The climate crisis is the world’s biggest threat. So what is the future of the food supply if the worst-case scenarios come to pass? And what is being done to ensure that they don’t?

Visiting a supermarket back in February could sometimes feel like a horrible lockdown throwback. Empty shelves, supermarket rationing… the only difference this time was it was tomatoes, peppers, and cucumbers in short supply, not toilet paper.

The causes of this year’s shortages were also different, with an intense and prolonged drought ravaging crops across Spain, just one of a growing list of foods affected by our collapsing climatic stability in recent years. Tesco said February’s shortages were “temporary” at the time, but just last week, more shortages emerged due to unseasonably cold weather in Spain.

Extreme weather events are nothing new. But their impact on food supplies is expected to become ever more obvious unless serious mitigation measures are put in place.

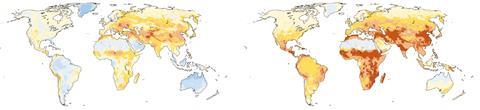

Two years ago, NASA published a study suggesting that global corn production could fall by up to 24% by the end of the century unless such policies were quickly enacted. If not, the shortfalls could start becoming apparent by as early as 2030.

High productivity – ‘breadbasket’ – regions like India, Brazil and Argentina would be especially susceptible, the report said, with key crops like wheat, soy, bananas, rice and coffee all affected.

“Even under optimistic climate change scenarios… global agriculture is facing a new climate reality,” said lead author Jonas Jägermeyr. “And with the interconnectedness of the global food system, impacts in even one region’s breadbasket will be felt worldwide.”

It’s a prediction familiar throughout the academic literature. A study published by peer-reviewed journal One Earth, in 2021, concluded that one third of global crop and livestock production could move outside safe climatic areas by the end of the century unless global temperature warming was kept to 1.5°C-2°C as per the Paris Agreement goals. It argued the most vulnerable areas included south east Asia and Africa’s Sudano-Sahelian zone, a belt region in central Africa that is already known for extremely dry conditions.

More optimistically, it also gave forecasts for a low emissions scenario, predicting 8% of crops and 5% of livestock would be at risk if the Paris Agreement is met.

But the issues aren’t only abroad. Climate change poses the “biggest medium to long-term risk” to British production too, according to the government’s 2021 Food Security Report, which highlighted the 40% drop in wheat yields after bad weather in 2020 as “an indicator of the effect that increasingly unreliable weather patterns may have on future production”.

All in all, it means food shortages as a result of extreme weather events are not only likely but “inevitable”, says William Hughes, Mazars sustainability services lead.

What of Spain?

It is therefore perhaps little wonder that food businesses are increasingly concerned, with 10 times more organisations now citing weather and climate as a risk to their ability to operate, compared with 2018, according to regulatory experts Ideagen.

The problem facing them is that while it’s one thing to put a risk assessment strategy in place, extreme weather events are hard to predict. This makes solutions tricky and means deep supplier engagement is necessary to go beyond the usual transactional nature of buying and supplying, Hughes says.

“The issues with fruit & veg earlier this year really highlighted the importance of knowing your suppliers a little bit better,” says Hughes. “Not just for supply reliability, but also from a climate change point of view.”

This might include having robust and dynamic relationships with suppliers, involving them in risk assessment conversations, helping them financially recover from the impacts, and often funding the likes of water management and soil improvement projects that help them prepare for future challenges.

Diversifying is important too. “Retailers should be building strong relationships outside of their core suppliers,” says Andrew Opie, director of food and sustainability at the British Retail Consortium.

So what of Spain, the current causal hotspot of European food shortages and producer of 10% of Britain’s total food imports? Already this year, the country is in a record-breaking spring heatwave. What if recent droughts continue to persist?

“I don’t think it will get to the stage where the retailers move production entirely out of Spain because it is an incredibly important part of the supply chain,” says Opie. Nonetheless, since it has become “more of a risk”, he does suggest supermarkets think of alternatives.

But even this has obvious limitations. “There’s only so many times you can keep shifting until there’s nowhere else to shift to,” says Martin Baxter, deputy CEO at the Institute of Environmental Management and Assessment. “The question is do businesses have the foresight to recognise that and therefore make the investments to build resilience?”

To achieve long-term durability, companies need to know exactly the type of risks they are dealing with, which is where mandatory policy like the UN’s Task Force on Climate-related Financial Disclosures (TCFD) comes into play.

Now a legal bind, the TCFD framework requires large businesses in the UK, such as Tesco, Unilever and Danone, to include climate risks in their annual reporting. It forces companies to place a financial value on the risk of climate breakdown, encouraging the risks to be valued as much by commercial teams as those focused on sustainability.

“Even under optimistic scenarios, global agriculture is facing a new climate reality”

Jonas Jägermeyr

The IPCC has made it clear global warming, under any scenario, comes with a financial toll, from the energy needed to heat or cool industrial livestock facilities to changes in feed quality and quantity, as well as managing limited water resources more efficiently.

So TCFDs crucially provide a glimpse into how much addressing that impact is going to cost companies. For instance, Tesco’s latest TCFD report showed that the potential impacts of a 2°C scenario on its animal protein and property categories could respectively amount to £150m-200m and £50m-100m annually by 2030.

Even Nestlé’s low emissions scenario predicts a cashflow impact of up to £16bn by 2030. For most companies, the more costly measures include potential carbon taxes, adoption of lower-carbon tech, and consumer demand shifting to more sustainable choices.

But while the common thread in all these assessments is the significant financial cost of addressing climate action, by and large there is recognition that the risks of not acting pose more serious financial threats in the long term.

Investors are therefore wary too. FAIRR, an investor network representing over £56 trillion in combined assets, reported in March that ‘business as usual’ from now on would lead to 40 livestock companies suffering a 7% reduction in profit margins compared with 2020. This represents £19bn in total, equivalent to over seven times Tesco’s annual profits.

Considering the meat and dairy sectors are set to be some of the most affected by climate change, as per FAO estimates, it’s to their benefit to have robust mitigation strategies in place.

Even so, there are concerns that many businesses are failing to take necessary action. JBS, for instance, the largest meat processing company in the world, was referred to the US financial regulator by campaigners over claims it had failed to disclose the full impact of its carbon emissions when selling green bonds to investors earlier this year.

Tesco too was recently slammed for allegedly buying chicken and pork fed on soy allegedly from illegally deforested areas in the Amazon. And Nestlé was accused of falling short of its own net zero ambitions just last week by failing to set methane emissions reduction targets.

A lack of corporate buy-in is already having direct consequences on the climate, with the likelihood of keeping below the 1.5°C limit down by 10% since the IPCC’s first global warming special report in 2018. This is the “direct result of governments and corporates in high-emitting economies failing to implement the needed transformation in a coherent manner,” according to Amir Sokolowski, global director for climate change at the Carbon Disclosure Project (CDP).

Inside Nestlé, there is an awareness “we can do more and we need to accelerate”, says Emma Keller, the company’s head of sustainability.

“There’s only so many times you can shift before there’s nowhere else to shift to”

Martin Baxter, Deputy CEO at the Institute of Environmental Management and Assessment

But rather than simply dropping suppliers who may not be taking suitable steps, Keller argues it is more important to stick to a long-term plan rather than going reactionary. “You might get a different picture from retailers vs suppliers, but for us shifting is not really an option. We have a vested interest in ensuring those supply chains are robust so we can continue to get those ingredients.”

This includes working with farmers around the globe to reduce carbon emissions and invest in regenerative agriculture practices. Nestlé is actively working on this, investing one billion Swiss francs in its coffee supply chains to help farmers transition to a regenerative agriculture model and paying dairy farmers in big sourcing countries like Brazil and the UK an additional bonus to encourage them to implement sustainable practices.

They’re not the only ones on the forefront of climate action at a supply chain level. Britvic was also recently recognised by the CDP for its supplier engagement efforts, ranking in the top 7% of international companies working with suppliers to combat climate change.

Danone too was one of the few companies that achieved a place on the CDP’s ‘A List’ for its robust efforts across the three environmental areas of climate change, forest preservation and water security.

Keller believes only with greater multi-sector collaboration can food security and climate action go hand in hand. And “we need to ensure farmers are funded to be able to do the things we’re asking them to do”, she adds.

Mangoes and pineapples

When talking about food shortages in the long-term, the concept of seasonality often comes up. Should we be buying mangoes and pineapples year-round, knowing the carbon impact that comes with growing and transporting these products around the world? Or should we look to back British growers, even if it comes at the expense of a less diverse offering and higher prices?

The issue is domestic production isn’t immune to the climate challenges either. A recent Climate Change Committee study showed the UK was “strikingly unprepared” for climate change, leaving sectors like agriculture vulnerable due to the absence of clear strategy from government and business.

Last year’s heatwave was a clear example of that, with fruit & veg growers left counting their losses after their crops were badly affected.

But it’s notoriously hard to change people’s attitudes towards seasonality when they’ve grown accustomed to being able to buy everything, no matter the time of the year.

Ultimately though, they might not have to. “We don’t know what’s going to happen with UK seasonality”, says Opie, noting strawberry production is now possible in October due to warmer climate as well as tech innovations. Plus, the UK still largely has the privilege of being a wealthy nation with easy access to food chains from all over the world, so long as it’s ready to pay more when availability shrinks.

“The UK is strikingly unprepared for climate change”

Climate Change Committee

But this “mercenary approach” in which farmers in vulnerable areas are “used then discarded” is not going to cut it, Hughes says. This is why intergovernmental collaboration at forums like COP and international treaties like the Paris Agreement are so important – to make sure “just transition” is not just a buzzword but actual law.

Progress was made at last year’s COP27, when after 30 years of deadlock, the world’s richest countries finally agreed to pay poor nations – largely from Asia, Africa, Latin America, the Caribbean and South Pacific – for the damage caused by devastating storms, heatwaves and droughts fuelled by global warming.

There are still questions around how the fund will work, who pays up, and where the money goes. These details will take a while to iron out, adding to the prevailing worry, which is whether both businesses and governments are acting fast enough to avoid food shortages.

Now the effects are measurable and the pressure is on from every side, businesses are aware of the risks of inaction. “Can we do more? Yes,” Keller says. “Any minute we delay is a wasted opportunity. But I genuinely think we are on the cusp of really seeing a change in both attitudes and narrative and a real willingness to step up and do this.” Let’s hope she’s right.

No comments yet