The world’s fmcg giants survived the pandemic. Now they’re facing into rampant inflation. Are they agile enough to handle rising costs, changing shopper habits and geopolitical volatility?

Many of the globe’s largest consumer goods businesses have brushed off a global pandemic to come out of Covid in rude health. The annual OC&C Global 50 for the Grocer paints a historic picture of an industry bolstered by pandemic demand and the roaring return of out-of-home dining, drinking and spending.

Largely analysing the 2021 calendar year, the annual accounts of the world’s 50 largest fmcg companies showed growth at a decade-long high. Aggregate growth surged to 9.3% from just 1.1% in the previous year, with broad-based sales increases linked to higher volumes and prices and strong organic growth.

Overall performance was helped by a strong rebound in beer and spirits as pubs and restaurants reopened to rise 11%, while food and drink suppliers were also up 11% as they held onto pandemic gains.

Those 24 companies that do split out organic growth showed volume growth of 3.4% and price/mix growth of 4.5% to post-organic growth of 7.9%, compared to just 1.7% in 2020.

The margin picture was a little less rosy, with gross margins edging down 0.1%, though a reduction in operating costs during Covid meant adjusted EBIT margins increased 0.7 percentage points to 19.1%.

According to Jefferies consumer analyst Martin Deboo, it is evidence that the thesis of those who wrote off the sector amid stagnant growth rates of 2017/18 was “massively overdone”.

“When the chips were down under Covid, it became all about the ability to supply at scale, and it was the big guys who were able to service that demand that benefited during lockdowns,” he argues. So far, so good.

Now however, a new challenge is already underway: an inflationary fever gripping the world that could prove harder to shake off.

“Inflation is so widespread, everybody has accepted prices must go up”

The post-Covid jump in the cost of logistics and shipping has joined with sharp increases across agricultural raw materials, the rising cost of labour and – following Russia’s invasion of Ukraine – soaring energy prices, to create an inflation tsunami.

The world annual inflation rate reached a 25-year high in April of 7.4% and has continued to rise sharply. This is not the first 21st century inflationary spike fmcg producers have had to manage, but OC&C managing partner Will Hayllar notes the magnitude of the increases is “significantly higher” than other recent rises. “It does mean that in some ways producers are following the same playbook to pass inflation through, but the industry is going into uncharted territory in terms of understanding if those methods are still valid,” he says.

Illustrating the pressure on the giants’ balance sheets, Unilever, for example, is facing having to recover some €4.6bn of raw material inflation just this year, though the signs from first-half results were broadly better than the market feared.

“So far we see prices being very successfully passed on,” says OC&C partner Claire Dannatt. “Inflation is so widespread and significant that everybody has accepted prices must go up.”

Not that price rises are always happening easily. In the UK, Tesco has publicly gone into battle with Colgate, Kraft Heinz and Mars over price disputes this year, although Bernstein consumer analyst Bruno Monteyne suggests such disputes were overplayed. “It reminds me of American wrestling, with big shows of bulky guys fighting each other, but in the end it is all a choreographed dance. The brands are all back on shelves at much higher prices than before.”

Although the picture on sales volumes was a little more mixed, overall pricing was ahead of expectations, allowing consumer giants to grow top-line and suffer less margin damage than most had assumed.

‘The worst is yet to come’

The major concern now, though, is whether there is a limit to pushing inflation through with pricing, as macro-inflation continues to mount.

Although there is some evidence that commodity pricing and transport costs have eased coming into the second half of the year, the major drivers of inflation – energy, labour costs and geopolitical volatility – will provide little respite for the rest of the year. “The general consensus is that the worst is yet to come,” says Deboo. “Even if the inflationary environment shows some signs of easing, the consumer environment is getting decisively worse.”

Fitch Ratings lead fmcg analyst Giulio Lombardi adds: “Those companies which are more exposed to private label replacement that don’t have strong pricing power, or have not hedged effectively, will need to increase prices to cover their costs – but those price increases may be too high for the consumer to tolerate.”

That has led to much industry scrutiny on the scale of downtrading and the likelihood of big branded players losing share to private label producers or customers buying smaller packs.

Deboo notes some early signs of private label taking share – but counter-intuitively, he argues, this is typically in categories with smaller price gaps, such as toilet paper and tissues, and less where there are significant price gaps such as skincare and cosmetics. “It comes down to the fact that brand equities and consumer engagement in those categories is so much higher, so people are more resistant to trading down,” he says.

This complex picture looks unlikely to have a uniform effect, with some categories such as dairy, bakery or cleaning products more exposed to downtrading, and those with higher brand equity able to maintain price gaps and volumes.

As a result, says Rothschild global head of consumer Akeel Sachak: ”You will see private label growing and consumers trading down to lower price brands. But at the other end of the spectrum, for super-premium products, there will be less impact.

“Therefore, valuations will become more bifurcated between those more resilient in this environment and those more vulnerable.”

Additionally, private label suppliers tend to operate on tighter margins so will arguably come under more pressure than large producers to raise prices – meaning the price gap between private label and brands is unlikely to expand significantly.

Monteyne concludes: “The amount of sales these big brands have to lowest income consumers is a very small part of their business. To really see significant pain you’d need to see a major recession, with the middle classes losing jobs and worrying about money before they trade down from brands.”

The other side of the coin to downtrading is premiumisation – a key driver of growth for global players to move western customers up the value curve and bring consumers from growing economies into major brands from local products.

Fitch’s Lombardi expects economic conditions to dampen the overall trend, suggesting premiumisation will be less prevalent and more selective in nature.

“When the chips were down under Covid, it became all about the ability to supply at scale”

Hayllar agrees large fmcg players will be less reliant on premiumisation for performance delivery, given they will be persuading consumers to spend higher sums on their existing consumption, but it will remain a key plank of the growth platform. “Premiumisation is still the long-term path to growth for this industry as population growth slows across the globe,” he says.

Dannatt adds: “It’s still important to have premium strategies and products for those consumer groups more able to keep spending or who could be trading down from even more expensive super-premium goods… Big players have become very good at thinking about bifurcated strategies and a full portfolio structure will remain extremely important.”

One other possible spanner in the works from an economic perspective is the likely shift away from out-of-home consumption, having only just returned from Covid. While that will potentially benefit grocery suppliers, those with a significant out-of-home weighting – alcohol, soft drinks, snacking – could see their mix hit again as the public cuts back on spending.

Deboo suggests producers will likely focus on top-line protection, possibly sacrificing margin to maintain sales. “Investors are more tolerant of temporary reversals and compressions in margin than they are of top-line stagnation. Therefore brands will manage their promotional strategies to keep market share up, which could squeeze private label.”

That thinking is predicated on the lesson from the recession of 2008: that margin impact was short-lived and global fmcg saw a strong rebound a year later. Of course, economic conditions are different again from the last recession – but the benefits of scale that enabled global giants to bounce back have reasserted themselves during the pandemic.

Hayllar says: “In the past, scale has been seen mainly as an absolute cost advantage and efficiency benefit, but scale can be a resilience benefit if companies have factories around the world and more options to deal with disruption from spikes in demand.”

“These businesses are benefiting from their diversification,” says HSBC analyst Jeremy Fialko. “Their scale gives them more ability to flex their network when they run into supply chain difficulties or problems sourcing something.” It seems the old cliché of smaller, local players using astute NPD and savvy digital marketing to run rings around slow-moving multinational behemoths may be diminishing.

Sachak also believes the major beneficiaries of current volatility “will be the largest, most geographically diversified groups, which have a product and brand mix that can pivot to a changed environment most readily”.

A changing climate

That diversification could prove especially useful if the current inflationary trend continues into the long-term. The global economic, geopolitical, environmental uncertainty certainly suggests it could be, and points to an underlying climate that will ask fundamental questions of these consumer giants.

“The world has become less stable – both in geopolitical terms and environmentally, with more extreme weather events, both potentially impacting key inputs,” says Hayllar. “So these companies need to rethink how and where they invest, right-size portfolios and product mix, and have the right supply chain set-up and geographical spread.”

“We’re still in the early stages of that more fundamental response – which is likely to create businesses that are slightly less efficient than they were previously.”

Covid illustrated the vital importance of durable supply chains, so it is unlikely consumer groups will return to lean, cost-effective but unresponsive systems given the need for resilience and flexibility. Additionally, sustainability issues and commitments to net zero cannot be deprioritised to recover margin, given consumer, investor and employee demands around ESG, which will add longer-term structural costs to businesses.

Fmcg giants are also likely to continue their trend towards geographic diversification, to spread risk, find pockets of growth and lower reliance on regions with geopolitical or economic issues, such as China.

“There will need to be more thoughtful diversification across geographies,” says Dannatt. “Some may retrench back into their heartlands and be more risk-averse, but there remain structural drivers for those prepared to hold their nerve and invest behind growth opportunities to broaden their global outlook.”

With disruption in eastern Europe, and China potentially becoming a tougher market in which to find growth than it has been in recent history, companies may renew their interest in some bigger economies in southeast Asia, including India, where inflation is actually falling.

The focus on getting geographical approaches right has also led to restructures at the likes of P&G, Coca-Cola, Kraft Heinz and Unilever – all aimed at improving agility and responsiveness as well as realising some efficiency cost savings.

“This might appear to just be a bit of organisational reshuffling or slight cost-cutting, but actually there is a much more fundamental shift going on in terms of decision-making power within those organisations to respond to longer-term structural change,” Dannatt concludes.

“The world has become less stable. Companies need to rethink how and where they invest”

The final major plank of response to this changed world is portfolio management, to ensure diversification and exposure to pockets of growth and profitability.

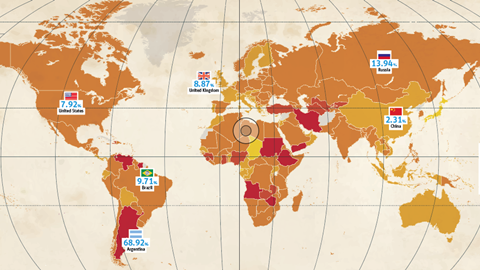

2021 was a year of significant recovery in terms of Global 50 M&A activity, with 50 disclosed deals for $65bn – the highest level of dealmaking since 2018 – as L’Oréal, Nestlé, Coca-Cola, Heineken and Mondelez all made multibillion-pound acquisitions.

That activity has understandably shuddered to a halt in 2022 amid uncertainty, volatility and resultant difficulties in valuing assets, and has coincided with a pre-pandemic trend of fmcg giants becoming more conservative in terms of their balance sheets and debt ratios, with 37 of the 50 groups deleveraging in 2021 compared to the previous year. And with debt also more expensive, large-scale debt-driven industry consolidation looks off the table.

However, the longer-term drivers of M&A across global consumer multinationals remain compelling, both in terms of acquisitions and divestment.

“The trend to diversify portfolio and divest non-core assets will continue,” says Sachak. “There is an imperative in big fmcg to refocus and get out of business where they don’t have a relative competitive advantage, or that is dragging down overall growth or margins.”

Private equity was a major player in consumer M&A in 2021, with 42% of deal value among Global 50 transactions involving a PE buyer compared with 28% in 2020 and 21% in 2019.

The soaring cost of debt is likely to hamper PE involvement in the short term, which could constrain divestment opportunities – but equally it could give big corporates a freer run at assets for which they may previously have been outbid.

Hayllar comments: “The pause in private equity activity should, over the next few months, eventually lead to a resetting of value expectations… For those producers with strong balance sheets, it might be a good time for them to be thinking about where they want to invest to change their future trajectory.”

The trend for investing in faster-growing businesses and categories is likely to remain a key driver of activity. Hayllar says: “Growth is difficult to organically generate over a long period, so these companies will be thinking about those structural trends they want to tap into to provide growth, rather than focusing too much on the inflationary environment right now.”

The world’s largest fmcg groups have come out of Covid with renewed strength and answered industry naysayers suggesting scale was an outdated concept. Now they face a wholly new challenge. And the types of response that saw them through the global pandemic – supply chain durability, geographic and category spread, pricing power – will again be key factors in emerging from the current volatility with strength.

The world is rapidly changing once more – with the big beasts determined to leverage their advantages.

Commodities

Not all commodities are at historic highs, but amid soaring macro-inflation and energy prices, global food groups have had to manage vast ingredient input inflation against the prevailing trend.

Food inputs were climbing steeply already in the second half of 2021, but this trend was supercharged by the war in Ukraine. Russia’s invasion in February had the effect of restricting supplies of vital foodstuffs, wheat in particular, while driving up wider commodity costs.

In just two months at the start of the year, wheat prices jumped 30%, maize by over 21%, and sunflower and palm oil were up by 67% and 32% respectively.

However, there has been some respite, with wheat down almost 27% from 2022 peaks and sunflower oil falling 34%.

“Many commodity prices are rapidly coming down as a lot of the bottlenecks disappear and economies start slowing down,” says Bernstein’s Monteyne.

However, the easing in some commodity prices will only have a “marginal” beneficial impact in the immediate term, according to OC&C’s Hayllar, given macro-inflation continues to rise and energy costs show little sign of easing.

“Energy is still moving in the wrong direction, but there is evidence of food commodities softening,” he says. “Broad-based crop commodities will begin to come down as there is a planting response to the higher prices.”

OC&C Global 50 food and beverage rankings: how fmcg giants are tackling inflation

The world’s fmcg giants survived the pandemic. Now they’re facing into rampant inflation. Are they agile enough to handle rising costs, changing shopper habits and geopolitical volatility?

Currently

reading

Currently

reading

OC&C Global 50 food and beverage rankings: how fmcg giants are tackling inflation

- 2

- 3

No comments yet