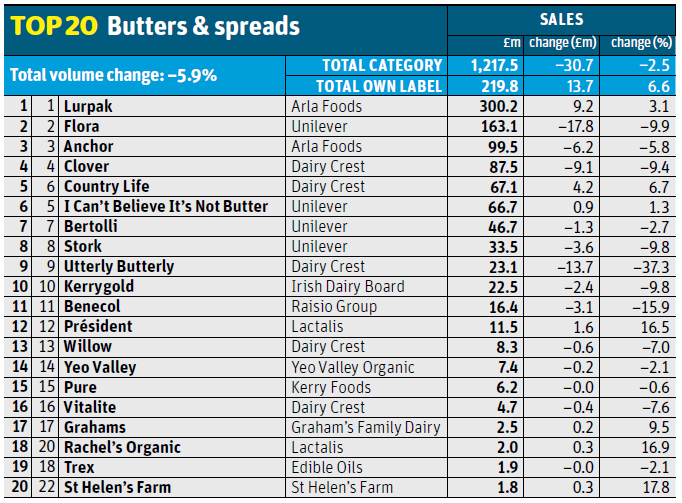

If 2013 was a tough year for butters and spreads (value was down 4.3% on volumes down 5.9%), the past year has been even tougher. In volume terms, at least. Value has continued to slide, by 2.5%, while the volume fall has accelerated to 5.9%.

That’s despite the continued popularity of home baking, personified by Mary Berry and The Great British Bake Off. Brands have taken the biggest hit: they’re down 4.1%, an eye-watering loss of £42m, on volume down 8.1%, suggesting they’re not doing enough at present to convince shoppers they are worth their premium over own label, which is in 6.6% growth to £219.8m; volume is up 4.4%.

Look beyond the headline figures, though, and performances across BSM vary enormously. While many spreads continue to have a tough time (Flora sales are down nearly 10%, while Clover is down 9.4% and Utterly Butterly is down 37.3%), some butter brands - especially at the premium end - have managed to take advantage of resurgent consumer interest in butter as the focus of the public health agenda has shifted away from satfat and towards sugar.

Louise Pike, head of marketing for BSM at dairy Crest, says BSM is subject to “two distinct movements”: the growth of butters - benefiting from consumer trends towards naturalness and a shift in retailer promotional focus - and a decline in spreads.

“Butter is where the action is,” agrees dairy industry consultant Hamish Renton. “Consumers are changing their preferences, and valuing natural dairy products like butter over the transfat-rich alternatives.”

These trends are plain to see in the performances of the category’s big hitters. Market leader Lurpak, for example, has managed to increase overall value by 3.1% to top the £300m mark despite a 4.2% volume loss over the past year.

“The category has received a battering this year, and we have been focusing on the basics” Polly Price, Adams Foods

And Dairy Crest’s Country Life butter has had a storming 2014 after losses in 2013, with the increased consumer desire for unprocessed products contributing to a 6.7% growth in value to £67.1m in sales, says Pike, with volumes up 8.1%. “Butter is perceived by many as less processed than margarines,” says Pike. “This consumer trend towards ‘natural dairy goodness’, together with an intelligent promotional programme, has benefited our Country Life brand this year.”

Mike Walker, head of BSM Arla Foods, points to the strong performance of Lurpak Spreadable as a key factor in Lurpak’s continued growth over the past year, with consumers recognising “the value of Lurpak and trading up from dairy and sunflower spreads.”

Lurpak has done well on the value front despite losing volume, as consumers cut back on “traditional hosts” for butter - such as bread and crumpets - over the past year. This is partly because of its commitment to premium NPD, claims Walker, including the introduction of a four-strong range of butter-based products under the new Lurpak Cook’s Range in March.

It is such activity that ensured Lurpak proved to be the “key winner” in the category during 2014, concurs Jonathan Fairclough, chilled and frozen foods buying controller at The BuyCo. He adds the brand’s venture into new territory with the Cook’s Range, and its “significant above-the-line support, focusing on the usage occasion of the brand in scratch cooking and baking,” has helped the brand succeed in a declining market.

Other key examples of premium butter brands doing well include Lactalis’ Président, up 16.5% over the past year on volumes up 14.2%, and Rachel’s Organic, also part of the Lactalis stable, which has grown by 16.9% to £2m as volumes have surged 7.9%. That’s not to say all premium NPD works. Lurpak Slow Churned, launched last year and sold in a premium silver-coloured aluminium dish, failed to gain year-round traction with shoppers and is no longer available as a permanent line.

Indeed, not all butter brands have had it easy. Anchor, also made by Arla, experienced a 5.8% decline in value sales to £99.5m, despite a £14m multi-channel marketing campaign to celebrate “everyday family moments.” Volumes fell by a much heftier 12.3%, suggesting shoppers were discouraged by a rise in the brand’s average price. It has “seen a more challenging period impacted by competitor promotional activity and continued price deflation of own-label”, says Walker, adding Arla will continue to invest in the category in 2015 and expects “both Lurpak and Anchor to outperform the category based on strong plans and marketing investment.”

Elsewhere, a “quiet year” on the promotional and NPD side contributed to a 9.8% fall in value sales for Adams Foods’ Kerrygold. “The category has received a battering this year, and we have been focusing on the basics with our core range,” says Adams Foods category manager Polly Price.”We’ve been quiet compared to our competitors,” she admits, with Adams Foods launching only one piece of NPD - an unsalted block of butter - this year.

Yet despite volume sales falling by 24.3%, Price claims the brand has managed to sustain higher prices, with a loyal consumer base “coming back to us whether we are on promotion or not.”

Kerrygold produced a limited-edition pack designed by Irish designer Orla Kiely during the autumn, which attracted a younger demographic, Price says, and will return to promotional and marketing activity during 2015 by focusing on the natural health benefits of butter.

In spreads, meanwhile, the category dynamics continue to be tough. Flora has lost £17.8m over the past year - a less dramatic decline than in 2013, thanks perhaps to an ongoing advertising campaign for the brand, but still cause for concern. Rachel Chambers, Unilever’s marketing manager for spreads, acknowledges the category “remains challenging” and points out it “has been in decline for a number of years.”

Bucking the trend, however, is Gold from Flora (see Top Launch; p101) - a blend of golden butter and Flora - and Bertolli with Butter, made with Mediterranean olive oil, Chambers says. Launched by Unilever this year to respond to growing shopper interest in butter, they were the fastest growing BSM NPD of 2014 and a key driver in “record-breaking household penetration for spreadable butter,” generating £3.5m in value terms since launch, Chambers claims.

Pike at Dairy Crest, meanwhile, points out that a softening in promotional activity on spreads over the past year has helped contribute to a reduction in overall sector volume, with Clover seeing a drop in sales of 9.4% to £87.5m. Despite the widespread decline in the spreads sector, however, “Clover volume sales have outperformed the market and the brand has maintained share performance,” she says, adding Dairy Crest’s loyalty metrics also remain positive.

And despite a significant fall in value sales, Utterly Butterly continues to perform well within its target market “as an all-round good value proposition,” she stresses. So does rival I Can’t Believe It’s Not Butter, it would appear: the Unilever brand has bucked the general decline with value up 1.3% on volumes up 2.7%. A significantly lower price has no doubt helped.

Top launch: Gold by Flora Unilever

With consumers switching from spreads to butter, Unilever launched Gold from Flora in May.

The standalone sub-brand contains 40% less satfat than block butter, and 30% less than spreadable butter. It was designed to fill a gap in the market for consumers who wanted the health credentials of a spread but craved the taste of butter, said Unilever. Gold offered “all the sunflower goodness of Flora with the taste of butter”, added Patty Essick, Unilever’s UK brand building director for spreads.

No comments yet