For the world’s largest consumer goods players, struggling to find meaningful growth, the new mantra is clear: ‘If you can’t beat them, buy them’

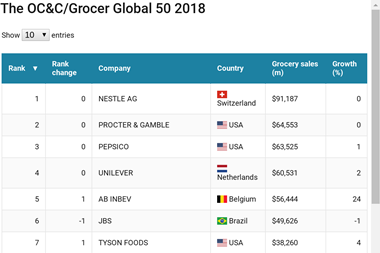

The OC&C/Grocer Global 50 study of the world’s largest fmcg companies charts a dramatic return to top-line growth after years of stagnation. The most recently filed annual accounts of these consumer giants show annual revenue growth jumped to 5.7% - the highest level for six years - after languishing at just 0.3% and 0.5% over the past two as the Global 50 has bolted on mergers and acquisitions of all shapes and sizes and formats to deliver growth.

Almost three-quarters of the revenue boost was driven by M&A as the Global 50 sealed the highest number of deals in 15 years.

The 50 largest fmcg players agreed 60 deals, a 46% year-on-year increase. Those acquisitions were worth $145bn, almost triple the value of deals in 2016 and only beaten in recent years by the $226bn seen in 2015 (a figure distorted by the $175bn SAB Miller and Kraft Foods acquisitions).

This flurry of dealmaking masks a more sober underlying picture for the consumer goods industry, with organic growth still weak at 2.6% - ahead of 2016’s 2.5%, but well down on the 3.7% and 3.8% of 2015 and 2014 respectively. And organic volume growth across those of the Global 50 that split out that figure was an anaemic 0.55% - down on 0.7% last year - with pricing driving the lion’s share.

Given this weakness in the underlying growth profile of global fmcg companies - which have been losing share amid fragmenting tastes in the west and slowing emerging markets - M&A and consolidation has long been seen as a natural industry response.

OC&C’s global head of consumer goods Will Hayllar says such deals may have been hampered by geopolitical uncertainty in 2016, but the drivers of M&A have become so strong that major players have been forced to act. “The industry is clear about the magnitude of the challenges to growth and that they are long-term issues that require a fundamental response,” he says.

Head of global staples research at Société Générale Warren Ackerman suggests the incentive to turbocharge M&A may have been intensified by changing economic circumstances, particularly in the US. “Some of these companies have been able to borrow at negative rates, but there is a feeling that the era of cheap money and capital is coming to an end so there has been a window for M&A to happen,” he says.

The biggest deals have taken place in alcoholic drinks and tobacco. Total revenue growth was 22.2% for the former and 12.3% for the latter as the integration of SAB Miller brands into AB InBev and Asahi and the merger of British American Tobacco with Reynolds American underpinned consolidation-driven growth.

Consolidation is a natural response to long-term volume decline, particularly in tobacco, but on the food side, with the exception of the 2015 Kraft-Heinz deal, mergers are few and far between. There has been a measure of consolidation in coffee, with Nestlé buying the Starbucks consumer business and JAB adding Keurig Green Mountain to its Dr Pepper Snapple business. But Hayllar notes the food space lacks a “natural, active consolidator”, with a lot of players more complex and chaotic as they lack the single category focus of tobacco.

SG’s Ackerman agrees: “In this world of consumer fragmentation, digitisation, hyper-segmentation and localisation, the argument for paying a big premium for a stable of megabrands is harder to make.”

That is not to say other food-focused groups are shying away from making M&A moves - they are just making them in a different way. M&A in food has centred more on buying exposure to higher-growth market segments that big players are under-represented in - diversifying into different sectors, more ‘better for you’ categories and smaller fast-growing premium brands, as well as emerging market geographies. And typically these aren’t mega deals.

Unilever, Ackerman points out, has made 23 acquisitions since 2015 with an average turnover of just €100m, while eight of the Global 50’s top 10 are investing in growing smaller brands through venture funds or incubator programmes. Money is also being poured into direct-to-consumer subscription businesses, like Dollar Shave Club and Tails.com, as well as non-brand innovation, including logistics technology platforms and marketing and analytics startups.

“Many of these global consumer goods companies are going to have to make much more radical shifts outside their comfort zone to sustain healthy growth,” says Rothschild’s global head of consumer Akeel Sachak.”I don’t think buying another mature category business and generating in-market cost synergies is the answer long term.”

The jury remains out on whether investment in smaller, higher-growth brands will be the strategy that moves the needle on organic growth. The Global 50 have relied on their international reach and relative market strength - as well as the increasing shift towards premiumisation in their product portfolios - to drive organic price increases of 2.06%.

But price has been growing consistently above volume for a number of years, with industry volume growth well below global population growth of 1.1% for each of the past three years. Clearly the Global 50 are not growing sales as fast as their smaller rivals.

“Buying small bolt-ons is not enough to move the dial on organic growth, but it can be an important part of a wider growth strategy,” says Hayllar, pointing to Diageo’s use of M&A and own-brand development to grow exposure in premium spirits. “Diageo’s reserve brands now contribute a third of its growth - so the cumulative impact of doing several things that are individually quite small can start to become noticeable.”

Strategic divestments can also drive a recovery in organic growth, as shedding low-growth businesses - such as Unilever’s spreads division - immediately enhances like-for-like growth prospects as the portfolio becomes more centred on higher-growth assets.

SG’s Ackerman notes that acquisitions take 12 months to have any impact on organic growth, but that Unilever claims the businesses it has bought are growing at an annual average of 16% and acquisitions and divestments will add 100 basis points to organic growth by 2019. He also points out the collective impact of this portfolio optimisation - Nestlé’s strategic M&A activity adds up to a 10% change in its $90bn portfolio.

However, portfolio remodelling brings its own challenges, like how a large global stable of mega-brands can keep the characteristics of the smaller more dynamic brands they snap up. These more niche brands are likely to require different positioning and activation to traditional mass-market brands and question marks remain over the ability of, for example, global brewers to manage the host of craft brewers they’ve snapped up.

“There is a real tension for these businesses,” says Hayllar. “How do you balance scale efficiencies with the need to keep these brands distinct and not crush and kill off the very things that made then attractive in the first place?”

Identifying the right growth brands to buy is also far from simple. “There are a number of conflicting trends - provenance versus localism, naturalness versus functionally healthy. It is not straightforward to work out which business is going to resonate, ensure and become drivers of scale in the future.”

There is, though, a sense the global fmcg companies have woken up to these deep structural changes - the category shifts, consumer segmentation and rise of e-commerce rather than focusing simply on the bottom line. That might also be because they feel they can.

Once again the Global 50 has made more progress on profitability than it has on organic sales growth. The OC&C/Grocer Global 50 report shows the Global 50 squeezed out a 0.7 percentage point improvement in gross margins, continuing a long-established trend.

Average gross margin has risen in six of the past seven years, climbing from 43.4% in 2010 to 46.2% today. Removing exceptional items, the Global 50 posted its first rise in net margin for three years - up to 17.1% after dropping as low as 15.8% in 2011.

Zero-based budgeting: discredited?

One of the key drivers of this shift has been the cost-cutting playbook of 3G Capital - owner of AB InBev and Kraft Heinz - and its zero-based budgeting mantra.

Zero-based budgeting, where each year costs start from scratch and every penny spent requires a return-based justification, has become increasingly prevalent across consumer goods giants, with 11 of the Global 50 adopting ZBB principles in recent years.

There is evidence this has had a positive effect on the bottom line beyond those 3G Capital-owned businesses. In total, five of the top seven margin improvements across the Global 50 are ZBB adopters. Campbell and Kellogg’s increased margin by 5.7ppts and 4.7ppts for example.

AB InBev, the poster child of ZBB, is still delivering growth (and improving profitability) through consolidation and premium pricing. However, average organic growth among ZBB adopters was just 0.3% compared with 3.1% across non ZBB players, with Kraft Heinz’s 1.3% figure particularly unflattering versus other diversified players like Danone (4.3%) and Nestlé (4.1%).

Sachak says the de-rating of Kraft Heinz shares over the past six months suggests “the market is no longer as convinced that cashflow and profit growth that isn’t accompanied by robust organic growth is sustainable for the long-term health of a business”. The danger for ZBB advocates is that a significant proportion of bottom-line growth has been driven by slashing marketing and R&D spend, which could actively undermine growth opportunities.

The Global 50 reduced marketing spend by 0.1%ppts to 10.9% last year (down 0.7ppts to 9.9% in food and 1.2ppts to 14.3% in beer and spirits. Weighted R&D spend was flat at 1.5% grocery sales.

This effect was more pronounced among ZBB players, though, with those companies cutting SG&A (selling, general and administrative expenses) and COGS (cost of goods sold) by significant proportions since adopting ZBB principles - a collective 8.5% at Mondelez, 7% at Kellogg’s and 6.4% at Campbell.

Cost-cutting advocates have argued lower marketing costs reflect the growing power of digital and an increased focus on more targeted, less mass-market campaigns. But Jefferies analyst Martin Deboo believes the decline of the power of traditional media has been exaggerated - noting “media reach goes hand in hand with growing penetration and mass reach is still the near-exclusive province of traditional ‘linear’ TV.”

Even if more efficient marketing spend is accepted as positive, the lack of cash being funnelled into R&D seems worrying. “The underlying consumer shifts are more material at the moment so the need to have the right product is more critical than ever,” Hayllar argues. However, the lack of R&D spend could also be related to M&A strategies, with companies prioritising buying ready-made propositions that can be scaled up.

Ackerman suggests the overall R&D spend has become less important than how fmcg R&D departments operate. “Ultimately the whole game is now about speed,” he says. “There’s no point having lots of people with PHDs doing interesting stuff with a 10-year time horizon. If you can’t launch a new product from concept to shelf in 12 to 18 months then it is too slow.”

That also explains the increasing investment in external incubator schemes, such as Nestlé’s Henri programme and Unilever’s Foundry.

A geography lesson

One of the primary drivers of the cost-cutting trend has been long-term weakness in the US consumer market, and the food sector in particular. That weakness persists, with only two of 18 US companies in the Global 50 achieving above-average growth rates. It also resulted in a wider underperformance in food growth, with local currency sales growth of just 0.8% compared with 22.2% in beer and spirits, 12.3% in tobacco and even 2.9% in household and personal care.

The macro-economic conditions in the US remain relatively positive, but Hayllar argues US-centric companies will continue to drag on overall Global 50 growth. “The challenge of the big North American food businesses is more on competition and shifting consumer habits than macro-economics,” he says.

Jefferies’ Deboo argues problems are specific to the US, given online grocery remains at just 2% (compared with 7% in the UK) and own-label food penetration is only 17% (the UK is at 50%-plus).

Global players have traditionally relied on high-growth emerging markets to mitigate long-term sales slowdowns in developed markets. But economic weakness in Brazil and Russia and a slowdown in China has starved players of their usual growth engines.

“If you’re a consumer staples company you have to accept developed markets have no growth and are deflationary, while emerging markets are volatile,” says Ackerman. “The only way you grow is by gaining market share, innovating and being more relevant.”

A further headwind for the Global 50 are the looming trade barriers stemming from US President Donald Trump’s protectionist policies, as well as Brexit. Consumer goods players are less exposed than some industries, given a higher proportion of goods are manufactured locally. However, any impediment to the flow of agricultural products around the world could have a significant impact on manufacturing.

“The most widely affected area might be beverages,” says Moody’s senior analyst Ernesto Bisagno. “We have already seen Jack Daniel’s increase prices by 10% and it could be similar for Diageo.”

Despite an uplift in headline growth, the overall picture for the Global 50 remains one full of challenges. But these challenges - losing market share to smaller players, fragmenting consumer tastes, the power of digital and e-commerce - are nothing new and the fmcg giants are working to formulate their responses.

Crucially that response now seems to widely recognise that growth is key for long-term relevance and potentially survival. Global 50 players are redefining their portfolios and their management structures, investing heavily in buying and/or growing smaller, more bespoke, on-trend brands as well as nurturing startups and funding new sales platforms and marketing technology. The next stage is delivery - and that will be primarily measured by growth. Success won’t come easy, but at least the Global 50 are in the race.

Footnote: How commodities prices affected the Global 50

There was a mixed picture for commodities in 2017 - with key inputs into food and drink remaining relatively benign despite a big rise in energy costs.

Most key commodities were back on the up after a number of years of marked decline, though in most cases this rise remained in single digits.

Nevertheless, the pricing mechanics of a number of Global 50 players was supported by higher commodity prices in 2017. For example, the bulk of Arla’s 11.2% organic growth was driven largely by the escalation in dairy prices during the year.

Crucially the Global 50 seemed able to pass on the bulk of input inflation, with organic price growth of 2.2% suggesting consumers have absorbed most of the impact.

OC&C’s head of consumer goods Will Hayllar puts this ability to pass on inflation down to the Global 50 often enjoying strong positions within markets.

Jefferies analyst Martin Deboo comments: “UK food producers saw rapid commodity inflation because of Brexit and the depreciation of sterling, but that is not true worldwide where there hasn’t been material commodity inflation for four or five years.”

However, looking at the rise of underlying commodities - most notably global oil prices - that benign environment could be set to change.

“Agricultural inputs do on average move with the oil price, albeit slightly lagging it,” says Hayllar. “Petro chemicals is such a big part of input costs across agriculture that over the next six months it will start to make itself felt”.

Brent Crude is currently trading close to $80 a barrel, having been at $45 in June 2017 and plunging below $30 in early 2016.

No comments yet