of Tesco and Booker shareholders agitating unsuccessfully for a higher price in the merger of the UK’s biggest supermarket and wholesaler. Morrisons was leaned on by Elliott in 2014 to sell off its property portfolio. And Whole Foods Market fell into the hands of Amazon after Jana Partners built a sizeable stake in the natural food retailer.

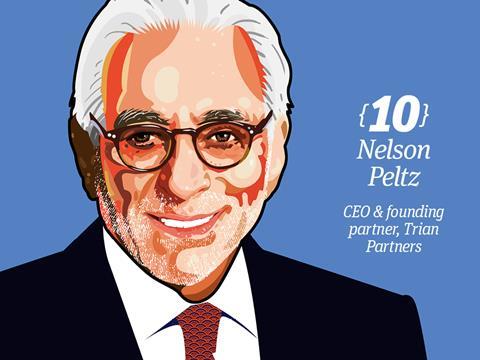

So why is food and drink so vulnerable to activism? Seasoned activist Nelson Peltz spelled out the issues facing the industry in a 94-page document criticising P&G during his mammoth proxy battle with the company. Consumers, particularly millennials, distrust big brands and are seeking out “purpose-led” alternatives, he says, alongside the “hyper-growth” of natural, organic and wellness. The rise of digital tech and social media has also levelled the playing field between small and big brands.

Gavin Davies, head of the global M&A practice at Herbert Smith Freehills, says once activists have spotted a theme that works in a sector they will return again and again. “Activists seek out value in listed companies, whether by balance sheet restructuring, encouraging corporate events or through business turnaround, wherever they see the most valuable opportunity.”

Although activism is nothing new in the consumer packaged goods industry, one player has arguably been more influential than any other in recent years.

Power list 2018: who’s steering the public’s mood about food?

“3G Capital changed the game,” says Neil Sutton, global head of consumer markets at PwC. “The industry and investors saw that 3G was able to apply ruthless cost management to very big global consumer goods businesses and saw rapid and significant improvements in profit margins. It proved nobody is too big for activism or investment.”

There was also a surge of interest in food and drink following the Heinz deal in 2013, and its later merger with Kraft. Activists such as Bill Ackman at Pershing Square Capital Management and Daniel Loeb at Third Point have made big bets at the likes of Mondelez and Campbell’s in the hope they can push them towards being the next 3G target.

Since the misjudged tilt at Unilever though, 3G has had little luck, with top-line growth stalling, a share price in decline and aggrieved shareholders shouting for action. It is grist for the mill of sceptics who warn excessively cutting costs ultimately erodes market share and starves companies of the oxygen needed for brand-building.

“There is fierce debate about the effectiveness of the 3G model,” says Will Hayllar, global head of consumer goods at OC&C. “The rebuttal of 3G - and other activist approaches - from management is to say ‘we do need investment to drive sustainable growth and we are confident we will deliver on that’. It is the counter-argument Unilever laid out to its investors to defend against 3G.”

Unilever CEO Paul Polman has long banged the drum for focusing on long-term sustainable growth rather than obsessing on the quarterly financial cycle in which public companies are trapped. And Nestlé, under pressure from Daniel Loeb’s Third Point, is desperately seeking to balance cost cutting and profit chasing with investment and future growth. CEO Ulf Mark Schneider told shareholders at a company annual meeting: “Many companies are focusing on radical cost-cutting to deliver higher profits in the short term. This approach is not sustainable.”

Akeel Sachak, global head of consumer advisory at Rothschild, says top-line sales growth is needed to sustainably create value in the long term, but that comes at the expense of short-term margin and cash generation.

“For better or worse the short-term market view towards shareholder value creation, plays into the hands of activists,” he adds.

All that said, the image of the old corporate raiders out to gut companies and run has softened considerably as activism has evolved, with recognition that these investors have an important role to play in business too - lighting a fire under big institutional investors who in the past have traditionally refrained from voicing their concerns in public.

“To have good corporate governance you need something on the other side of the board coming from investors,” Gavin Davies says. “Institutional investors and other shareholders are becoming more prepared to air their concerns, or to lend their support to those who will, when they feel their concerns are not being registered by management.”

Social media power list: grocery’s biggest influencers

The recent revolt against plans at Unilever is a case in point. Aviva Investors and its chief investment officer David Cumming led the fight, alongside Legal & General Investment Management, M&G Investments, Columbia Threadneedle and hedge funds Schroders and Lindsell Train, to stop the consumer goods giant moving its headquarters to the Netherlands.

Sachak points out activists have a good record of delivering shareholder value in the consumer sector and he expects to see more and more interventions in the future. “Typically, corporate boards are loath to dramatically change the status quo structures. Activists are usually the friend of shareholders, if not always the friend of management.”

Neil Sutton adds: “There is quite a high degree of recognition that you better take these activists seriously. You need to get your strategic act together before the power is taken out of your hands. And there is now more quiet preparation than ever by boards to think about what the activist agenda might be.”

So, with activism here to stay in food and drink, who are the biggest power players hopping over those gates?

If there is one example that highlights the scale of the problem facing global behemoths of food and drink, and the power wielded by activists, it has to be Daniel Loeb’s tussle with Nestlé. The world’s biggest food company crumbled just days after Loeb’s $18bn hedge fund revealed in June 2017 it had spent $3.5bn on buying a 1.3% stake and accused the Kit Kat maker of being “stuck in its old ways”. Nestlé committed to a $21bn share buyback programme and later set itself an operating margin target for the first time.

It sent a sobering message to the rest of the consumer packaged goods industry: no one is too big to shake up.

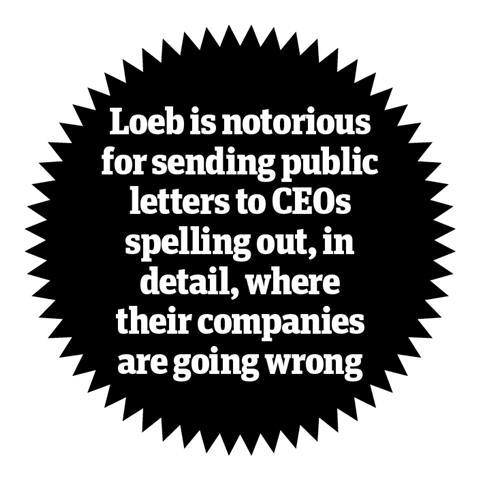

Loeb is notorious for sending public letters to CEOs spelling out, in detail, where their companies are going wrong and what needs to be done. “The dismal stock performance is a report card on the company’s leadership, which has made a series of blunders,” he wrote during his latest campaign against Campbell Soup. “We believe the past year has been particularly disastrous.”

He has a point. Campbell’s sales have been in decline for five years in a row and it has amassed huge debt thanks to its questionable $6.2bn acquisition of Snyder’s-Lance.

Third Point, which holds a 7% stake, took the drastic step of calling for all 12 directors to be replaced (even after CEO Denise Morrison quit), and sued the board for alleged breach of “fiduciary duties” but this week it finally ended its proxy fight after winning two seats on the board and a role in its search for a new CEO.

Even when he has not actively called for change, Loeb has caused headaches with his actions. He piled misery on Morrisons in 2015 building a short position worth £50m against the stock of the then-struggling supermarket. The bet didn’t pay off though as the most shorted stock on the FTSE 100 unexpectedly surged on a David Potts-inspired recovery.

Back at Nestlé, despite giving in to a raft of Loeb’s 2017 demands, Third Point has stepped up its campaign this year as the Swiss group’s share price continues to languish. Loeb has even launched a website, Nestlenow.com, to rally other investors to his cause.

Loeb writes that with its “muddled strategic approach” Nestlé is failing to live up to its own mandate of “long-term sustainable value creation”. He is urging the business to become sharper in articulating its strategy, bolder in reshaping its portfolio and faster in overhauling its organisation.

There are also calls to break up the lumbering Swiss giant into three distinct business units to cover grocery, beverage and nutrition - each with their own CEO - and put the ice cream, frozen foods and European confectionery businesses up for sale.

Worryingly for Nestlé and CEO Mark Schneider, it appears as if other shareholders share Loeb’s concerns about how the group is dealing with shifting consumer behaviour. An independent survey of investors by Exane BNP Paribas in October indicated 80% of those questioned thought Nestlé should be more active on disposals, 70% wanted it to offload the 23% stake held in L’Oréal (despite announcing plans to sell its separate skincare business) and 65% said they would vote against the re-election of chairman, and former CEO, Paul Bulcke if Third Point campaigned against him.

Consumer goods CEOs will be nervously hoping not to become Loeb’s next target.

If the 3G Capital model of slashing costs and chasing margins is viewed as the ultimate in short-term investing, JAB may be the antidote. The German family investment group’s voracious appetite for food and drink deals makes comparisons with 3G inevitable, but JAB plans to hold on to its portfolio for at least a decade, investing in and expanding its companies. City sources say that where 3G starts from a thesis of stripping out costs to invest in further M&A, JAB is more focused on brand building.

Backed by the secretive Reimann family, JAB is run by three co-managers, including former Reckitt Benckiser CEO Bart Becht. The team has splashed out close to $60bn in the past six years building up a coffee empire to rival Nestlé and Starbucks.

An $18.7bn cash purchase of Dr Pepper Snapple in January marked a departure from the focus on buying coffee and coffee-linked retail assets such as Krispy Kreme and Panera Bread. It has combined the fizzy drinks producer with its Keurig Green Mountain coffee business. JAB also added Pret a Manger to the mix in June for £1.5bn.

It remains to be seen whether the group can keep making deals at such a relentless pace. However, Becht has admitted JAB is on the hunt for more outside capital to fuel further growth. “The end game is now to have a major player in beverage and we retain our objective of being a major player in coffee,” he says.

The darling of Wall Street, 3G Capital has transformed the beer, fast food and packaged food industries. Its brutal, yet highly focused, playbook of ‘zero-based budgeting’ has been adopted by a raft of struggling food giants seeking the same surge in profitability. The global investment firm - founded in 2004 by Brazil’s richest man Jorge Paulo Lemann, along with other investment partners - has stripped $1.7bn of costs out of Kraft Heinz since the $62bn merger, axing 10,000 jobs in the process. Margins at the business have soared to 28%, compared with the industry average of 16%.

However, 3G has found food manufacturing a much more frustrating and complicated experience than its forays into beer and restaurants.

As well as the embarrassing climbdown in the misjudged £115bn tilt at Unilever, the merger of Kraft Heinz has proved a real blot on the copybook, with sales tumbling for eight quarters in a row. Investors have reason to question the model, with Kraft Heinz shares trading at more than 30% lower than at the time of the merger, a painful loss in market value of about $50bn. Buffett stepped down from the Kraft Heinz board in February and, in April, 3G sold a chunky 7% stake, dropping its holding to 22%.

To add to the misery, 3G now has its own activist shareholder calling for action to stop the rot. Krupa Global Investments, which owns £100m of Kraft Heinz stock, held protests outside the offices of 3G and Berkshire Hathaway in September calling for further investment and more acquisitions.

It remains to be seen whether a wounded 3G proves to be an even more dangerous animal, but you wouldn’t bet against it.

Elliott Management is a hedge fund with the power to take on nation states - and win. With almost $40bn and an army of 400 employees it has the resources to get its way in any battle with corporate boards. The New York fund, launched by Paul Singer in 1977 with $1.3m, famously fought with Argentina for 15 years over lapsed debt payments, seizing one of the country’s naval ships in the process. It also led the charge against Tesco in seeking £100m in damages, accusing the supermarket of misleading the stock exchange in the wake of the 2014 accounting scandal.

Activist Insight’s latest annual report on activism reveals Elliott broke its own records in 2017, with 21 companies subjected to its public demands across nine countries. And food and drink hasn’t escaped its advances. In April, the fund disclosed it had amassed a 6% stake in Whitbread and demanded the business spin off the Costa coffee chain from Premier Inn. Whitbread caved in less than 10 days later, selling to Coca-Cola.

Elliott is also an expert in twisting the arms of companies to pay more for acquisitions. During the 2016 takeover of Poundland by South African retailer Steinhoff, Elliott increased its stake in the discounter to 17%, enough to potentially derail the entire deal. Although the fund’s intentions were not made public, Steinhoff increased its offer by £13m to £610m.

And it isn’t the first time Singer has profited in food and drink from this kind of hold-out approach during live takeovers. AB InBev - and 3G Capital - ultimately coughed up an extra £8bn before it swallowed SAB Miller for £79bn when Elliott argued for improved terms in the aftermath of Brexit and the sharp fall in the value of sterling.

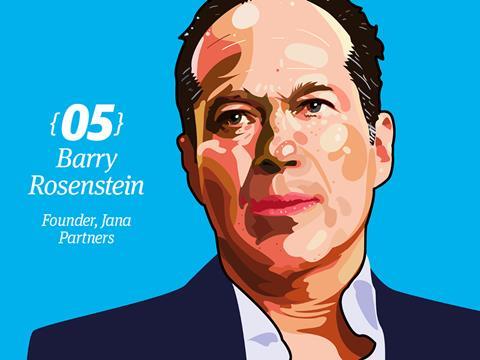

“They’re greedy bastards.” Whole Foods Market founder and CEO John Mackey certainly came out swinging as he tried to fight off Jana Partners in 2017. Mackey accused the activist hedge fund of putting out propaganda and trying to destroy the reputation of the organic food retailer in search of a quick buck. The problem, though, was Jana and its founder Barry Rosenstein had done their homework. The $8.5bn fund pinpointed a host of structural problems at the flagging business as it revealed it had amassed a 9% stake. Shares in Whole Foods rallied as hopeful investors anticipated a sale. And they didn’t have to wait long, with Amazon swooping in for a $13.7bn takeover less than two months later and Jana pocketing a healthy $370m profit as a result.

Jana was the most prolific activist operating in food and beverage in 2017, with four campaigns against Pinnacle Foods, Jack in the Box, Bloomin’ Brands and Whole Foods, according to analysis by Grant Thornton. The fund has previously agitated for change at bloated packaged food producer Conagra and US retailer Safeway too, resulting in wholesale restructuring and sell-offs at both businesses.

The irony won’t be lost on Leahy that, after turning Tesco into the UK’s biggest supermarket, quadrupling revenues and growing market share to 33% in his 14-year tenure, he has since piled into the competition.

Private equity giant CD&R appointed Leahy as a senior advisor in 2011 and chose him to chair B&M European Value Retail as it readied for a flotation. The discount chain had doubled sales to £2.7bn, rapidly expanded its store portfolio, and boosted its grocery offer, not least with the purchase of Heron Foods, by the time he left five years later. Leahy was also a critical component of CD&R’s attempt to win the Unilever spreads auction. And he currently sits on the board of Motor Fuel Group, another CD&R investment, which this year acquired the UK’s largest service station operator MRH to create a business with more than 900 sites. The growth of convenience stores within petrol stations is just another avenue that has siphoned off sales at supermarkets.

Unilever may have robustly fended off Kraft Heinz and 3G Capital, but the unsolicited approach left the consumer goods giant shaken. In short order, it announced a dramatic restructuring plan to placate investors, including a form of 3G’s infamous zero-based cost cutting. It set itself a margin goal of 20% by 2020, formalised plans to offload the spreads business and addressed the complicated dual UK-Dutch stock market listing. But the proposal to abandon its UK headquarters and shift base to Rotterdam sparked a furious investor revolt, with its third-biggest shareholder, Lindsell Train, a UK fund that usually likes to stay below the radar, joining the chorus of opposition. Shifting HQ would have turned Train, and other shareholders in the FTSE 100 benchmark index, into forced sellers of the stock. Unilever beat a hasty retreat, scrapping its plans three weeks ahead of the shareholder vote. Train, who operates a quieter, more long-term strategy than most funds, also holds large positions in Diageo, Heineken, Mondelez and PepsiCo.

Considering the myriad challenges consumer goods firms are struggling with sector-wide, it took plenty of chutzpah for Martin Franklin to set out to build a global food and drink empire in 2014. And if that wasn’t difficult enough, he bet on the stagnating UK frozen food category as the launchpad for his ambitions. Nomad Foods, the investment vehicle floated on the London Stock Exchange by Franklin and Noam Gottesman, reeled in Birds Eye owner Iglo for €2.6bn in its 2015 maiden acquisition, before bolting on Findus for £500m. The turnaround has been slow and painstaking, but has started to yield results this year as the overall category emerged from a big freeze to become the best performing in the UK market. The jury is still out on whether Nomad will ultimately succeed. But Franklin has done it before, building up vast consumer products business Jarden from nothing and selling it for more than $15bn.

Painstaking restructuring at Metro has left the door open for activist investors, with Czech billionaire Daniel Kretinsky taking up the challenge. Metro shares have floundered on the back of a string of poor financial results and lowered future forecasts. The group has spent several years selling off non-core businesses and pushing through a demerger of its wholesale and retail arms from consumer electronics division Ceconomy.

Speculation is mounting that Kretinsky is preparing a full takeover bid of Metro after he built up a substantial shareholding earlier this year, buying stakes from investment group Haniel and taking over most of Ceconomy’s remaining 10% holding.

Kretinsky has a wide range of business interests, including ownership of the biggest energy group in Central Europe EPH, Czech media house Czech Media Center and football club Sparta Prague.

The 76-year veteran investor isn’t showing signs of slowing down in his golden years, picking a fight with a global giant with market cap of $232bn in 2017. His bruising encounter with P&G - the biggest, and most costly, proxy battle in corporate history - ended with him taking a seat on the board. Trian Partners, a $13bn fund co-founded by Peltz in 2005, spent $25m on the campaign on top of a $3.5bn investment in the company.

Peltz is perhaps best known for his pivotal role in the break-up of Cadbury Schweppes in 2007, with fellow activist Bill Ackman. He was later instrumental in the creation of Mondelez, which spun off from Kraft. A campaign to push PepsiCo to do the same and split its beverage and snacks businesses was ultimately abandoned as CEO Indra Nooyi stuck to a long-term plan to shift the portfolio to healthier products. However, PepsiCo still slashed 8,700 jobs as part of a $1.5bn cost-cutting exercise to appease the activist.

No comments yet