Once they were a publicity-shy enigma. Now, they are anything but. Aldi and Lidl’s newfound love of PR has seen curious customers pour through their doors to snap up the bargains they have read about or seen on TV. That, plus a combination of the lingering recession and their rapid expansion, has generated sales and profits that have left their rivals staggering around punchdrunk in their wake.

It’s a rosy status quo. Kantar Worldpanel says Lidl sales are up 20% year on year, delivering a record market share of 3.6%. Aldi is doing even better, with year-on-year uplifts of 32% and market share of 4.8%, firing it right up behind Waitrose, which has 4.9%.

Meanwhile, Nielsen data shows the discounters are visited by 14% more people than a year ago. And there’s more to come. Over the next five years, the UK discount market will double in value , from £10.8bn now to £21.4bn by 2019, increasing its market share to 10.5% in the UK, the IGD predicts.

The discounters have been “very effective at stealing share for packaged goods,” but if they can “eat into” the mults’ fresh foods sales “we could see a seismic shift in the sector over the next six months,” warns Mike Watkins, Nielsen head of retailer and business insight.

Yet potential hazards lurk on the horizon. The discounters might have big plans for store numbers, but so do rivals. And having been blindsided over the last three years, those same rivals are now fighting back. Asda is locking prices down; Morrisons is slashing them. Sainsbury’s has teamed up with Netto, and new Tesco CEO Dave Lewis won’t make the same mistake his predecessor did and underestimate them. So with all those challenges - and more - ahead, how big can the discounters get?

In terms of ramping up store numbers, Lidl is the more ambitious. In November 2013, in his first interview, MD Ronny Gottschlich told The Grocer he dreamed of 1,500 stores in the UK. Six months on, nothing has changed. “It is full steam ahead,” he says. “I can see us adding 20 to 40 stores a year. We might do 50. We want more stores and that long-term vision remains the same.”

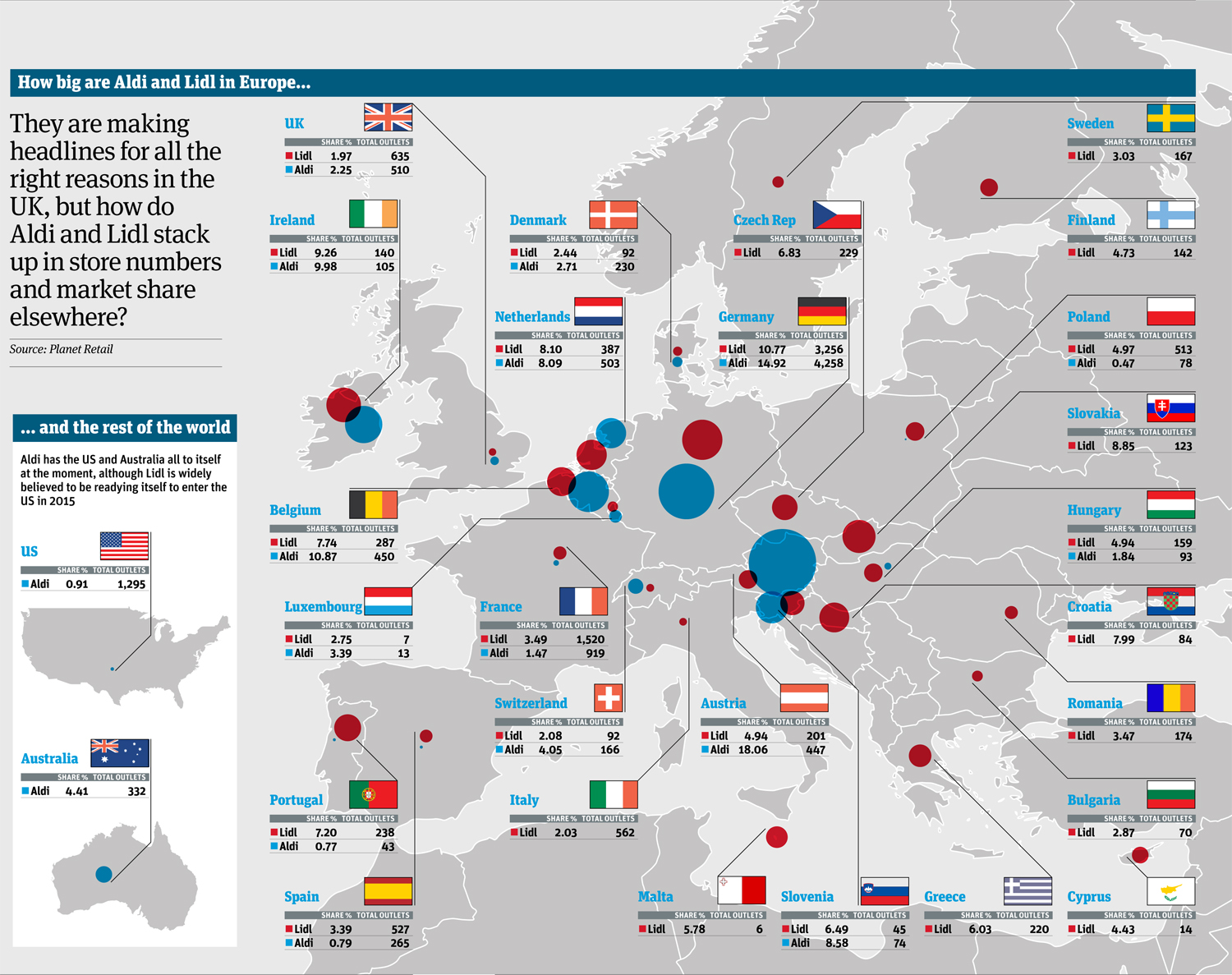

Aldi has 510 UK stores to Lidl’s 635, according to Planet Retail, but it’s growing faster, arguably because it caught on to the power of publicity earlier. It did its first interview with The Grocer in October 2012, and its TV ads were being chuckled at a full two years before Lidl hired TBWA in 2013 to produce something similar.

Aldi has also been more aggressive property-wise, adding 25 stores in 2012 and 39 in 2013, according to property analysts Glenigan, while Lidl focused on consolidation and refurbishment, adding 27 stores over the same period - less than half as many.

“They have sizeable acquisition teams; they have feelers out everywhere”

And Aldi is by no means finished. It plans to splash out £600m this year on 60 stores. “We are convinced we can keep it going,” says joint MD Matthew Barnes. “Sixty five new stores a year isn’t out of the question. It’s not the easiest country to get sites in, but we think 1,000 stores is an absolute possibility.”

Possible yes, but all the grocers want new stores and there are only so many that can be built. And whereas once the discounters could build 10,000 sq ft stores while the supermarkets focused on stores 10 times that size, that particular space race is over. Space Race II is all about stores up to 10,000 sq ft, meaning they have serious competition. Although Aldi and Lidl have shown flexibility recently, opening a 7,000 sq ft store in Kilburn and a 5,000 sq ft store in Camden, the classic 10,000 sq ft model remains the priority.

“They have specific requirements because there are operational considerations to take into account,” says head of retail at Christie & Co, Steve Rodell. “I was with Sainsbury’s yesterday, talking about Netto, and a unit has to be 18m wide. They can’t be flexible because it impinges on the floor plans and the store layout. I imagine Aldi and Lidl are the same. I have put units to them in the past you would think could convert to a discount store, but they have said no. So to expand they may need to be more flexible in their criteria.”

That said, Rodell offers up two reasons as to why he’s confident the discounters will get what they are after. “They have sizeable acquisition teams, they have feelers out everywhere, and when they start advertising they get inundated with enquiries. And if you are a switched-on developer you might welcome a discounter with open arms. It will bring footfall, the rent will be secure. I don’t think they need to worry too much about competition.”

Perhaps not, but other challenges remain. “Expansion needs to be where expansion is needed most, and often that is in the cities, where securing sites is tough for multiple reasons,” says former Lidl senior buying manager Stefan Porter, now a freelance fmcg consultant and MD of Market Porter. “The biggest sales growth is in well-to-do areas like Leatherhead and Dorking. They are not cheap, and there is often PR to negotiate they have to spend six months dealing with.”

“I think Lidl are game for online. Dieter Schwarz owns Schwarz E-Commerce, which built the Lidl app”

Not to mention the usual planning quagmire. Furthermore, after picking up The Grocer Gold for Grocer of the Year in June - Aldi’s second in a row - joint MD Roman Heini referred to Aldi as a “victim of its own success” and spoke of the ongoing need to upgrade and extend existing stores and car parks to cope with the influx of customers.

It’s a problem any of the major multiples would love to have, but Porter says however welcome that pressure is, it “inevitably replicates its way back through the supply chain to the warehouses, where more deliveries arrive, so more stock is held, which means more space constraints. That is where the bottleneck is felt. These are pressures always felt at times of unprecedented growth and they can only be abated by capex in the form of new warehousing.”

Which is exactly why Aldi and Lidl are both building more: Aldi will open its eighth - a 441,000 sq ft depot in Goldthorpe - in 2015. When Lidl opens its new DC in Northfleet later this year, it will have nine.

Post recession blues?

Perhaps the biggest issue isn’t whether they can handle the growth, or build hundreds of new stores, but whether by the time they have doubled in size the recession, which originally drove so many customers in, will have finally faded away. Should that happen, will relatively flush shoppers still want to shop there?

There is a precedent. In 2008, with the credit crunch in full swing, Aldi recorded pre-tax profits of £92.7m and sales rose 32%. The media dubbed its performance the “Aldi effect.” Then the initial impact of the credit crunch wore off and sales plunged. Aldi delivered a £54.2m pre-tax loss for the year to 31 December 2009 and sales rose just 1.7% to £2.1bn, despite 45 new stores.

However, Kantar Worldpanel director Ed Garner doesn’t think the discounters need to worry this time around. “The mood has changed. The offer we see today is different to 2009 and the perception is much less pejorative than it used to be.”

So if the major multiples can’t rely on a booming economy to help them out, or the fact the discounters are an attractive proposition for a landlord, what can they do to derail their progress?

Sainsbury’s has taken a novel approach by joining forces with Netto, which left the UK after Asda snapped up its 193 stores for £778m in 2010. The new jv plans to launch 15 stores within 100km of Wakefield inside a year to test the water. A more conventional strategy could be to go head to head on price, but it’s “probably only Asda that can do that,” says Garner. Or do the opposite, and “shift as far as way as possible away from them, like Waitrose. That leaves Tesco and Morrisons in the middle, which is why they are suffering”.

It’s also important to note that it’s not just Aldi and Lidl making an impact. Fixed price discounters like Poundland and variety discounters like B&M Bargains and Home Bargains are experimenting with chilled food - Poundland sells ham, cheese, bacon, minced beef, yoghurts and milk, for example - and all are making determined moves into ambient grocery. Meanwhile Farmfoods is coming up fast in frozen, recording sales uplifts of 23.2%.

“The big four will struggle to live off similar margins to a discounter”

Yet when the reasons for Philip Clarke’s departure were picked apart, the impact made by the German discounters, and his apparent reticence to take them seriously enough, quickly enough, emerged as a major factor. Clarke’s replacement, Dave Lewis, will no doubt want his customers back. “The big four are taking the discounters more seriously than they ever did,” says Porter. “If they decided to take a huge chunk out of their margins, that could damage the discounters. But they will struggle to live off similar margins because the cost of running a broad assortment is so high.”

In any case, the discounters have vowed publicly they will never be beaten on price. “It’s interesting that some of the competition is trying to fight us on our home turf,” says Aldi’s Heini. “I wouldn’t say we welcome it, but we are more than happy to fight that battle.”

Their ambitions and achievements are not limited to the UK, of course. Planet Retail analyst David Gray predicted in June that Lidl would overtake Carrefour, Tesco and Aldi to become Western Europe’s biggest grocery retailer by 2018, generating sales of £65bn, while Aldi would overtake Metro to move up right behind Tesco. So how could what Gray describes as an “unprecedented power shift in European retail” affect their potential for growth in the UK?

“Germany is saturated, so they are seeing slow growth, and France is quite fast but a lot slower than the UK,” says Gray. “At Lidl, the UK remains way behind those two.” That gap offers room for UK growth, says Gray. However, he cautions there aren’t many lessons we can take from the discounters’ success in their native Germany, where they dominate the market.

“The UK and German grocery markets are simply poles apart, making it unlikely the discount model first developed in Germany can be directly uplifted to the UK,” he says, adding it’s also “unlikely” the UK will hit similar market share. “At least not in the next five to 10 years. Yes, market share will go up, but even in five years they’ll still remain relatively niche.”

Yet he also says global growth could fund trips down other UK avenues, like convenience, which is to date relatively untapped by the discounters.

And there is online. Both Aldi and Lidl have insisted they have no plans, although Lidl’s rhetoric has been softer than Aldi’s. And of the two, Lidl launched a non-food and wine offer online in Germany in March, allowing shoppers to order online and collect from stores.

“I think Lidl are game for online,” says Porter. “Dieter Schwarz (Lidl chairman and CEO) owns Schwarz E-Commerce, which built the Lidl app and powers its e-commerce offering, so you’d expect that space to be entered soon.”

Will it? As ever, when the discounters choose to, the wall of secrecy is virtually impenetrable. Yet even from the outside looking in, one thing is clear. Growth will inevitably level out, but with sales continuing to increase - and additional channels as yet unexplored - the Teutonic twosome aren’t in any danger of slowing down anytime soon. Just the opposite, in fact.

The A-Z of Aldi & Lidl

A is for Advertising: hugely popular and successful above-the-line campaigns from both Aldi and Lidl introduced their evolution to UK living rooms.

B is for Buying power: the discounters have enormous buying power throughout Europe, which delivers rock bottom prices on staples like rice and pasta.

C is for Credit crunch: the recession sent straitened Brits pouring through the doors of the discounters, who reacted quickly to keep them there.

D is for Dynamic duo: Aldi’s unique set-up of joint GMDs Roman Heini and Matthew Barnes has worked a dream as they dovetail perfectly.

E is for Expansion: expansion has been rampant over the last couple of years, particularly at Aldi, and has been a key factor in its massive sales uplifts.

F is for Fresh: both have ramped up their fresh offering and Brits love it. 50% of Aldi sales are now fresh and 40% at Lidl - a huge turnaround.

G is for Gottschlich: Lidl’s Anglophile East German MD is relaxed, friendly and driving the discounter forward with intelligence and focus.

H is for Horsegate: Aldi and Lidl didn’t break stride, despite being implicated. Aldi even emerged rather well, after a blistering attack on a wayward supplier.

I is for Imitation: Aldi got burned by Saucy Fish after launching a similar line but copying or benchmarking against top brands is key to its successful ad strategy.

J is for Jokers: Lidl and Aldi both make humour central to their ad campaigns and Aldi has won numerous awards - and customers - because of them.

K is for Kilburn: Aldi recently relaxed its rigid stance on minimum store size in central London, opening a 7,000 sq ft store. Lidl is doing the same.

L is for Locations: their concentration of high-street stores fits with the current trend for shopping little and often rather than heading out of town.

M is for Marketing: straightforward offers and voucher tie-ups with tabloids have been received well by shoppers on a budget.

N is for Non-food: it looks like a random assortment of nonsense, but Lidl say that’s precisely why its shoppers love it.

O is for Own label: the predominance of own label, particularly at Aldi which only carries a handful of brands, means prices are consistently low.

P is for Price war: Morrisons kicked it off, Tesco joined in, but Aldi and Lidl just keep growing the gap - and have stated publicly they will never be beaten.

Q is for Quality: record-breaking numbers of Grocer own label awards for both Aldi and Lidl tell the story of how progress has been made on quality.

R is for Ranging: supermarkets jump on the limited range as a criticism - but discounter shoppers don’t care. It makes for a quick, uncomplicated shop.

S is for Simplicity: everything is kept as simple as possibly: from the lack of confusing promotions, to the stripped-down range, to the layout of the shop.

T is for Tiering: introducing good, better, best tiering to allow shoppers to trade up or down has been hugely successful - particularly the top tiers.

U is for Underdog: Brits love an underdog - community spirit thrives among loyal shoppers who spread the word about getting one over on the mults.

V is for Value: Price means nothing if the product is rubbish - value for money is what savvy shoppers are after in 2014 - and both deliver excellent examples.

W is for Wagyu: premium beef, award-winning Champagne, lobsters: affordable luxury has become a key strategy.

X is for X-for-y: there are no confusing x-for-y style promotions, apart from the very occasional bogof in Lidl. It’s a straightforward price reduction or nothing.

Y is for Year on year: sales are up 32% up at Aldi, 20% at Lidl - numbers that the supermarkets can’t even dream of getting close to.

Z is for Zeitgeist: it’s a German word - and the discounters are unquestionably tapping it when it comes to the state of grocery in the UK today.

1 Readers' comment