Those who remember physics lessons will know nature abhors a vacuum. The same is true of business - and a political vacuum is exactly what we have after a rudderless UK ejected itself from Europe, sending the markets into a tailspin not seen since the global recession.

For the globe’s biggest fmcg players, the economic and political chaos unleased by Brexit could hardly have come at a worse time as the industry has stumbled to its weakest post-recession level of growth.

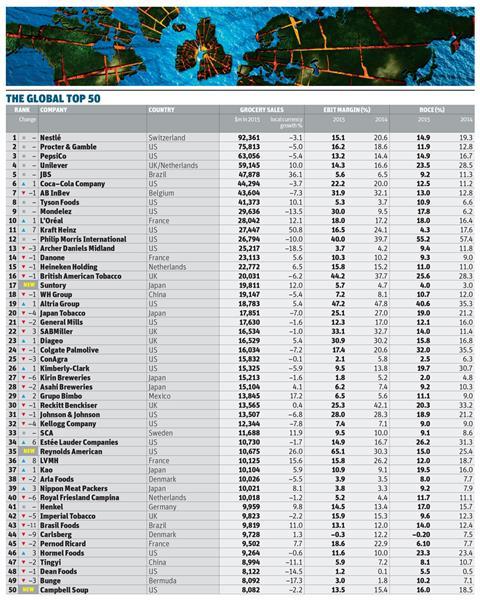

The OC&C Strategy Consultants/Grocer Global 50 rankings reveal headline growth fell to just 2.3% last year from 3.5% in 2014, and Brexit only adds another hefty obstacle on the road to recovery.

It may be an exaggeration to say a country of 60 million has derailed a sector with a potential customer base of more than six billion, but the aftershocks of the Brexit earthquake look likely to be felt far and wide.

Most immediately the plunge in the value of the pound - which at the time of writing has slumped almost 12% against the dollar since the referendum vote - builds existing currency headwinds into a gale.

“What Brexit has done in the near term is create heightened uncertainty and more wild currency movements, which makes it harder to plan how you do business, set pricing and know what your costs are going to be in the next month or year,” explains OC&C’s head of consumer goods Will Hayllar.

The quantifiable effects of the slump in the pound are not wholly negative for these global giants - those sourcing materials in dollars and selling in sterling (or euros) will suffer, but big exporters like Diageo and British American Tobacco are boosted by translational impacts. The bigger issue is the global uncertainly triggered by currency volatility coupled with political instability - particularly the potential for more EU states to follow the UK to the exit door and the general growth of anti-establishment politics.

“The big concern is what Brexit means for European and global GDP,” says Liberum consumer goods analyst Robert Waldschmidt. “The danger is the volatility and uncertainty mean consumer spending takes a knock and companies become more cautious and don’t invest, which has a feedback loop in terms of global growth.”

While question marks will remain for years about the nature of the UK’s trade relationship with the EU, the US is also facing its own anti-establishment political insurgency in the form of Donald Trump and the threat he poses to the era of free-trade through protectionism and trade barriers. “There is some genuine worry around free trade,” says Hayllar. “If the world becomes less well connected and more isolationist that is undeniably bad for business.”

Tectonic instability

With the tectonic plates already destabilised by economic downturns in many of the so-called BRIC nations, to say nothing of the threat from global terrorism, it’s clear growth is an increasingly rare commodity.

Indeed, strip out the distorting effect of last year’s Kraft/Heinz merger, overall growth across the Global 50 fell to just 0.9% in the 2014/15 financial year, having been as high as 7.3% in 2010/11 and 5.6% in 2011/12.

That slump has been particularly felt among pureplay food and drink players. Local currency sales growth was just 0.4% among food and drink firms, but 10.8% in companies with greater non-food sales, like Unilever and Kimberly-Clark.

That’s partly because commodity deflation was less significant in non-food and partly because competition from local brands is less fierce, says Moody’s senior analyst Ernesto Bisagno. “The trend for uptrading to Western brands varies across different products, [but in general] competition is more fierce for packaged food businesses where it is more difficult to differentiate than, for example, tobacco firms.”

Another key inhibitor of growth has been currencies. Pre-Brexit the major Western currencies strengthened significantly against a basket of other global currencies (see box). Since global fmcg players are more likely to be denominated in the currencies of these stronger markets, it’s created huge headwinds in reported figures, with grocery sales down 5.6% for US firms - only four US fmcg giants increased sales - compared with 2.1% growth in non-US based companies.

‘Currency volatility is the new reality’

The issue of currencies looms large across the OC&C/Grocer Global 50 2016 table. Although clearly there are differences in underlying performance, most of the major moves are driven by currencies and the strength of the US dollar.

LVMH’s rise of eight places up the table was partly driven by a 10% revenue boost from the effect of favourable exchange rates, while Carlsberg’s nine place fall and Brazil Foods’ 11 place tumble can be blamed on their revenues appearing much worse when their sales are compared in US dollars (15% lower for Carlsberg and 20% lower for Brazil Foods).

US companies saw revenues fall 5.6% during the year, while non-US companies saw a 2.1% rise in sales - something OC&C’s Hayllar says is almost entirely driven by the strength of the dollar.

While companies typically hedge currency effects to an extent and investors pay more attention to underlying performance, currencies can have a material effect on performance.

“There’s been high volatility in FX markets in the last few years,” Moody’s Bisagno says.

“The effects are mainly translational, which is more of an accounting issue than a material impact on companies’ credit metrics. But for those companies who have commodity costs or other costs in dollars and revenues in devalued currencies, the impact on margins is real.”

Philip Morris said in its annual report for 2015 that currencies had impacted profitability and hit revenues by 10%, while Kellogg’s reported a 7.2% currency impact and Kraft Heinz a 5.8% hit.

The above figures have been adjusted post-Brexit, which has resulted in a further weakening of the pound and euro against the dollar as investors see the US currency as a safe haven. As such, the situation does not look like resolving itself soon.

“Currency volatility is the new reality for now and is part of the issue in terms of lower growth for longer,” says Liberum’s Waldschmidt. “The global economic mess hasn’t resolved itself and until it does currencies won’t be anything but volatile across the basket.”

| Change in annual exchange rates against the US dollar (Jan 2014-date) | ||

|---|---|---|

| Euro | -19.60% | |

| Sterling | -22.20% | |

| Brazilian real | -41.70% | |

| Chinese yuan | -9.60% | |

| Russian ruble | -49.20% | |

| Japanese yen | 4.30% | |

| South African rand | -29.60% | |

| Ukraine hryvnia | -66.90% | |

However, of most concern is the steady decline in organic revenue growth among those companies that have reported it for the past three years - dropping from 4% in 2013 to 3.8% in 2014 and 3.4% in 2015.

On the surface this appears currency related as Unilever and LVMH, two euro-denominated stocks, reported stronger organic sales growth. But it’s also down to individual performance and the strength of particular brands in a fast-changing world.

“Until a few years ago if you had the number one or number two brands in a big category you could always expect to at least match GDP growth,” says Akeel Sachak, global head of consumer for Rothschild. “You can’t make that assumption anymore as there is a real issue for established brands to remain relevant to the millennial consumer. You’re seeing that development everywhere.”

This steady fall in organic growth is primarily driven by weakening volume growth across the Global 50. Those 18 players that split out volume growth reported a measly 0.3% average increase, with key players such as Kraft Heinz (-2.6%), Carlsberg (-3%) and Mondelez (-3%) reporting significant volume drops.

And this decline comes despite the growing global consumer base. Indeed it’s worse than that, says Hayllar. “The total volume of consumer products that are being consumed in the world is growing faster than the 1.2% population growth as people shift from subsistence into active consumers, so these global players are losing further share.”

Finding a way to drive volumes becomes especially important given the underlying drags on growth from currencies. And there are other factors to contend with.

Deflation

One of these is declining commodity prices over the past four years - particularly the sharp 19% drop in food commodity prices in 2015. Driven by falling oil prices this hasn’t necessarily led to deflation in all markets (as it has in the UK) but it universally helped dampen price inflation and that inhibited top-line revenue growth.

Brent crude oil collapse depresses prices

Oil is a big input into agriculture prices and the drop in the price of oil to an 11-year low of around $36 a barrel had a huge effect on the price of raw materials.

OC&C data shows sugar prices dropped 21% during the year, cereals and meats 15% each, food commodities 19% and dairy plunged 28%.

The fall in dairy prices was especially significant and had a notable impact in driving steep price declines among global dairy firms and hitting revenues. Dean Foods reported a 14.5% drop in organic growth and price falls of 11.5%, while Arla Foods saw organic sales fall 8.3% with prices down 11.4%. Conversely Danone saw 4.4% organic growth with prices up 3.5% because it focuses more on premium processed dairy products and was more protected from price declines.

In general terms, the fall in commodity prices was one of the drivers behind the expansion in gross margins in the Global 50 as input costs fell sharply.

OC&C’s Hayllar notes that, although falling commodity prices do not help volumes, they “help operation gearing in these businesses and give them more breathing space with their top line”.

Since the end of 2015 the price of Brent crude has returned to over $50 a barrel, creating a more benign environment for agricultural commodities like sugar and oils, though dairy continues to fall partly due to EU and US regulation helping drive the oversupply of dairy products.

Dairy producers remain under the most pressure as the long-term decline in retail prices is expected to continue, compounded by the removal of EU production quota regulations in April 2015.

| Food commodity price inflation | |

|---|---|

| 2011 | 22% |

| 2012 | -7% |

| 2013 | -2% |

| 2014 | -4% |

| 2015 | -19% |

At the same time, global fmcg players relying on booming emerging markets sales to bolster performance in recent years have been hammered by the sustained slowdown. The trend for shifting from local brands to premium brands in emerging markets has been a key driver of growth across fmcg, particularly in the alcohol sector. But economic downturns in China and South East Asia and recessionary pressures in Brazil and Russia have slowed this trend.

The problems are perhaps best illustrated in China, where fmcg growth of 3.5% is now significantly behind the country’s 6.9% GDP growth, having been at 11.8% compared with 7.8% GDP growth in 2012. Growth has been steadily declining since 2012 with volumes largely flat and alcohol in particular bearing the brunt as anti-corruption crackdowns and increasing health consciousness have sent alcohol sales down by 6.1%, having been up by 15% in 2012.

Furthermore, it seems local Chinese fmcg producers are coping better with the declining growth than international players. Domestic brands have grown twice as quickly as global brands, with 70% of them in growth compared with 50% of global brands in the country.

One reason is because lower tiered cities are performing better than the high-tier cities typically targeted by global fmcg players. The Global 50 are more targeted at the premium end of the market, which has seen more pronounced slowdowns than regional cities that are boosted by migrants from rural areas.

The battle for consumers in many markets is often characterised as David v Goliath, with the smaller, more nimble local Davids outmanoeuvring their larger, less adaptable global rivals. Certainly these themes remain relevant - from the growth of craft brewers and healthier food and drink alternatives in developed markets as digital marketing opportunities decrease scale barriers, to larger players struggling to adapt to pockets of growth in local emerging markets.

However, Hayllar notes that domestic firms can often be larger within their own markets than multinationals and so can benefit from more scale and route-to-market advantages.

So, with the Global 50 struggling to maintain global share what is their response?

3G Capital’s influence

One increasingly influential approach is that taken by 3G Capital, owner of AB InBev and now Kraft Heinz.

3G has relentless focused on cost efficiencies - stripping out $400m of cost from its 2013 acquisition of Heinz by the end of 2014 and cutting jobs and manufacturing sites to drive a six percentage point increase in EBITDA despite a 5% year-on-year revenue slump.

This “zero-based budgeting” programme has continued with the acquisition of Kraft: 4,600 job cuts have already been made in the combined group amid seven plant closures. In the meantime, AB InBev boasts the best margins in the industry, after cutting more than $2.25bn in costs from 2008 to 2013.

HSBC global beverage sector head Carlos Laboy points to Coca-Cola as a company that has had to change its behaviour to deal with the influence of ABI, by disposing of company-owned bottling operations and reducing headcount from 123,000 to possibly as low as 20,000 by 2018, to increase its operating margins. Laboy argues AB InBev’s next acquisition target could be Coke, forcing it to adapt to outrun the potentially acquisitive beer giant.

“Coca-Cola was weighed down by a great deal of inefficiency, an enormous asset base that was not productive and a legacy of being slow,” he says. “This is about getting faster, leaner and more efficient to be competitive in the new AB InBev/3G world.”

New entries

Suntory

Country: Japan

Grocery sales: $19.8bn (+12%)

Roaring into the Global 50 on the back of a heady binge of M&A activity, the Japanese drinks group powered on with its global expansion. The group has suffered from stunted growth in its domestic market - which accounts for two-thirds of its sales - as volumes in alcoholic beverages declined. Its most notable acquisition was the $16bn swoop for Jim Beam distiller Beam Inc to form Beam Suntory in 2014. It gave Suntory exposure to the world’s largest spirits market and made it the world’s third-largest distiller. Between 2009 and 2015, Suntory also picked up Australian soft drinks business Frucor Group, Orangina Schweppes, the rights to GSK’s Lucozade and Ribena brands and Japan Tobacco’s soft drinks operations, as well as joint ventures in India, China, Vietnam and Indonesia.

Reynolds American

Country: US

Grocery sales: $10.68bn (+26%)

Reynolds ended its year-long attempt to consolidate and reshape the US tobacco market in June as it completed the $27bn takeover of Lorillard. The deal saw the three main players in the US become two and helped Reynolds close the gap on Marlboro maker Altria (Reynolds has broken into the Global 50 at 35 while Altria sits at 19). It now holds more than a 30% share of the $100bn US cigarette market. Part of the rationale was to boost Reynolds’ geographic footprint: its Camel brand is popular in the West of the country and in rural areas while Lorillard’s main brand, Newport, is strong in the North East and in urban areas. However, Reynolds was forced to sell the Kool, Salem and Winston cigarette brands and Lorillard’s Maverick to Imperial Tobacco to get the deal past regulators in a process that lasted a year.

Campbell’s Soup

Country: US

Grocery sales: $8bn (-2.2%)

Soup giant Campbell edged into the Global 50 in 50th place largely thanks to the $231m acquisition of salad and houmous producer Garden Fresh last year. The deal expanded Campbell’s into the deli section of grocery stores, complementing its presence in the produce section. The Garden Fresh deal follows other forays into fresh foods in recent years, including the acquisition of Bolthouse Farms in 2012 and buying up Plum Organics in 2013. The promotion to the Global 50 comes despite a 2.2% revenue drop during the year, but it recorded 1% organic growth driven by a small increase in price and flat volumes. Campbell has also looked to tap the increasingly health-conscious trend in Western markets and became the first Global 50 company to declare it will be labelling products containing GM ingredients.

These margin-boosting efficiency programmes have become widespread - notable adherents include Reckitt Benckiser, Unilever and Danone. As a result, and boosted by the tailwind of lower input costs, average gross margins across the Global 50 rose from 44.4% in 2014 to 45.1% last year, with margins up in all sectors except a minor contraction on beers and spirits.

Yet despite the gross margin growth, the Global 50 experienced a 0.6 percentage point decline in profit margins in 2015 to 16.6% from 17.2% in 2014 and 17.1% in 2013. This suggests focus is beginning to shift from an overriding concentration on the bottom line to driving growth again - to address topline stagnation - through investment in marketing spend and R&D.

Indeed the Global 50’s weighted average marketing spend rose from 6.2% of revenue in 2014 to 6.9% last year while weighted average R&D spend rose from 1.2% to 1.3% of revenue. Notably, marketing spend growth at 3G-owned AB InBev topped the list for those players that split out spend, with a 1.9 percentage point rise as a proportion of revenues.

Will Hayllar points to Reckitt Benckiser as a business that is successfully combining practical innovation and strong marketing to drive better than average organic growth. “Given the overall lack of growth for the past several years, investors may be willing to absorb some margin decline for a period of time if they’re confident that investment has good growth prospects,” he says.

Mergers & acquisitions

While marketing purse-strings are being loosened to counter the low growth environment, another lever being strongly pulled is M&A. Total deal value across the Global 50 was close to 2008’s all-time high, rising to $226bn (from $54bn in 2014). Admittedly deal values were distorted by the bumper $120bn AB InBev SAB Miller deal, but there were seven deals over $1bn in value. And deal volume was the second highest since that 2008 peak, with the 51 deals during the year.

As to what’s driving these deals, more than 94% of acquisitions (by value) were motivated by strengthening positions within existing sectors and markets, rather than diversification or growing in new geographies, as potential synergies and cost benefits are viewed as more helpful than hedging.

“Global consolidation will continue,” says Rothchild’s Sachak, “especially in categories where there are benefits from having a global or regional footprint. There are a number of globally relevant brands that have momentum but could benefit from stronger local routes to market.”

Who’s buying what?

AB InBev/3G Capital

Target : SAB Miller

Value : $120.3bn

Berkshire Hathaway/3G Capital

Target: Kraft

Value: $54.5bn

Japan Tobacco

Target: Natural American Spirit

Value: $5bn

Coca-Cola Enterprises

Target: Coca-Cola Iberian Partners, Coca-Cola Erfrischungsgetraenke

Value: $3.2bn

JBS

Target: Moy Park; Cargill Pork

Value: $3bn combined

Post-Brexit

The uncertainty created by Brexit is a double-edged sword for European targets as the fall in the pound and euro makes them cheaper to international buyers, but Sachak warns there is now “a question mark as to whether the UK will continue to be regarded as a launchpad into a pan-European market”.

What scant organic growth there is has been driven by price, with overall price growth of 2.9% across the 18-company sample, and only Arla Foods reporting commodity-driven price falls.

Where there has certainly been more active investment to address flat-lining organic growth is in digital - not just in terms of digital marketing, but direct-to-consumer propositions like P&G’s dedicated Amazon shop and L’Oréal’s own premium brand website.

Hayllar points out that digital has become a key battleground in the fight for young talent with graduates now more interested in working for start-ups and media and tech firms than consumer goods players. To this end companies like L’Oréal and Pernod Ricard have invested heavily in growing digital skills among staff.

Digital is another reminder (if it were needed) that global fmcg giants cannot stand still or they will become obsolete. And it is by no means Western companies leading the digital charge - with Chinese companies like Yili and Bright Food spending huge sums on content marketing and digital sales channels.

The competitive pressures on the Global 50 are only intensifying and the shock of Brexit has thrown up a new set of regulatory and economic problems. But those companies that can respond to increasingly fragmented global demands - be that through product mix, route-to-market efficiencies or scale - will thrive. Those that can’t will be replaced.

No comments yet